Objective

The Committee wants to create comparability regarding capital requirements for operational risk by defining a consistent measurement for all banks. Hereby the new SMA is in line with the standardization and homogenization in context of Basel IV. Especially, the high degree of freedom, currently implied in AMA, shall be reduced. Nevertheless, the measurement for operational risk is said to be bank-specific and the simplicity of current standardized approaches shall be preserved.

Approach

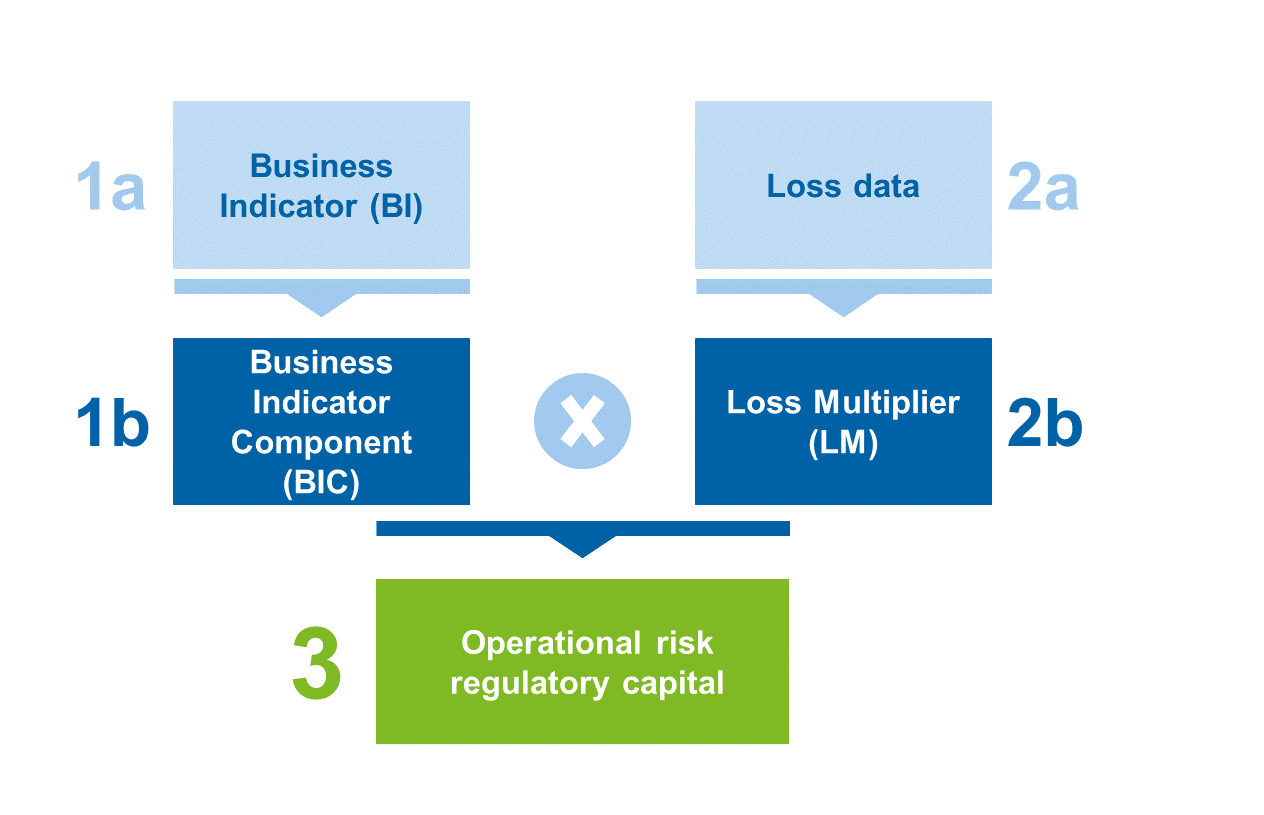

Two components are multiplied by each other in order to calculate operational risk capital requirements:

- Business Indicator Component (BIC)

- Loss Multiplier (LM)

The Business Indicator Component (BIC) again is derived from the Business Indicator. The Loss Multiplier is based on observed historical bank-specific operational losses. The figure below shows the calculation logic:

Figure 1: Calculation logic of new SMA

Figure 1: Calculation logic of new SMA1) Business Indicator (BI) and Business Indicator Component (BIC)

The Basel Committee on Banking Supervision conducted a study to analyze various explanatory variables of operational risk. The business indicator showed the highest explanatory power and was chosen as a risk indicator for the new SMA.

The Business Indicator replaces the current variable gross income used in the simple BIA and STA approaches. Three components, that are calculated from P&L positions as well as balance sheet positions, are added up to the Business Indicator:

- Interest, Lease and Dividend Component

- Services Component

- Financial Component

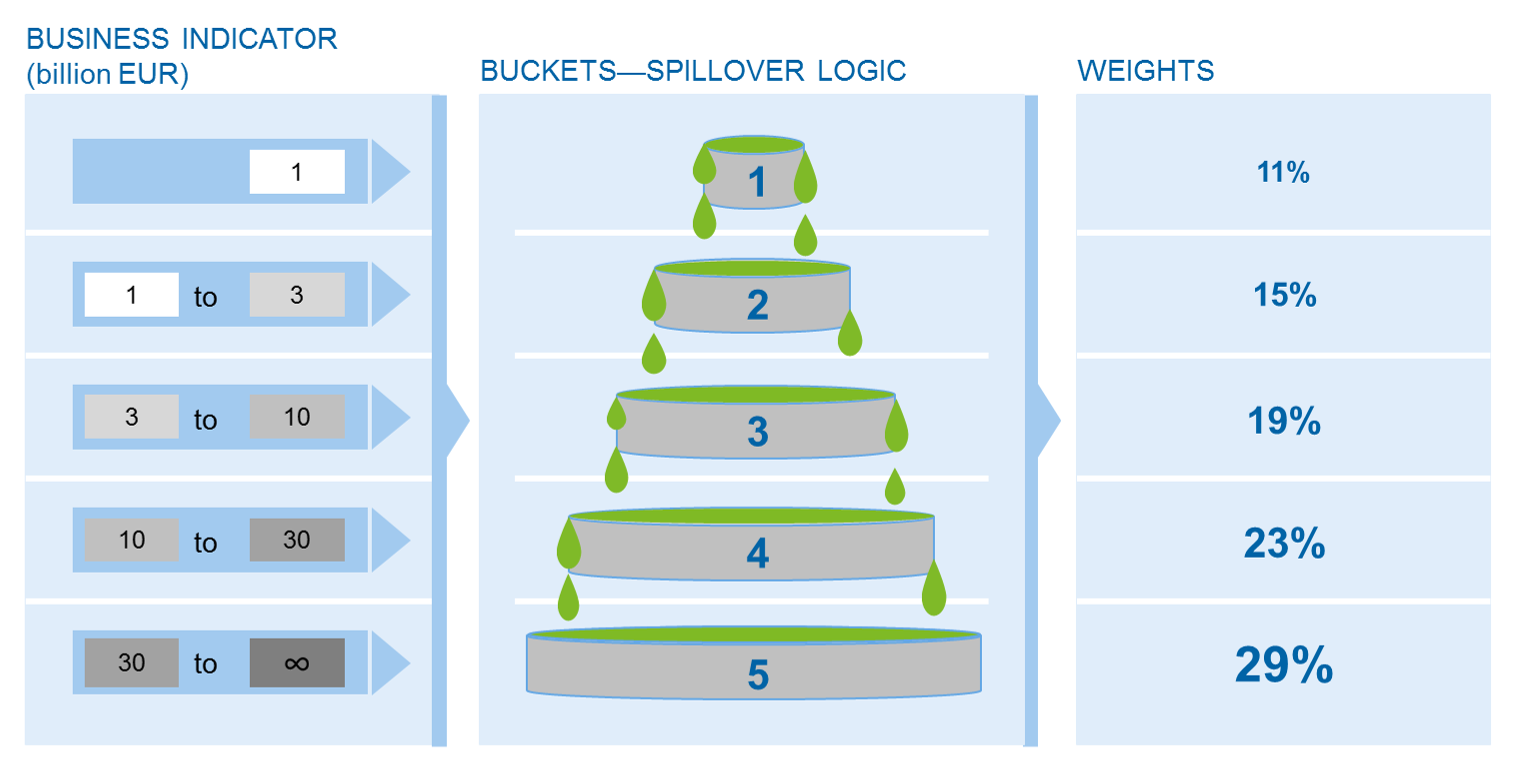

Size categories (buckets) for the Business Indicator are derived by a spillover logic. A weight is assigned for each bucket. The weight increases with each bucket. The Business Indicator Component itself is the weighted sum of business indicator buckets. The following figure illustrates the spillover logic:

Figure 2: Spillover logic for Business Indicator Component

Figure 2: Spillover logic for Business Indicator Component Example: Assuming a Business Indicator of EUR 5 bn, EUR 1 bn are assigned to bucket 1 and are weighted with 11%, additional EUR 2 bn are weighted with 15% in bucket 2 and the remaining EUR 2 bn (EUR 5 bn – EUR 1 bn – EUR 2 bn) are weighted with 19% (bucket 3). The Business Indicator Component results in EUR 0.79 bn (1 × 11% + 2 × 15% + 2 × 19%).

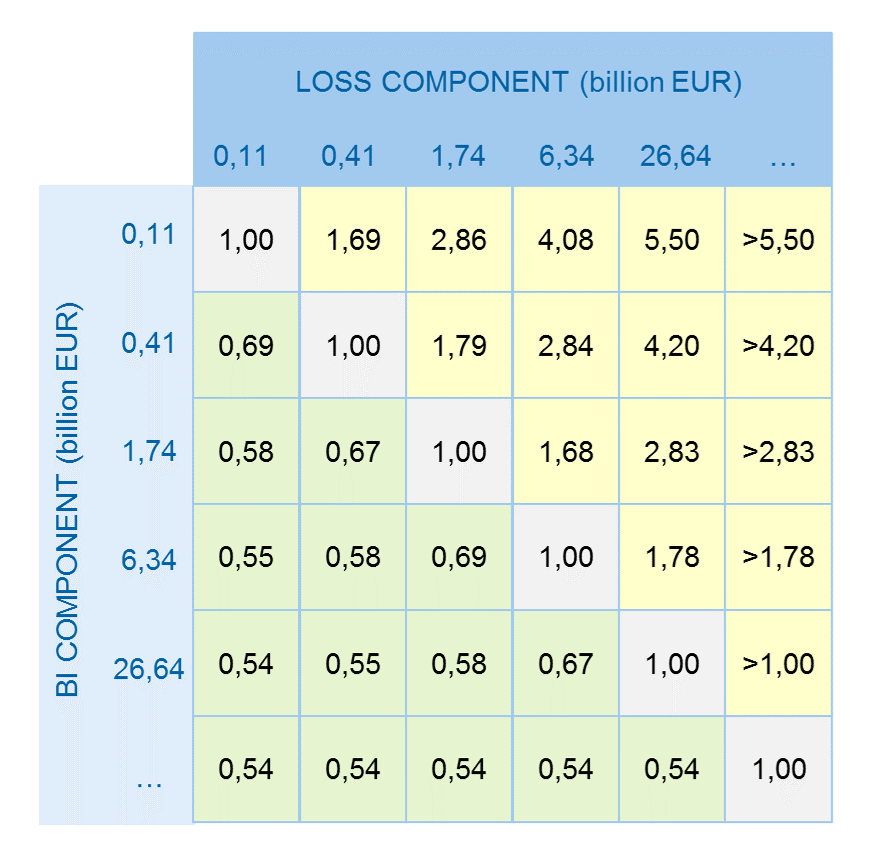

2) Loss data and Loss Multiplier

Banks with a Business Indicator greater than EUR 1 bn (bucket 2–5) must estimate a Loss Multiplier. The Loss Multiplier is calculated based on bank-specific historically observed operational loss data. Therefore, the Basel Committee demands 10 years of good-quality loss data. For a transition period, at least 5 years of loss data are expected.

The Loss Component is calculated from average annual operational losses, but high losses (losses greater than EUR 10 m and losses greater than EUR 100 m) are weighted higher. By weighing major loss events higher than average events, it is taken into account that the loss distribution of two banks with the same average operational loss can differ a lot (fat tails). Thus, major loss events result in higher operational risk capital requirements.

According to the Basel Committee, the Loss Multiplier takes the value 1 if the bank has observed market average operational losses (Loss Component and Business Indicator take the same value). In case of above average losses, the multiplier is greater than 1 and thus leads to higher operational risk regulatory capital (and vice versa). The following figure shows the connection between Loss Component and Business Indicator Component:

Figure 3: Loss Multiplier as relation of Loss Component and BI Component

Figure 3: Loss Multiplier as relation of Loss Component and BI Component3) Capital requirements

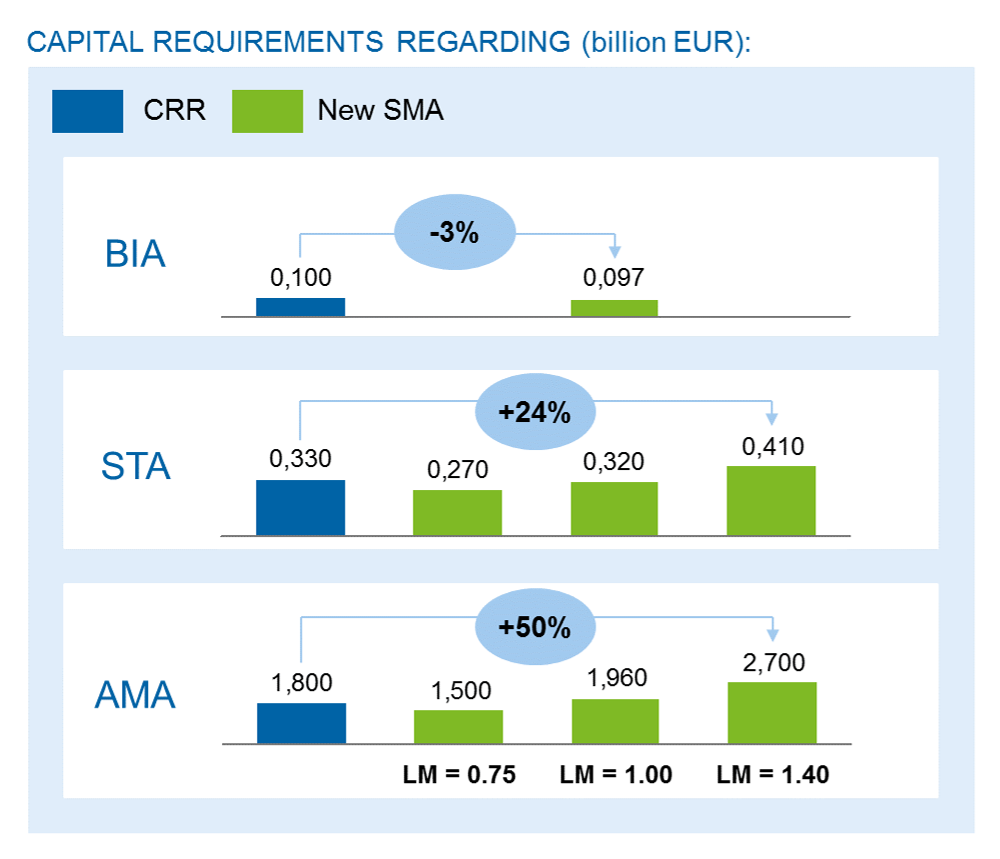

Banks of bucket 1 (Business Indicator up to EUR 1 bn) calculate operational risk regulatory capital solely by the Business Indicator Component (the Loss Multiplier is assumed 1). The capital requirements for banks of buckets 2 to 5 are calculated by multiplying Business Indicator Component and Loss Multiplier.

Impacts

Rather lower capital requirements are expected for BIA banks. Although the calculation of the BIC is more conservative than the calculation of gross income according to BIA (e.g. fewer degrees of freedom for netting of income and expenses), the weight for the BIC in bucket 1 is only 11%, whereas the currently applied weight for BIA is 15%; i.e. much higher than the proposed weight of 11%.

AMA banks are most likely faced with higher capital requirements. One reason is obvious: the standardized approach doesn´t allow to account for bank-specific characteristics “in such an optimized way” as it was possible with the bank-specific models of AMA.

The following figure shows capital impacts for exemplary banks (BIA bank, STA bank, AMA bank):

Figure 4: Examples of impacts on operational risk regulatory capital depend on current approach and Loss Multiplier (LM). Three scenarios for the Loss Multiplier are shown: below average operational losses (LM=0,75), average operational losses (LM=1) and above average operational losses (LM=1,4)

Figure 4: Examples of impacts on operational risk regulatory capital depend on current approach and Loss Multiplier (LM). Three scenarios for the Loss Multiplier are shown: below average operational losses (LM=0,75), average operational losses (LM=1) and above average operational losses (LM=1,4)Regulatory need for action

Three steps need to be taken for the implementation of the new SMA:

- The current calculation for operational risk regulatory capital is compared with requirements of the new SMA to identify gaps of the current approach (GAP analysis). Banks currently using standardized approaches will most likely face little problems for the calculation of the Business Indicator Component, because the positions used for the Business Indicator are almost identical with positions used to calculate gross income according to BIA and/or STA.

- The Business Indicator buckets are derived in a sample calculation. In single cases, only an exemplary calculation will prove whether a bank has to calculate the Loss Multiplier, too (i.e. in case the Business Indicator of the bank is greater EUR 1 bn).

- The identified need for adaption is to be implemented. In doing so, the technical units (especially management of operational risk, risk controlling, accounting and regulatory reporting) are needed as well as the IT unit which must implement SMA technically (e.g. data interfaces, calculation and reporting engine).

Business management

One main objective of the AMA was the estimation of capital requirements according to the individual, bank-specific risk situation. The implementation of a standardized approach that only focusses on past internal loss events seems to reduce the need for a proactive risk management.

A proactive risk management pursues the avoidance of risk events and furthermore the occurrence of internal losses. With forward-looking methodologies, e.g. on the basis of KRIs, risk assessments and scenario analyses, the view in the rear mirror will be complemented by a forward-looking view through the front window.

The main impact factor of the new SMA is the Loss Multiplier. Thus, a proactive management, which reduces operational risk events, leads to a lower loss multiplier and therefore to lower capital requirements. As extreme events have a high impact on the loss multiplier, also typical operational risk with low frequency and high impact should be managed proactively.

Summary

The SMA replaces all three existing approaches for the estimation of operational risk regulatory capital. The SMA is based on two components (Business Indicator Component and Loss Multiplier). For bigger banks, bank-specific internal operational losses are considered.

Impacts on small banks are manageable. Higher capital requirements are especially expected for AMA banks. Furthermore, the implementation of SMA will be more complex for AMA banks compared to BIA banks and STA banks.

Proactive management of operational risk remains important as it allows to avoid internal losses which again affect the loss component of the new SMA.

3 responses to “Capital requirements for operational risk – new SMA”

Sani

The explanation has simplified the technical aspect of this approach. However, more granularity on the illustration is required to enable a comprehensive understanding of the SMA.

Thank you

Leo Sea

Dear Andre & Maike

Good explanation the BIC. However, the same explanation for the Loss Multiplier would be helpful for a better understanding of the new SMA regulatory capital charge. Ideally, a figure with buckets, spillover logic and weights would perfect

Thank you again

regards

Leo Sea

Pingback: Basel IV: approach for determining the capital charges - BankingHub