State of the banking industry

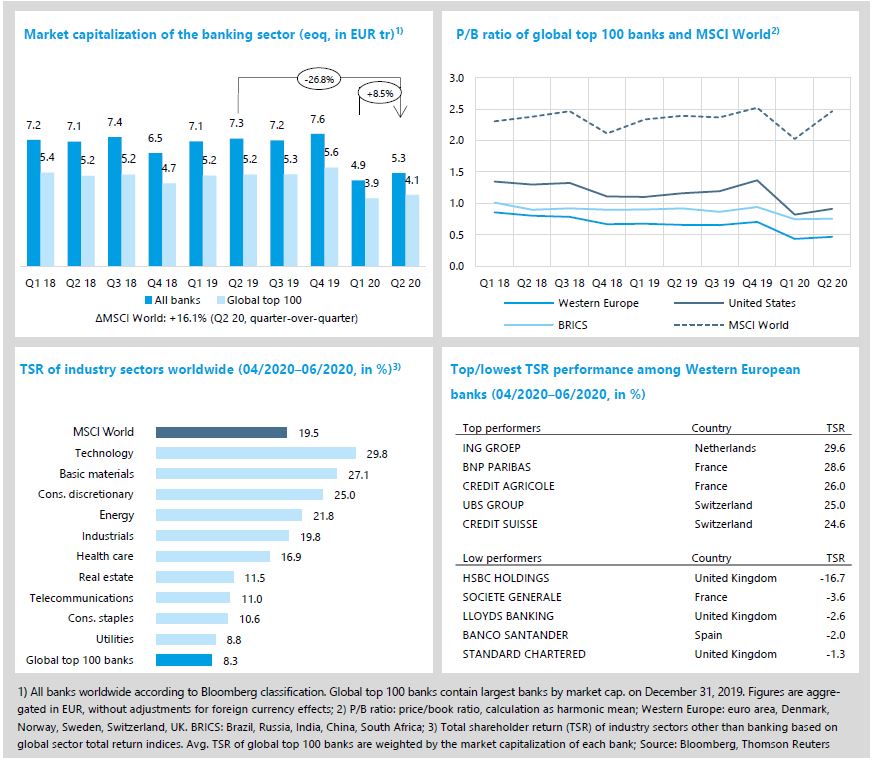

- Global top 100 banks profited the least of the overall stock market recovery in Q2 2020 (TSR +8.3% qoq compared to the MSCI World with +19.5%).

- Average P/B ratios clearly deteriorated across all regional clusters—U.S. banks took the hardest hit with -0.45x qoq and are now also below the important hurdle of 1.00x (Western European banks 0.50x).

After a very good year 2019, the COVID-19 pandemic blindsided capital markets. As a consequence of the global “shutdown”, stock markets collapsed across all regions in the first quarter of 2020. In the second quarter, stocks for most industries saw a speedy recovery and exhibited a strongly v-shaped development as first steps have been taken to restart the economy. The stock price for most banks missed out a strong rebound, reflecting the impact of falling interest rates and increasing credit risks.

- Banks’ market capitalization collapsed in March 2020 (Q1: all banks -35.1% qoq, global top 100 banks’ -31.1% qoq) but regained some ground in the second quarter with +8.5% qoq and +5.0% qoq, respectively. Still, global top 100 banks’ market capitalization would need to rise by another +38.1% to reach pre-crisis levels of EUR 5.6 tr (value end of Q4 2019).

- Average P/B ratios clearly deteriorated across all regional clusters. U.S. banks took the hardest hit with -0.45x compared to Q4 2019 and are now also below the important hurdle of 1.00x. Western European banks even dropped below 0.50x.

- Looking at industry sectors, global top 100 banks profited the least of the overall stock market recovery in Q2 2020 with a TSR recovery of +8.3% qoq compared to the MSCI World with +19.5% qoq or Technology with +29.8% qoq.

- UK banks among the low performers reflecting the strong impact of the pandemic on the UK which is likely to be the worst affected country in Europe. HSBC had the worst TSR performance of Western European banks as they additionally had to put restructuring plans on hold and U.S.-China trade tensions affect the bank disproportionately.

Economic environment and key banking drivers

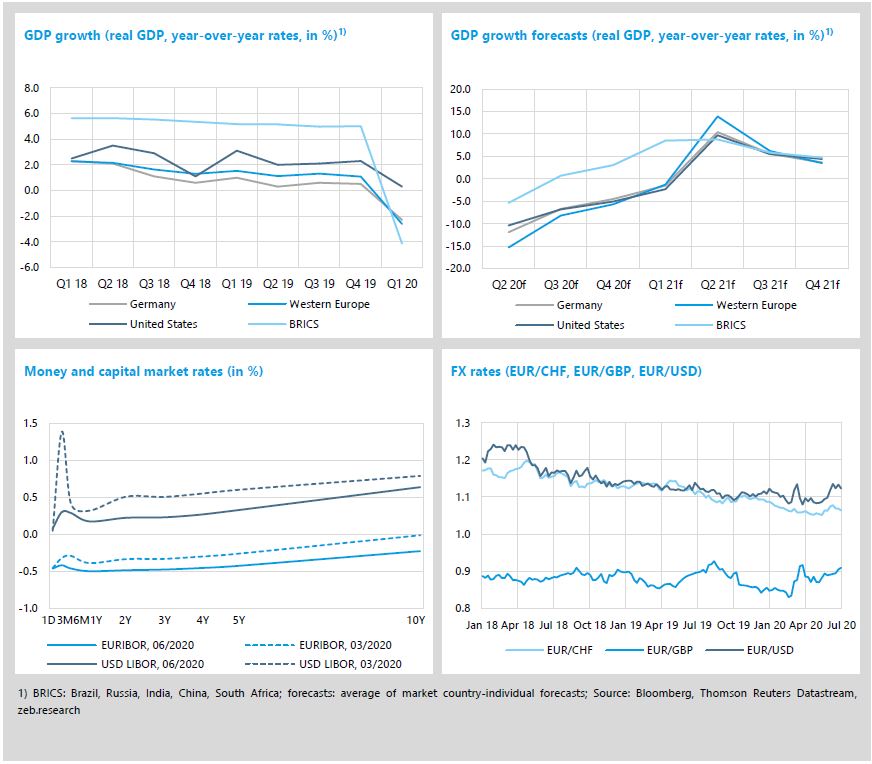

- Economic growth in Q1 2020 took a historic dive, with growth forecasts for Q2 2020 and subsequent quarters pointing towards a further deepening of the worldwide recession caused by COVID-19-related lockdowns.

- Low yield environment entrenched as major central banks responded to the COVID-19 pandemic with significant rate cuts and quantitative easing.

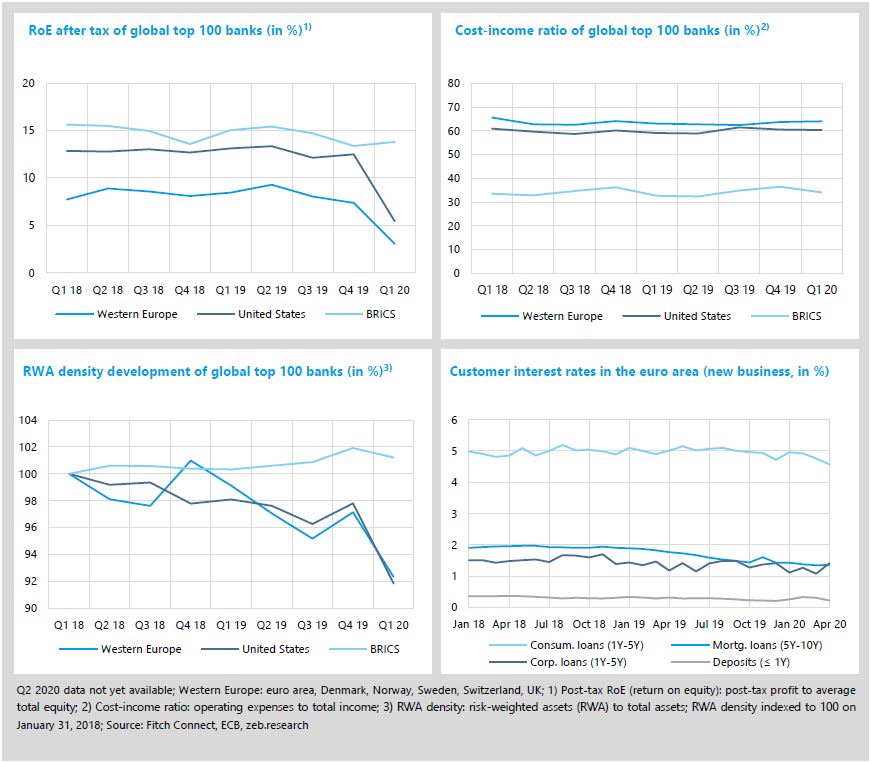

- European and U.S. banks were hit substantially by the current pandemic with profits collapsing in Q1 of 2020 due to skyrocketing loan loss provisions.

The economic environment banks are operating in remained very challenging in Q2 2020. Actual economic growth in Q1 2020 took a historic dive, with growth forecasts for Q2 2020 and subsequent quarters pointing towards a further deepening of the worldwide recession caused by COVID-19-related lockdowns. Furthermore, the low yield environment entrenched—the U.S. Federal Reserve responded to the COVID-19 pandemic with two significant rate cuts in March and the ECB kept its deposit facility rate at -0.50%, but significantly extended their asset purchase programs to support the European economy.

- Looking at current GDP growth forecasts, Q2 2020 will see the most significant yoy drop during this crisis and the economy will only slowly recover in subsequent quarters but will remain below previous years’ GDP growth figures across all regions except for the BRICS countries. High yoy rate forecasts for Q2 2021 must be read in conjunction with the very low growth expectations for Q2 2020—a full GDP recovery to pre-COVID-19 levels will likely last until the end of 2021 or even 2022.

- The U.S. Fed lowered the target for the federal funds rate to a range of between 0.00%-0.25% equal to the target range that was effective from 2008 to 2015 as a response to the Global Financial Crisis. Although the U.S. yield curve is not inverse anymore (Q4 2019), it stands at an extremely low level with all rates below 0.65%. The euro area yield curve shifted downwards even further and flattened slightly, with the 1Y rate dropping -11bp and the 10Y rate -21 bp compared to Q1 2020.

- Driven by more intense coronavirus outbreaks and harsher political intervention in the U.S. and UK, the USD and GBP lost some ground against the EUR—EUR/USD increased by +2.4% qoq and +3.4% since the end of February when the first cases were observed in the U.S. and Europe. Against the GBP, the EUR even gained +2.7% qoq and +8.9% since the end of February.

European and U.S. banks were hit substantially by the current pandemic with profits collapsing in the first quarter of 2020. At first glance, this might be some kind of a surprise as COVID-19 only impacted Europe and the U.S. around mid of March. However, the main drivers behind this decline are not lower earnings or higher operative costs but skyrocketing loan loss provisions. Aside from that, RWA density declined as total assets jumped in the first quarter driven by higher new loan business and credit lines drawn by corporate customers.

- Under the pressure of the crisis, the profitability of European and U.S. banks plummeted. In Europe, the already low average post-tax return fell from 7.4% in Q4 2019 to just 3.1% in Q1 2020, whereas U.S. banks’ relatively good pre-COVID-19 return shrank from 12.5% to 5.5%. As indicated by stable cost-income ratios, significantly higher loan loss provisions were the main driver here.

- The RWA density declined strongly in Q1 2020. This development was clearly driven by higher new loans and drawn credit lines which lead to higher total assets. However, risk-weighted assets increased only slightly but significant increases due to the COVID-19-induced new credit cycle are expected with a time lag towards the end of 2020.

- Looking at customer interest rates, the rates for corporate loans increased in a first step from 1.08% to 1.42% at the end of April. Despite a relatively stable and low overall yield environment, we expect further increases across all loan types in the future—higher risk costs but also an improving relationship between banks and their customers should further affect credit pricing.

Special topic

COVID-19 and the impact on European banks’ capitalization

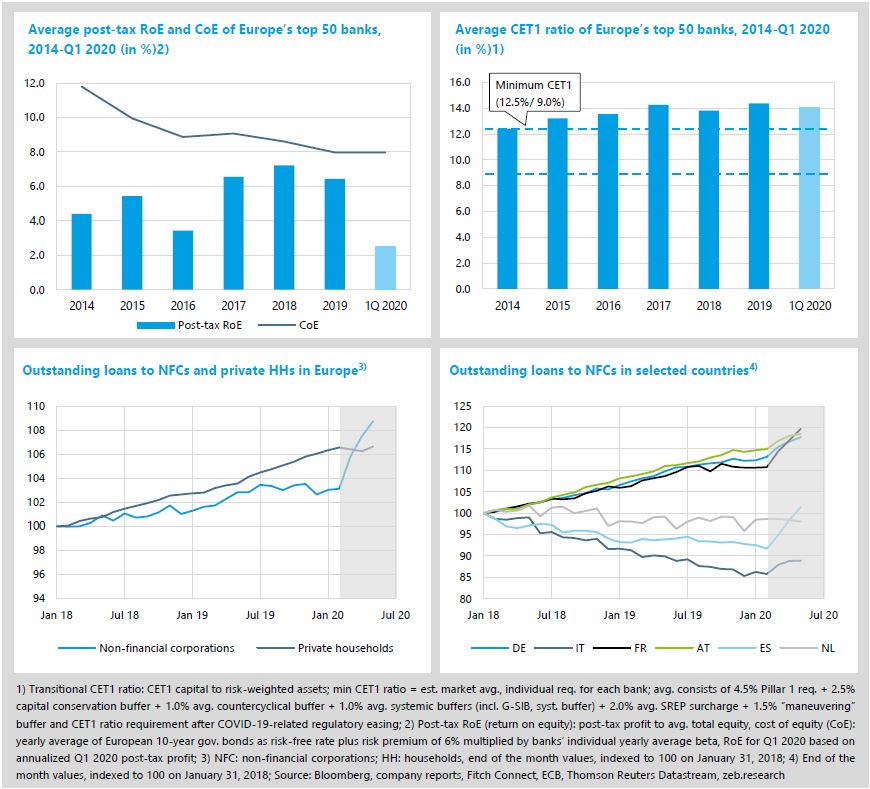

- Although Europe’s banks have become more resilient over the last years, they have to cope with low profitability and significant impacts on capitalization due to the COVID-19 pandemic.

- Even if first signs are already visible, the effect on banks’ capitalization will only become effective within the next 18 to 24 months.

- In the medium to long term, the credit quality of issued loans will be the key driver of RWA inflation and significantly increasing LLPs could eat into banks’ capital cushions.

The banking sector has been in the midst of the worst crisis since the financial crash of 2008/2009. Although Europe’s banks were substantially more resilient when the COVID-19 pandemic broke out than when they entered into the global financial crisis, they have to cope with significant impacts on profitability and capitalization. Even if first signs are already visible, in particular the effect on banks’ capitalization will only become effective within the next 18 to 24 months

Already suffering substantially from low yields and high regulatory costs, Europe’s banks entered the COVID-19 crisis with a persistent profitability problem—struggling to achieve post-tax RoEs above their costs of equity for years. Furthermore, the slight improvements from 2014 to 2019 were mainly driven by declining loan loss provisions (LLPs) and decreasing litigation charges, but not by advancements to the operating result. For 2020, published Q1 results of Europe’s top 50 banks indicate worse news on the horizon as the average RoE dropped down from 6.5% end of 2019 to just 2.5%. In anticipation of COVID-19 impacts to the real economy, banks significantly increased their credit risk provisioning in the quarter (~+200% yoy) leading to overall very weak results with post-tax profits declining by -66% yoy on average. Looking ahead, we simulated the development of the LLPs over the next 18-24 months for the corporate and retail banking business for each of the top 50 banks in a medium and a severe recession scenario. As a result, in the event of a severe recession, total LLPs in Europe could increase by up to 500 % on average compared to 2019. For some banks, the safety cushion that robust profitability could provide to fend off losses is already thin and such sharp increases in the costs of risk that will ultimately result from the COVID-19-induced credit cycle will have a negative impact on bank’s capital cushions.

The good news, Europe’s 50 largest banks have strongly improved their capital ratios and become more financially resilient in the past years. At the end of 2019 the average overall CET1 ratio of Europe’s 50 largest banks stood at an all-time high at 14.4%—clearly above the average regulatory and market minimum requirement of 12.5%. Further “breathing room” has been provided by regulators which have eased capital requirements substantially in response to the COVID-19 crisis. In order to support banks to extend their credit business and to provide the real economy with the required funds to successfully navigate through the COVID-19 pandemic, regulators explicitly allowed banks to temporarily operate below the level of capital requirements defined by Pillar 2 guidance and the capital conservation buffer.[1] Overall, the “COVID-19 capital requirements” are on average around 3.5%p lower than end of 2019.

Nevertheless, first (small-scale) effects of the crisis can also be found in Q1 20 figures as the average CET1 ratio decreased by 0.4%p as several banks reported higher new loans and drawn credit lines. In the upcoming months, additional RWAs (risk-weighted assets) in line with new business volumes and drawing of credit lines will lead to further decreasing ratios. First indications are visible when analyzing the developments of outstanding loans in the euro area. Since the end of February, following the weeks of lockdown in Europe, corporate loan demand increased markedly and loans to non-financial corporations rose to end of May by +5.5%—mainly driven by medium-term loans (1Y to 5Y). Although the amount of outstanding corporate loans evolved differently in recent years, nearly all major European countries showed growing loan volumes since February 2020. Spain (+10.6%) and France (+8.1%) are among the countries with the strongest inclines in overall corporate loan growth, followed by Germany (+4.1%) and Italy (+3.6%). Private households, however, shield away from new consumer credit loans which in turn was compensated by continuously growing mortgage business, leading to end of February values of total loans to households at the end of May again. So far, a trend reversal of COVID-19 lockdown-induced loan growth cannot be observed.

In the medium to long term, however, changes in the credit quality of banks’ customers will become the key driver behind further RWA inflation and will put significant pressure on CET1 ratios.[2] The current practice of credit moratoria provides certain customers with much needed alleviation to successfully navigate through the crisis. For banks, however, this translates, at least for some cases, into a time lag where the assessed credit quality of a customer will still be affected, but later in time. In cases where external ratings are employed in RWA calculations, the time lag of rating adjustments has also to be considered. For internal models to evaluate customers’ credit quality, the calculation methodologies are mainly based on corporates’ balance sheet and P&L data, which are also available after a time delay. In the meantime, rather manual rating overrides by banks based on ad-hoc information could affect RWA calculations. Therefore, the whole RWA impact only becomes fully effective after all government aid measures for corporates and SMEs have expired and relevant parameter shifts based on new and sound data are observable.

All in all, European banks’ capital ratios are expected to substantially suffer in the future from credit losses but also the in-built procyclicality of RWA inflation. Upcoming Q2 and Q3 numbers will primarily be driven by volume-induced increases in RWAs. Later into the year and into 2021 the credit quality of issued loans will be the key driver of RWA inflation and significantly increasing LLPs could eat into banks’ capital cushions. The overall impact on banks’ capitalization remains to be seen and is, of course, highly dependent on the severity and length of the economic downturn as well as the extent and effectiveness of the government aid measures. Transparency about the potential impact of the COVID-19 pandemic on the capital ratios is key for bank managers and regulators to derive adequate course of action. In this context, sophisticated simulations of COVID-19 impacts on B/S and P&L items could be a supportive tool for bank’s credit risk management but also regulators and governments to assess the stability of the financial system.

For more information and details on this topic, please read our new European Banking Study 2020 and stay tuned for our upcoming extract of our study in August, which will further analyze the drivers of RWA inflation and its impact on capital ratios for the largest 50 European banks. Please visit our page #zebFutureProof where we present detailed additional information, materials and specific offers.