|

LISTEN TO AUDIO VERSION:

|

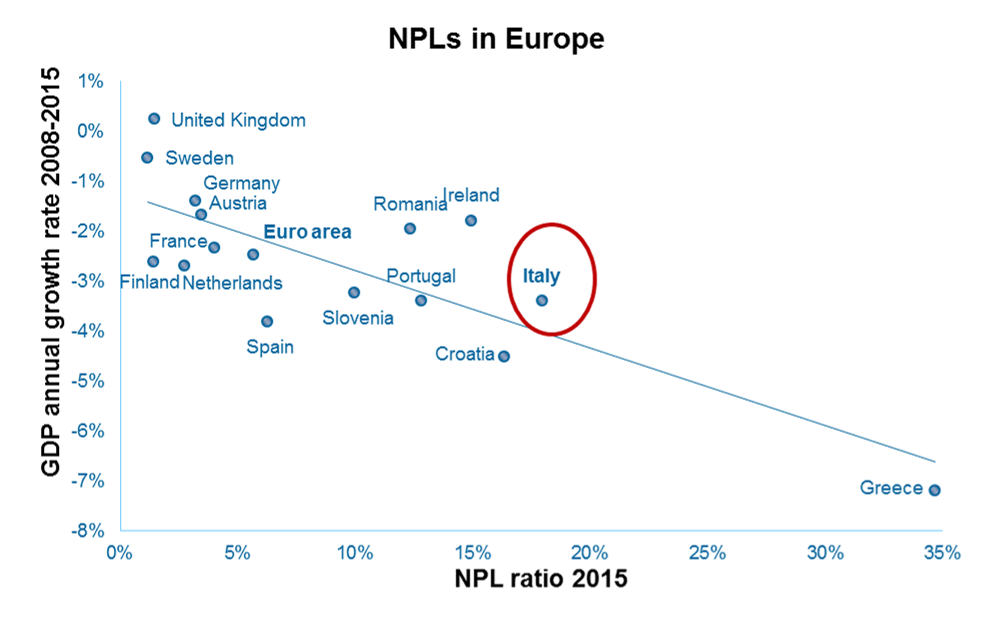

NPLs in Europe

A cross-country analysis shows scattered results with the highest NPLs ratios in those countries that are more affected by the financial crisis, such as Italy.

The NPL growth bears important consequences both at microeconomic and macroeconomic level. For a single bank weakened credit quality, a negative development of the value of collaterals and increasing supervision scrutiny raise provisioning costs to a critical level. From an aggregate view, banks with weaker balance sheets tend to lend less. This leads to a vicious circle where economic growth is not sustained by the financial system and the financial system cannot rely on the real economy to sustain stability.

Until now, finding a solution for the NPL puzzle has been a daunting task for banks and regulatory authorities across Europe. For a comprehensive analysis, see e.g. IMF Staff Discussion Note “A Strategy for Resolving Europe’s Problem Loans”.

Additional pressure will arise from stricter rules on credit classification (see e.g. EBA, “Implementing Technical Standards on Supervisory Reporting”, 2014) and IFRS 9, coming into force in 2018 and significantly changing the impairment methodology and provisioning dynamics. And last but not least from the ECB “Guidance to banks on non-performing loans”, released March 2017.

NPL in Italy

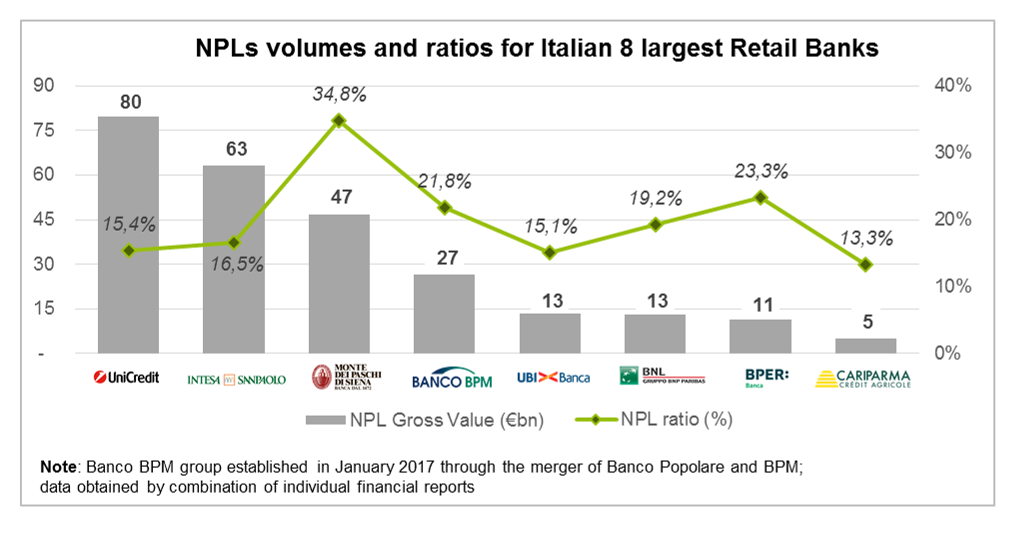

As it is widely known, Italian banks face a severe NPL challenge: at the end of 2015, the NPL stock of banks peaked at € 360 bn. The increasing provisioning costs have brought the profitability of banks to a historically low level, generating concerns about the future perspective of revered financial institutions and the industry as a whole.

In line with the findings of the IMF study mentioned above, authorities and regulators in Italy have moved forward trying to solve the credit quality issue abiding by European rules on state aids. In order to build the clear and favorable context needed to unleash market forces, a few important reforms have been recently issued. The most important reforms aim at strengthening legal protection for collateral claimants (e.g. Law 49/2016), streamlining judicial procedures (Law 132/2015 and Law 59/2016) and facilitating portfolio funding (e.g. guarantee scheme for securitization of NPLs or GACS) and sales.

While exogenous factors seem to be in motion to lay the foundation for recovery (as demonstrated by the growing volume of NPL transactions in Italy), individual banks need to implement a pro-active and comprehensive approach towards NPL.

Call for action—cleaning up the portfolio and keeping it clean

Experience suggests that the current situation is not only a result of the unfavorable economic environment but also of deficiencies in managing sub-performing and non-performing loans. Hence, tackling the NPL issue requires both, a clean-up program and the implementation of a distinct and advanced operating model ensuring to address problematic loans effectively at an early stage—the sooner, the better!

The scale and substance of the clean-up depend very much on the characteristics of the portfolio. Actions that are often taken include portfolio sales, outsourcing to overcome an acute capacity shortage or campaigns (offering a final settlement against a partial repay, etc.). In practice, the capability of a bank to absorb losses resulting from a clean-up is very often a limiting factor that needs to be taken into account when defining the program.

In addition to one-off actions, banks also need to enhance their NPL management capabilities implementing a distinct operating model. From our experience, there are four key areas to be mentioned:

(1) Value-based management strategy—how to maximize the portfolio value?

When it comes to defining the NPL strategy, the fundamental question should be how to maximize the portfolio value? Banks need to agree on a leading methodological framework to answer this question. From our point of view, the methodology should be based on estimating the net present value (NPV) of a portfolio and its elements as the NPV includes all relevant cash flows (expected cash-ins from collection or asset remarketing, but also any costs related to processing as well as funding). Besides, comparing the NPV of different options provides consistent answers.

Furthermore, defining the strategy is based on three major aspects: (i) Portfolio structure, (ii) Possible treatments and (iii) Relevant constraints. To bring these three elements in accordance is a turnkey for consistently managing the NPL portfolio.

The result of this exercise is a clear definition of a dynamic and data-based portfolio segmentation and the treatments to be applied for each segment. In addition, it is a strategic plan defining quantitative targets for reducing the NPL portfolio and for the expected return as well as the impact on capital, balance sheet and P&L.

(2) Governance and organizational design

The shaping of an NPL strategy should be sustained by a sound organizational design, which has to support the implementation of treatment strategies and allows for reaching defined targets. According to our experience, some elements are pivotal in order to build an appropriate governance structure and operational setup:

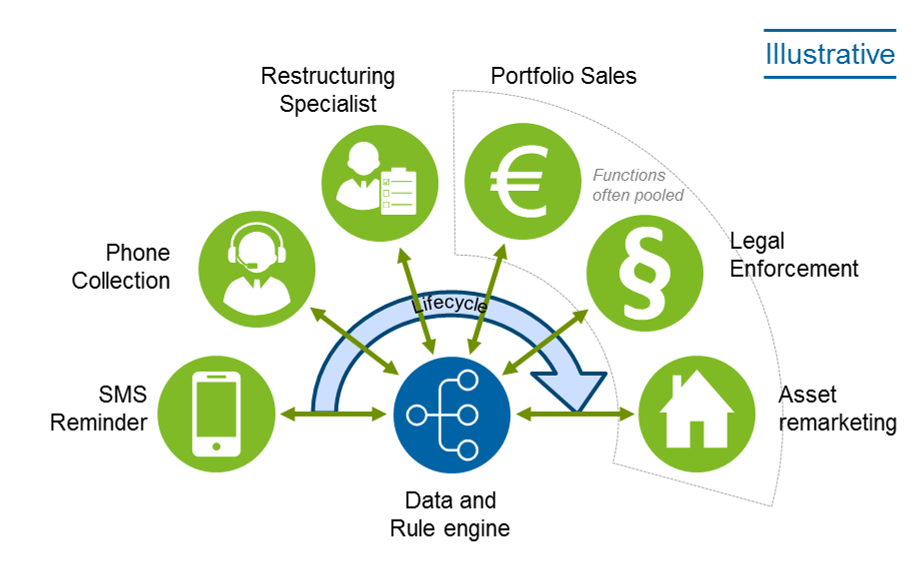

- Clear separation within the organization: units for managing sub-performing and non-performing loans should be clearly separated from loan origination (and maintenance) to avoid conflicts of interests and to ensure the unit is fully dedicated and focused on NPL; furthermore and depending on the portfolio size, banks should consider to separate early arrears, restructuring and workout as tasks and processes differ significantly.

- Specialization and clear roles following identified core tasks (whenever applicable given the individual portfolio and strategy): examples may be restructuring specialists, a team to manage distressed real estate assets, remarketing of repossessed assets, investor relationship management or provider management for external servicers.

- Outsourcing: experience suggests that outsourcing of collection to specialists is (i) a powerful tool to manage growing or volatile volumes while keeping the internal workforce stable and (ii) may increase recovery rates leveraging knowledge and best practices of the provider. The same applies to the support from external lawyers in legal enforcement procedures. In any case, outsourcing requires a continuous provider management (selection, SLA setting, performance monitoring, etc.)

- Steering and decision-making processes: consistent application of the principle of proportionality, i.e. delegation of decision power for low risk, but involvement of top management for high risk cases and strategic decisions; ideally decision-making processes are supported by comprehensive data sets and rules / decision trees.

(3) Efficient and IT-supported processes

Process design and IT support are key enablers for increasing the performance: a forward-looking approach will leverage advanced analytics to classify each single loan, decision engines and rules to derive the next action to be taken and workflow systems to manage and monitor the execution of actions and processes.

In fact, the outlined approach provides two great challenges: one is to design the IT architecture, to define relevant data flows and to integrate the various systems. The second challenge is to define the rules and decision logic to achieve high efficiency and to reduce manual efforts. A simple example may illustrate this idea: when the call center contacts a client, the agent should have a list of treatments (e.g. reduction of installments, payment holidays) suggested by the system based on the client’s data on the screen, so they can immediately agree on a possible solution together with the client. In a next step, banks may think about implementing a self-service portal where the client can choose between pre-selected options and send a reminder SMS with a personalized link to this portal.

Also more complex processes like restructuring an SME loan should be comprehensively supported by selecting eligible candidates based on decision trees or a “viability score” and dispatching these files to a specialist for review and final decision concerning the next steps. In addition, the process itself should be supported by a workflow to allow a final, yet important a monitoring of the status and progress.

Apart from triggering the right actions, the underlying database is also the source of a broad monitoring and reporting.

(4) Monitoring and reporting

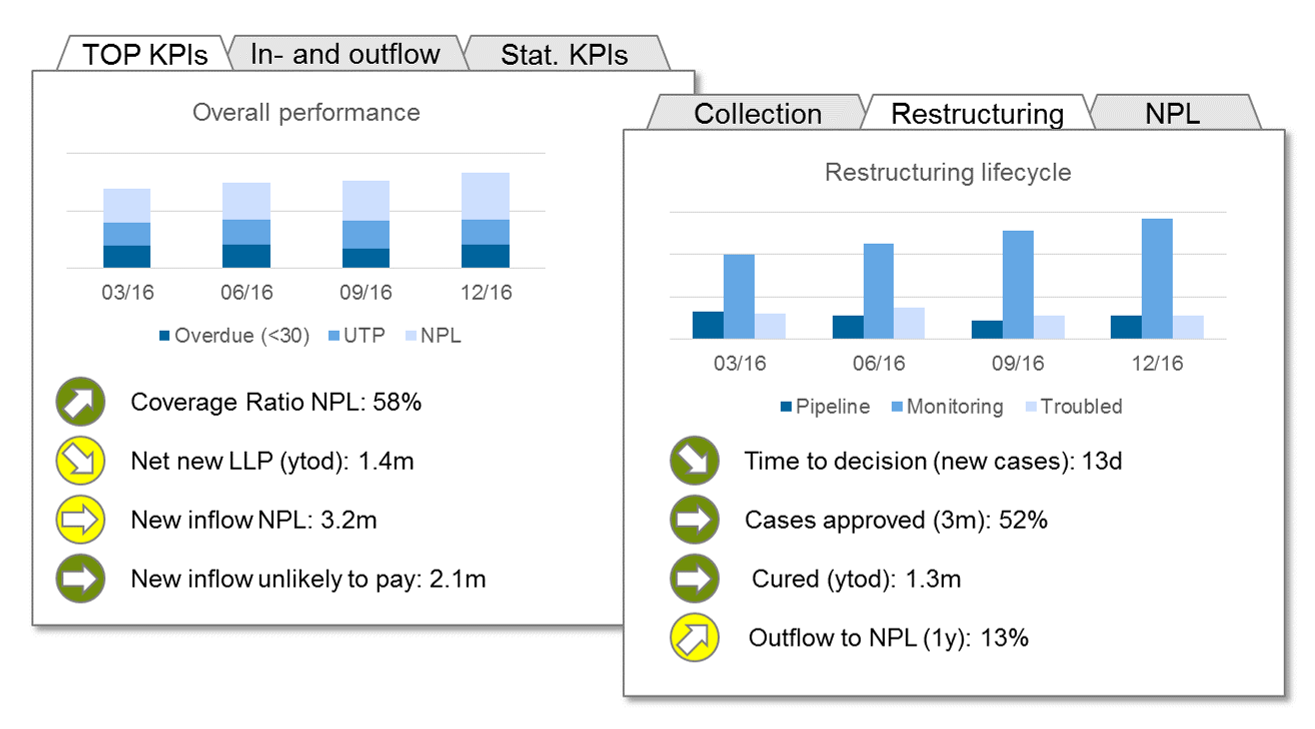

Reporting consistently links strategy / strategic targets with operational performance management. A fully-fledged reporting accordingly includes the following components:

- Management reporting for top management, heads of divisions, etc.: managerial view, i.e. evolution of the portfolio value, volumes, inflow and transitions, recovery rates, aggregated performance for internal and outsourced activities; accounting view (e.g. impairment needs)

- Operational performance reporting (unit / team leaders, heads of divisions for their direct reports): specific KPIs for the area of responsibility (e.g. for call center amount collected, number of calls per agent, promises-to-pay taken / kept)

- Monitoring effectiveness and quality of the rules: using decision trees, rules to automatize categorization requires a frequent back testing and calibration of the rules to achieve the best possible quality / discriminatory power. The same applies to the effectiveness of different treatment strategies. A simple example is the percentage of approved restructurings vs. the “eligible cases” suggested by a decision tree: a number that is too low is an indicator for tightening the rules and vice versa.

For setting up an informative reporting, banks need on the one hand a proper IT platform and on the other hand aligned top KPIs (in our view including evolution of NPV) and a value driver logic that links top KPIs with operational KPIs.

Conclusion

Obviously, the ability to manage problematic portfolios in an effective and timely way will be crucial for many banks in the near future in order to relaunch profitability and comply with the expectations of the regulators.

To do so, banks have to be diligent in designing a comprehensive approach, which should define both the credit management strategy and a coherent operating model. This will require significant investments to build dedicated infrastructures, acquire skills and know-how, review the organizational design and define governance models.

Key to the necessary changes is the mindset: credit management is not the source of bad loans, but if it is done well, it will create additional value for the bank. We consider using the portfolio NPV as a main performance indicator beneficial for this mind change.

2 responses to ““The sooner, the better”: a pro-active approach to NPL management”

Dmitry Chudakov

Nice approach, but not as easy to implement in practical terms. Institutional aspects of the efficient secondary market for loan trading, collaterals disposal as well as credit life data banks are the key. Applicable for fully standardized and small credit exposures.

Dr MacJohn Geraldo

The recommendations outlined are quite realistic and should be adopted to salvage bad loans crisis situations.