Initial situation

Following the financial crisis, however, the funding behavior of banks shifted from unsecured towards secured transactions, leading to a decline in the number of transactions relevant for index calculation. Ultimately, a series of LIBOR scandals led to the start of the IBOR reform process.

Subsequently, the regulators created the Benchmarks Regulation (EU 2016/1011) to establish an appropriate code of conduct for the creation of benchmark indices (e.g. IBORs) within the European Union.

Faith in a successful reformation of IBORs, however, diminished over the last few years: therefore

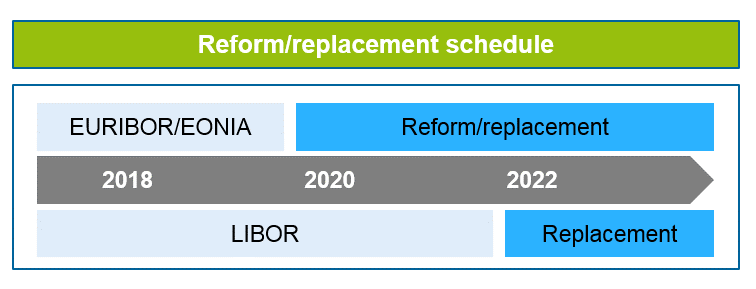

- the schedule for LIBOR replacement has been communicated: the FCA has announced it will no longer support the supervision of LIBOR after the end of 2021

- EONIA will be replaced at the end of 2019

- EURIBOR is to be reformed in accordance with the requirements stated in the Benchmark Regulation by January 2020—failing that, it will be replaced

Figure 1: Benchmark rate replacement schedule

Figure 1: Benchmark rate replacement scheduleThe replacement of the EONIA benchmark with ESTER (Euro Short-Term Rate) has recently been decided, whereas the EURIBOR reformation or replacement scenarios are still under discussion. With regard to LIBOR, some replacement candidates have already been defined, e.g.:

- SOFR (Secured Overnight Financing Rate) for USD LIBOR

- SONIA (Sterling Overnight Interbank Average) as an unsecured rate for GBP LIBOR

While the existing benchmarks are available for different maturity structures, all replacement options will solely be overnight rates. Term rates are under intense discussion and it is not guaranteed that in future, such rates will become available on the market. Due to different maturity structures and the hedged nature of some future rates, a one-to-one transition may therefore not be possible.

Implications of the transition

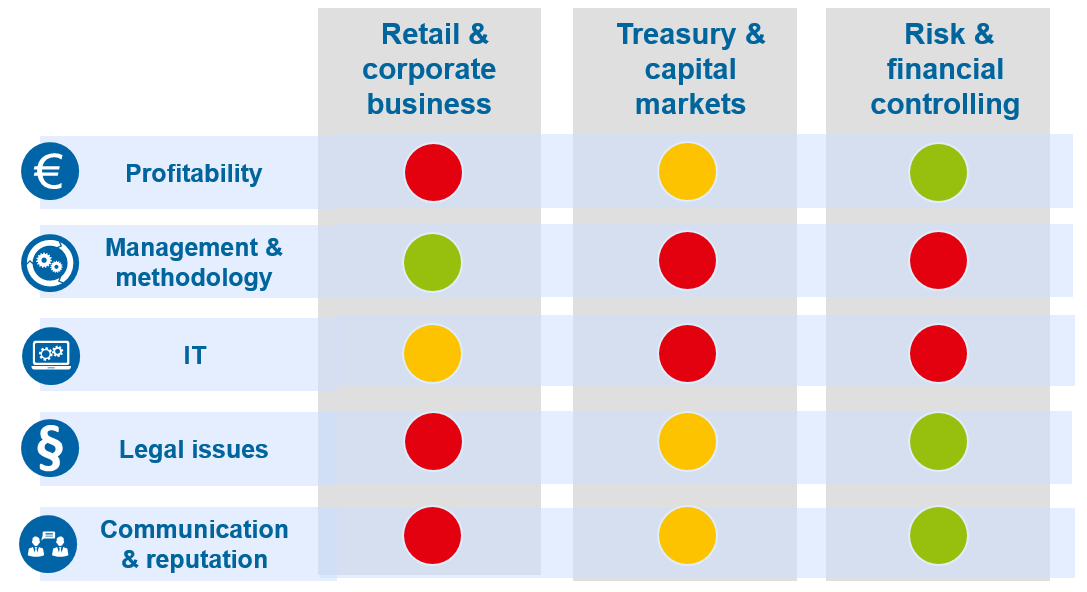

The IBOR transition has a significant impact on almost all bank segments. We anticipate impacts on profitability, management and methodology, IT, legal issues as well as communication and reputation dimensions. Figure 2 shows the extent to which each bank segment is affected by these dimensions.

Figure 2: Implications of the transition

Figure 2: Implications of the transitionFirst simulations reveal significant P/L effects, mainly due to unfavorable fallback clauses and hedging costs. Project costs are also likely to be high, especially in complex IT environments.

We will now take a more detailed look at the five dimensions.

Profitability

Profitability is particularly impacted if unfavorable fallback solutions take effect (e.g. in cases where the last available IBOR is applied to the remaining lifetime of a transaction), since they would likely impact on the asset side of the balance sheet with its loan portfolios more than on the liability side. Therefore, an open interest position needs to be hedged, which can lead to high costs depending on the market situation. This effect will be particularly severe if the transition falls into a period of rising interest rates and a steepening maturity structure, whereby the optionality gains value for the customer. Different transition dates for different products can also lead to open positions.

Measured in terms of their profit contribution, customer business as well as treasury and capital markets are likely to be hardest hit. In this context, a fair allocation mechanism for transition costs is crucial for preventing disincentives.

Management and methodology

The transition to new interest rate benchmarks triggers changes in a large number of bank management and steering processes and methodologies. Among others, the following areas are affected:

- Profitability/risk: embedded options, basis spreads, and arbitrage opportunities lead to significant uncertainties concerning earnings and capital. Existing derivative portfolios may have to undergo severe restructuring.

- Accounting: in addition to necessary book value adjustments and transition calculations for the income statement, which are triggered by changed discount curves, hedge relations may lose their effectiveness and would then have to be de-designated.

- Product pricing: in an environment of as yet illiquid markets or unavailable market data and a lack of industry consensus, spreads need to be readjusted.

- FTP: basis curves, spreads and indirect costs need to be adjusted.

All in all, the transition of the benchmark interest rate index calls for immediate action to establish a robust and effective steering framework in the light of a fundamentally changing market. The following paragraphs provide a deep dive into the impact on risk management and FTP.

Risk management

The substitution of benchmark indices gives rise to earnings and capital risks, which in the former IBOR world, would have seemed too improbable to even be considered. In line with IRRBB, the risk types that arise can be attributed to embedded options and index basis spreads.

Option risk: two of the more common options embedded in IBOR-linked fixed income products and triggered by the termination of the benchmark interest rate index are the following:

- Fallback option: upon termination of the benchmark index, the customer has the right to switch to a fixed rate which equals the latest fixing of the discontinued index plus the contractual spread. This option is extremely attractive to all rational players, since a simple swap transaction on the customer side will result in a windfall equal to the difference between the swap rate and the frozen fixing. Unhedged, the exercise of this option poses tremendous risks to profitability in an environment where interest rates can go nowhere but up. On the equity side, the capital requirements for a fixed-rate loan are affected proportionally to its duration. These requirements will rise sharply when the option is exercised and the loan’s interest rate changes from floating to fixed.

- Early redemption option: upon termination of the benchmark index, the customer has the right to pay off the loan in full or to return the security to the issuer at the outstanding amount without incurring a penalty. We expect such an option particularly to be exercised if banks were to offer unattractive spreads on the successor index and the customer were to make use of this opportunity to refinance—note that it is not unconceivable that institutional customers will exploit arbitrage opportunities by offsetting attractive against unattractive spreads.

Basis risk: this risk is particularly prevalent if IBOR and the successor index coexist for a certain period. More precisely, if the benchmark indices in hedge relationships (whether economic or designated) of the hedged item and the hedging instrument do not match, an index-index basis is opened. Because of different index properties, this basis may vary considerably.

Option and basis risk affect both earnings and capital from the point of view of interest income, costs for the dissolution of hedging transactions, undesired P&L volatility due to the dissolution of designated hedge relationships as well as illiquid derivatives markets.

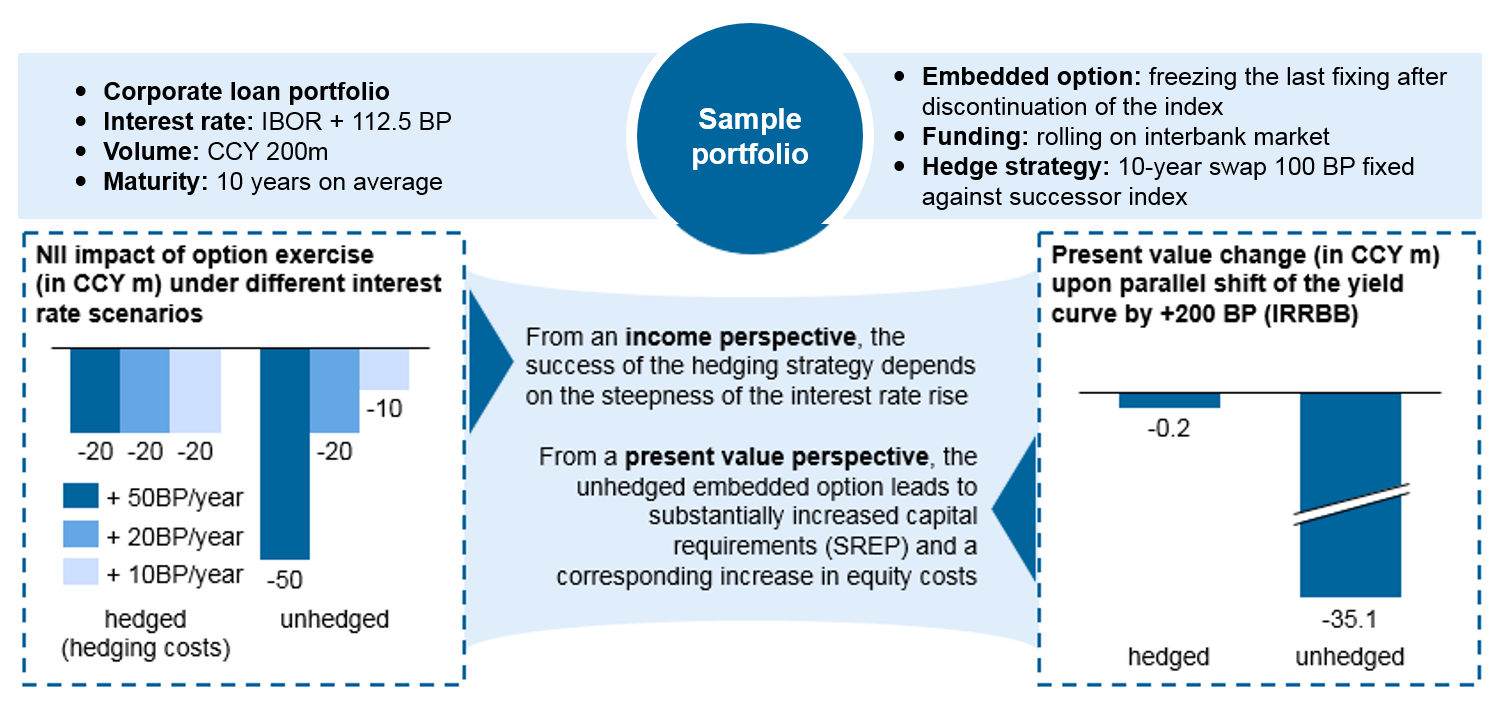

Corporate loan example: in the following example of a corporate loan portfolio, the effects of the embedded fallback option on earnings and present value become evident. In addition, it can be deduced that the success of hedging strategies through the use of swaps to convert the frozen interest rate to a variable rate depends on the future interest rate development.

Figure 3: Corporate loan portfolio

Figure 3: Corporate loan portfolioFunds Transfer Pricing

Due to the new benchmark curves, all FTP components must be reviewed. First, the base rate must be migrated from the current 3M IBOR reference rate to new overnight rates. The possible basis change (overnight versus 3M swaps) leads to a corresponding change in the individual funding spread components. The credit spread of the IBOR panel banks so far has also been implicitly taken into account (e.g. for 3M). Problems arise when determining the FX spread (e.g. future cross-currency swap with secured (e.g. USD) and unsecured (e.g. GBP) basis). Parameters from modelling (e.g. exercise probabilities for options, core deposits, etc.) will change due to the IBOR transition, therefore changes in “indirect” costs are also expected. Furthermore, effects from new basis and option risks need to be taken into account.

IT

IT will be one of the strongest cost drivers of a transition process, as many systems in several departments are affected. The biggest challenges lie in the requirement for parallel operations during the transition period as well as in the difficulties for posting systems to process daily postings when only overnight rates are available.

IPD, which may not be very well documented, can also be very costly. In this case, for example, the possible transition from forward to backward fixing and multi-curve valuation must be taken into account.

Legal issues

Legal aspects relating to fallback solutions for legacy contracts are particularly complex. First, a huge effort is required to obtain transparency on the different fallback solutions in different contracts, since a comprehensive contract database is often unavailable.

A common fallback clause states that the last available IBOR fixing is to be used for as long as there is no new fixing available. What was originally introduced as a fallback solution in cases where, for technical reasons, the interest rate is not available at short notice, can have an impact on a bank’s profitability, as shown above.

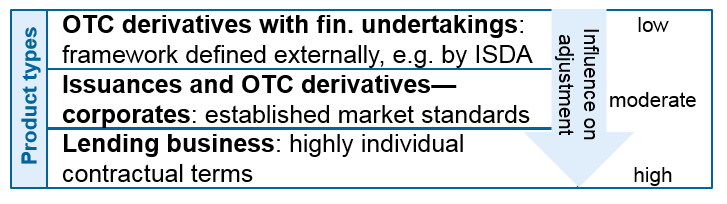

While we expect a high degree of standardization for OTC derivatives (especially those in line with ISDA standards), loans are considerably more individual. It is likely that a general legal solution will be adopted for retail loans; corporate loans may need to be renegotiated individually. A robust fallback solution for corporate loans is therefore the most pressing legal issue from the individual bank’s point of view.

Figure 4: Product types

Figure 4: Product typesCommunication & reputation

Amending fallback clauses for legacy contracts as well as pricing loans with potentially higher customer add-ons to the benchmark rate on account of the shift to a risk-free rate, constitute reputational risks. Furthermore, basis and option risks can impact the profitability of market divisions and treasury if they are not treated separately in the cost allocation process. A comprehensive internal and external communication strategy is therefore essential. External communication must be coordinated with other banks and associations. Due to possible P/L effects, lobbying also plays an essential role within the communication strategy.

Solution approach

We currently see the following key success factors:

- Appointment of a senior executive as project sponsor and establishment of a centralized project management

- Timely creation of transparency on the impact on profits, methodology and bank areas

- Early planning due to the high degree of complexity

- Early setup of stakeholder communication

- An agile process to ensure the flexibility of the content while adhering to a fixed deadline

We therefore recommend setting up a two-stage IBOR transition project, which is coordinated through flexible project management:

- Impact analysis: creating transparency on the impact on the different bank divisions and prioritizing the required project modules and/or working packages for further implementation

- Concept and implementation stage: conceptual design and implementation of the project modules, e.g. modification of fallback clauses, ensuring integrability of overnight rates into the systems, adjustment to funds transfer pricing, etc.

In parallel, early involvement in committee work and the initiation of stakeholder communication are key factors in following industry discussions, monitoring and influencing the developing market standards and best practices.

To tackle this issue, zeb has developed an IBOR readiness check toolbox, which covers the products and functional areas concerned and enables a financial institution to

- gain transparency about the impact levels for each product / functional area—including which topics have already been defined or are still being discussed,

- derive and prioritize a need for action and solution options in a structured manner,

- derive structured work packages and cost estimates,

- plan the implementation.

Waiting for relevant decisions on the exact future of reference rates is not an option for banks, given that many implementation activities require sufficient preparation time.