(Digital) accessibility for financial services providers

The European Accessibility Act (EAA) lays down binding EU-wide accessibility guidelines and requirements for products and services that the member states are obliged to implement and transpose into national law by June 28, 2025.

Agility in the modern corporate world

Agility is more than just the application of agile methodologies. It is a comprehensive approach aimed at enhancing the adaptability of individuals, teams and organizations as a whole.

Agile leadership

The key lever for a successful and future-oriented alignment of modern organizations is agile leadership. That’s because changes on the outside always require changes on the inside of organizations and of the people working in them, too.

AI

The term “artificial intelligence” (AI) refers to technologies that emulate and support human abilities such as seeing, hearing, analyzing, deciding and acting

Alternative asset classes

In principle alternative assets include all assets that do not fall into the traditional liquid asset classes, such as securities, money market instruments and derivatives. Alternative asset classes include also cryptocurrencies, antiques and art and other physical assets.

Ambidexterity

Ambidexterity, originally derived from Latin, denotes the ability to use both the right and left hand equally well. In an organizational context, it describes an organization’s capacity to address two seemingly contradictory challenges simultaneously.

APIs

Data exchange between the bank and authorized third parties (e.g. financial institutions, fintech start-ups and companies) is enabled via application programming interfaces.

Asset management

Asset management refers to the financial service of managing assets by means of financial instruments with the aim of increasing the invested assets.

Asset tokenization

Tokenization describes the process of creating a digital representation of the rights to an asset as a fungible token (usually a security token) or a non-fungible token (NFT).

Bancassurance

Bancassurance, as a strategic sales collaboration between banks and insurance companies, has firmly established itself as a promising business model in Europe.

Banking-as-a-Service (BaaS)

Banking-as-a-Service (BaaS) is an advanced business model in which financial institutions make their banking services available to third parties via APIs (application programming interfaces). These third parties can be other institutions or non-banks that want to expand their product range to include financial services.

CBDCs

CBDCs are issued by the central banks and represent a deposit claim against the central bank. A distinction can be made between wholesale CBDCs for use by commercial banks and retail CBDCs open to all economic agents.

Change management in IT

As part of digitalization, change management is an important step towards becoming fit for the future and meeting customer demands. The reason: a high median age of the workforce, increasing regulatory pressure and the simultaneous development of the “old” and “new” world often push financial services providers ato their limits in terms of organizational structures and staff.

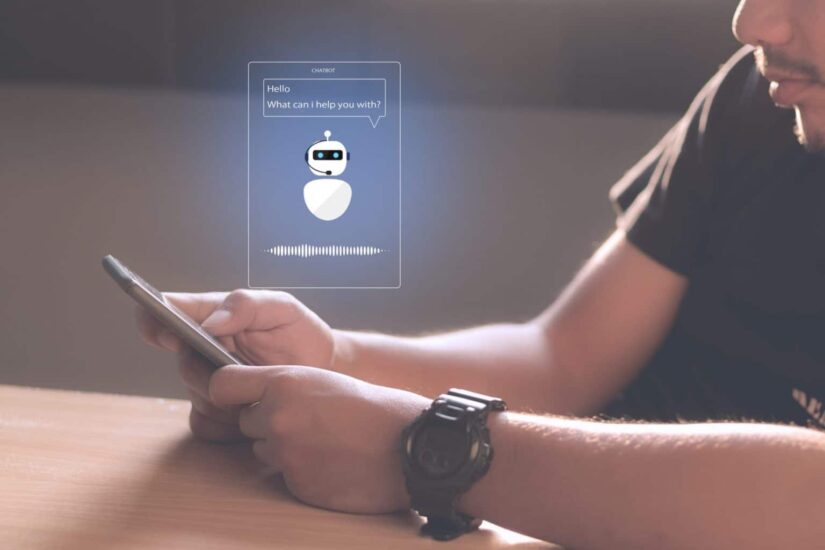

Chatbots and voicebots

Chatbots and voicebots enable dialog-based interaction between bank and customer. This topic becomes even more interesting when the technology is further developed using AI.

COVID-19 crisis

The COVID-19 pandemic and its consequences are often compared to the global financial crisis of 2008/09 – this time, however, the cause is exogenous.

Cryptocurrency

A cryptocurrency is a digital asset that enables cashless payments independent from intermediaries or is used for investment purposes.

Crypto fund unit

A crypto fund unit is a share in investment funds or in individual share classes of an investment fund that is registered in a crypto securities register.

Crypto mining

Crypto mining refers to the process of verifying blockchain transactions as proof-of-work and receiving rewards in the form of native tokens of the respective blockchain.

Crypto assets: advisory services on and portfolio management

Advisory services on and portfolio management of crypto assets describe the offer or provision of personalized investment recommendations to clients.

Crypto assets: placement

The business of placing crypto assets describes the marketing of crypto assets to buyers on behalf or for the account of the provider or a party affiliated with the provider.

Crypto assets: provision of custody and administration on behalf of clients

Crypto custody includes the secure safekeeping, storage, and control of crypto assets or the means to access such assets for customers, possibly in the form of private cryptographic keys used to hold, store, or manage crypto assets on behalf of others.

Crypto assets: provision of transfer services on behalf of clients

Transfer services on behalf of third parties include the transfer of digital assets in a distributed ledger network (DLT network) from one wallet address to another on behalf of natural persons or legal entities.

Crypto asset orders: transmission and execution on behalf of clients and exchange of crypto assets

The transmission and execution of orders for third parties and the exchange of crypto assets for fiat money or other crypto assets play a critical role in the crypto markets, enabling private and institutional investors to efficiently invest in cryptocurrencies

Crypto securities register

A crypto securities register is a register based on DLT technology for electronic securities as defined in the German Electronic Securities Act (Gesetz über elektronische Wertpapiere, eWpG).

Crypto security

Crypto securities are a new form of issuance for bearer bonds via a DLT-based crypto securities register.

Crypto wallet

A crypto wallet (or wallet for short) is a physical device or software that generates, secures, and stores public and private keys. Users can send and receive tokens and view their account balance via the wallet.

Data analytics

“Data analytics” refers to technologies whose primary focus is on analyzing, explaining and deriving insights from data.

dApp

dApps are DLT-based software applications that make smart contracts usable through a GUI.

Decentralized finance

Decentralized finance describes decentralized systems that use software protocols to enable financial transactions between users without the involvement of financial intermediaries such as banks..

Design Thinking

Design Thinking is a process-oriented and iterative innovation method that helps develop new products, services and customer experiences.

Digital assets

Digital assets are digital representations of assets that are not issued or guaranteed by any central bank or public authority and do not have the legal status of currency or money.

Digital asset services: the glossary for the digital asset world

Our MiCAR glossary series provides you with a detailed overview of the key terms and services that the regulation focuses on.

Digitale assistants

Digital assistants are an important building block for optimizing the digital customer interface. Software solutions that recognize the specific needs of a user and initiate a defined solution process are referred to as digital assistants.

Digital euro

The ECB’s deliberations on the digital euro to date can be summarized in the basic idea of “digital cash”. In addition to physical cash and electronic fiat money, the ECB wants to introduce a digital euro as central bank money with payment functions for everyday use via smartphone.

Diversity in the financial services industry

The Diversity Charter, an initiative to promote an appreciative working environment free of prejudice, defines seven core dimensions of diversity that reflect the individual personalities of different people.

DLT

Distributed ledger technology (or “DLT” for short) refers to a decentralized database that stores information in blocks that are distributed across a computer network

Ecosystems

An ecosystem is a network of several providers – orchestrated by the ecosystem’s orchestrator – who orient their services towards customer needs. An ecosystem can focus on one or more customer needs.

Electronic stock

The German Financing for the Future Act (Zukunftsfinanzierungsgesetz, ZuFinG) enables the DLT-based issuance of electronic stocks.

End-to-end organization (E2E)

E2E organization enables financial services providers to focus on customers and their needs while ensuring effective and efficient service delivery. The transformation towards such an E2E organization affects almost all areas of a financial services provider and goes far beyond a mere reorganization.

ESG

ESG – these three unassuming letters not only stand for environmental, social and governance, they cover an entire development that will change our society, the economy and our behavior and will thus also have a massive impact on banking.

Holacracy

In an ever-changing business world, companies are looking for innovative approaches to work more adaptably and efficiently. Holacracy has established itself as one of these innovative models aimed at improving collaboration, overcoming traditional hierarchical structures and paving the way for agile organizations.

Intelligent process automation

Intelligent process automation refers to the transformation of business processes that previously could not be automated because they involved the processing of unstructured data and therefore had to be performed manually. Complex process steps can be automated by integrating AI.

IRRBB

The extent of maturity transformation between the fixed-interest periods on both the asset and liability side has a significant influence on the level of interest rate risk in the banking book (IRRBB).

Metaverse

Broadly speaking, Metaverse stands for an evolved, immersive internet, in which the boundaries between the physical and digital worlds become increasingly blurred as a result of various software and hardware innovations. Consequently, Metaverse platforms are virtual ecosystems for social interaction as well as commercial and leisure activities

MiCAR glossary series

Our glossary for the digital asset world provides you with a detailed overview of the key terms and services that the regulation focuses on.

MiCAR unveiled: our comprehensive guide to crypto asset regulation in the EU

The introduction of the MiCAR will create a comprehensive regulatory framework at EU level that will uniformly regulate the market infrastructure for digital assets in one of the world’s largest domestic markets, replacing existing national regulations on an EU-wide basis.

New Work

New Work means that work is becoming flexible in terms of time, space and content/methodology. New Work goes beyond changes in premises and aims to further develop hierarchical organizations in such a way that innovation skills, innovation output and the adaptability of companies are increased.

Non-fungible token (NFT)

Non-fungible tokens (NFTs) are unique digital assets that can be issued and traded via DLT.

Open banking

Open banking refers to the practice of securely sharing financial data with customer consent. Data exchange between the bank and authorized third parties (e.g. financial institutions, fintech start-ups and companies that currently do not necessarily have to be active in the financial sector) is enabled via APIs.

Open finance

Almost 10 years after the publication of PSD2 as a major milestone in the development of open banking and many years of muted development falling short of initial expectations, dynamics have recently increased and reached broadly relevant levels.

In the shorter term, the capturing of daily banking income pools is expected to be a major driver of development; in the medium term, a broadened regulation, especially the Financial Data Access (FIDA) Framework, is expected to further promote open finance.

Platforms

In essence, digital platforms are online marketplaces that bring together supply and demand in a similar way to a real marketplace. Banks or companies offer services and compete on platforms.

Portals

Portals basically represent access points to any type of digital service. However, it would not be sufficient to reduce the role of a portal to a mere access channel

RegTech

Regtech is a portmanteau of the terms “regulatory” and “technology” and is considered a sub-division of the fintech industry, although in direct comparison it is still in the initial stage.

Robo advisor

The terms “robo advice” and “robo advisor” have been used for the past few years to describe digital asset management and its providers. In the future, robo advice will be part of financial services providers’ standard offering.

SACR

The standardized approach to credit risk (SACR) is one of the two possible approaches to determine risk-weighted exposure amounts in accordance with the Capital Requirements Regulation (CRR).

Security tokens

Security tokens are securities that represent a digital twin of an asset.

Smart contracts

Smart contracts are contracts implemented using DLT systems that automatically execute transactions when certain triggers occur, enabling digital transaction processing.

Stablecoins

Stablecoins are are DLT-based tokens whose value is pegged to other assets. Looking back, the launch of the crypto stablecoins Tether in 2014 and USDC in 2017 marked the beginning of stablecoins.

Staking

Staking of digital assets is becoming increasingly relevant as a DeFi service and is opening up new opportunities, particularly for financial institutions offering crypto services.

Tokenization

Tokenization describes the process of creating a digital representation of the rights to an asset as a fungible token (usually a security token) or a non-fungible token (NFT).

Travel Rule for digital asset transfers

The Travel Rule is a set of international regulations that requires financial institutions and digital asset providers to exchange data on the originators and beneficiaries of digital asset transfers. Digital asset transfers require compliance with the Travel Rule regulations!

Wallet

A crypto wallet (or wallet for short) is a physical device or software that generates, secures, and stores public and private keys. Users can send and receive tokens and view their account balance via the wallet.