Introduction

The most relevant feedback received from the banking sector concerned the inadequate measurement of IRRBB using a standardized approach as it does not take the heterogeneous and complex nature of the different institutions into account. Consequently, the standardized approach is intended as a fallback solution and/or for the development of an industry-wide benchmark. while, IRRBB is to be managed under Pillar 2 with substantially revised principles including the following key adjustments:

- Greater guidance on the requirements for IRRBB management including more detailed interest rate scenario presets, stricter modeling assumptions for deposits and the compulsory consideration of behavioral optionalities / embedded options (Principles 4, 5 and 6).

- Extended disclosure requirements including the disclosure of modeling assumptions and changes in the economic value of equity (EVE) under each interest rate scenario (Principle 8).

- Transparent identification of “outlier banks”: supervisors can require institutions to take specific measures if the maximum loss of EVE under one of the interest rate scenarios exceeds 15% of their Tier 1 capital (Principle 12).

Authorities expect financial institutions to implement BCBS #368 by 2018. In fact, banks are required to fully implement the standards in 2017 if a) the financial year of the respective institution ends on December 31, 2017 and b) BCBS #368 is made (inter-)national or law. Unlike the EBA guidelines on IRRBB, the Basel standards are not yet legally binding. However, the BCBS standards and the EBA guidelines need to be regarded as complementary indicating a potential harmonization. In fact, the EBA has reserved the right to adjust its guidelines.

Revised IRR principles as overarching guidelines

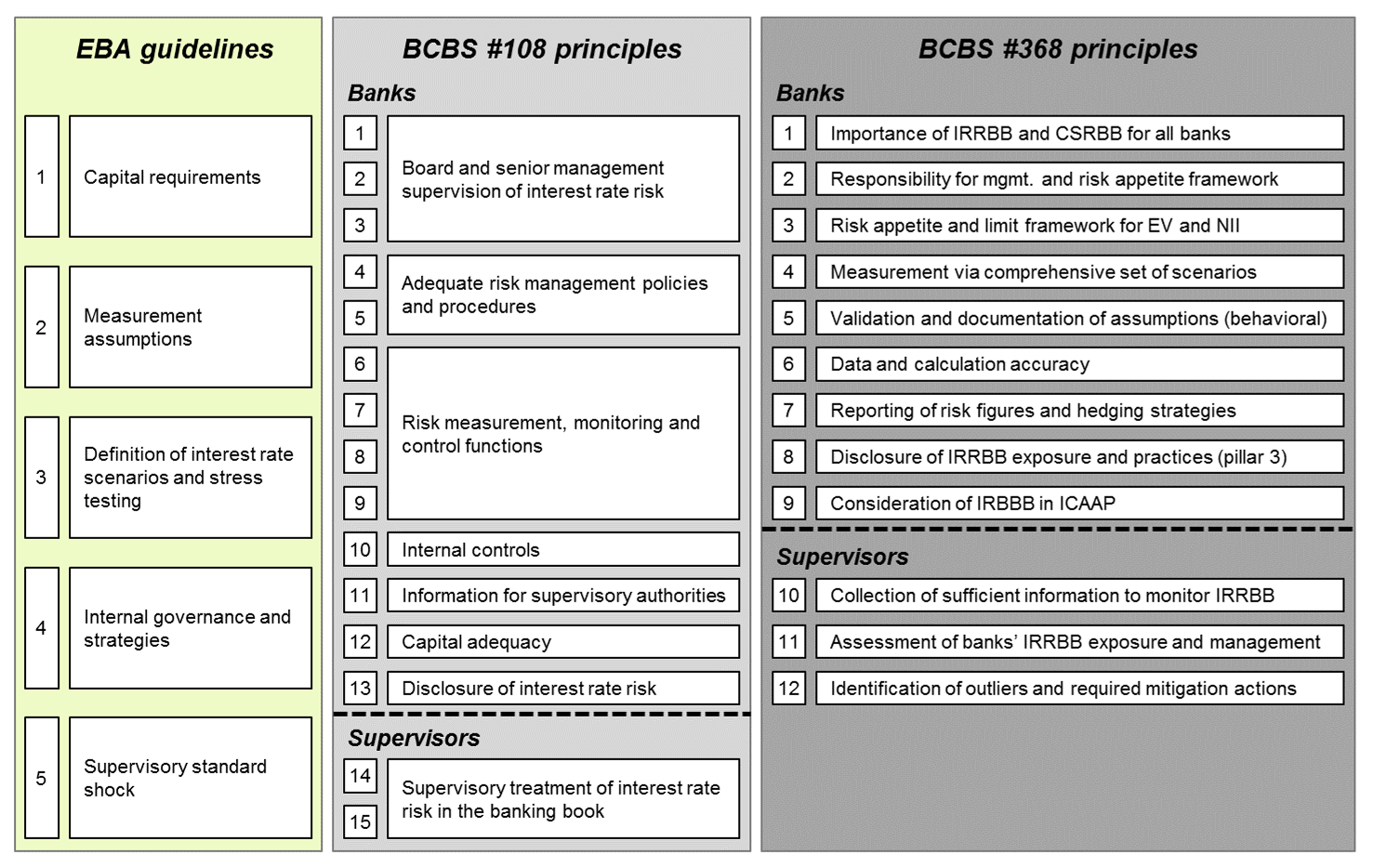

In order to put the revised principles into a contextual relationship with previous standards (BCBS #108) and the EBA guidelines, the requirements specified in all three documents are illustrated below:

The discrepancies between the EBA guidelines and BCBS standards are apparent and require further consideration. The main differences can be summarized as follows:

- Principle #1: In contrast to the EBA guidelines, BCBS #368 does not exclusively focus on IRRBB but rather it explicitly specifies requirements to identify, assess, monitor and control the Credit Spread Risk in the Banking Book (CSRBB).

- Principle #4: Clarification, extension and detailed definition of interest rate shock and stress scenarios as well as specifying the requirement to measure the effects of adverse spread and volatility adjustments. Moreover, the need to consider highly concentrated markets (which could affect the liquidation of positions), the measurement of asymmetrical effects of negative interest rates on assets and liabilities and reverse stress testing are addressed.

- Principle #5: The behavioral and explicit interest rate options need to be estimated and modeled for different interest rate scenarios. Moreover, non-maturity deposits(NMD) have to be analyzed for identifying the individual proportion of core deposits of a bank.

In order to determine potential changes in modeling assumptions caused by external factors (e.g. changing interest rate environment, macro-economic environment, etc.), banks are required to estimate potential changes of modeling assumptions under different interest rate scenarios and different macro-economic developments. Furthermore, regular validations (at least on an annual basis) of key behavioral assumptions and adequate documentation of the requests above are required.

- Principle #6: Clear and stringent specifications on the adequacy of measurement systems, entered data and governance to validate applied IRRBB measurement methods. The measures to be applied range from simple and static models to more sophisticated and dynamic measurement methods.

- Principle #8: Extensive disclosure requirements are specified and include qualitative and quantitative components:

- qualitative disclosure: description and thorough explanation of the underlying assumptions as well as measurement, management, monitoring, controlling and potential mitigation strategies of IRRBB

- quantitative disclosure: economic and earnings-based risk figures for the prescribed interest rate shock scenarios as well as the average and longest repricing maturity for NMDs underlying the calculation need to be disclosed

Principles for supervisors:

- Principle #11: Evaluation of the IRRBB management framework, internal measurement systems (IMS), economic and earnings-based IRRBB exposure and capital adequacy for IRRBB. The evaluation is performed at an institutional level and compared to peer group benchmarks.

- Principle #12: Performing a “materiality test” to determine “outlier banks” with a maximum change in EVE not exceeding 15% of Tier 1 capital. Furthermore, authorities can perform additional materiality tests but need to publish the criteria used for identifying an outlier bank. If the evaluation of the Internal Measurement Systems or the consideration of IRRBB within the Internal Capital Adequacy Assessment Process (ICAAP) are considered deficient, authorities are entitled to impose mitigating actions. These include a potential request to reduce IRRBB or to increase the Tier 1 capital within a specified period, purport criteria for adjusting the IMS of an institution or to inform the respective institution about the requirements to improve the risk management capability. Ultimately, authorities may request that the standardized framework is applied if their evaluation indicates deficiencies in the internal models of bank.

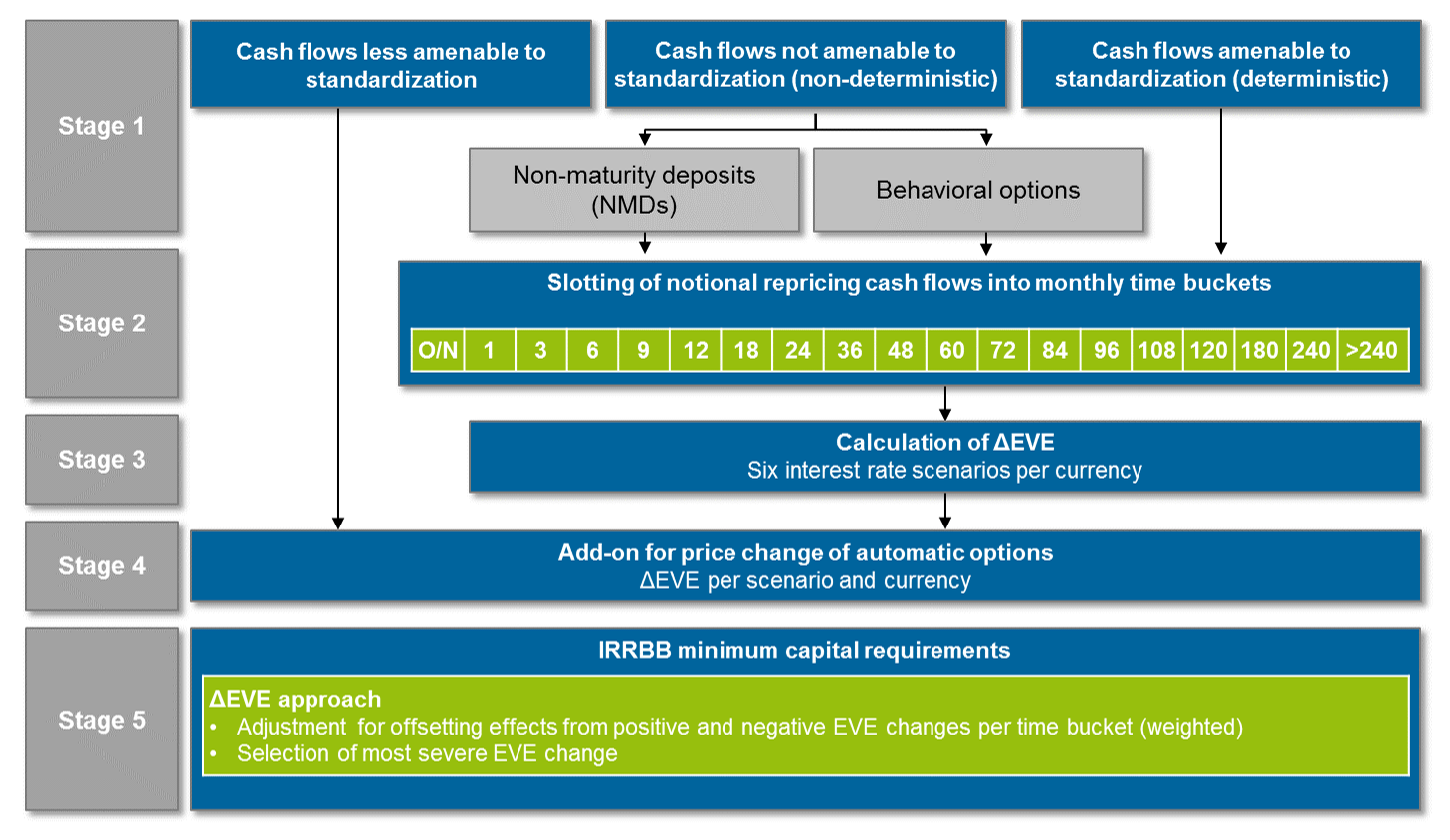

The standardized framework as “fallback” solution and benchmarking tool

Although the standardized framework proposed in BCBS #319 is not applied for the calculation of minimum capital requirements, a revised and simplified approach is nevertheless included in the final standards. The supervisors may use this approach as a benchmarking tool and can request banks to apply the standardized framework in case of severe deficiencies in the internal models. As shown in the figure below, the procedure to calculate IRRBB in the final standardized framework is based on the initial proposal in the BCBS #319 consultation paper.

The main differences between the initial and final version of the standardized framework can be summarized as follows:

The Basel Committee initially proposed the introduction of a standardized framework under Pillar 1, but reacted on the industry’s feedback, suggesting that a standardized framework does not sufficiently take the complexity and heterogeneity of banks’ business models into account. Thus, the final standards on IRRBB provide a standardized framework as a fallback solution under Pillar 2 that supervisors can request banks to use. Alternatively, banks may also choose to calculate the interest rate risk exposure voluntarily by means of the standardized framework.

The standardized framework has also been simplified. The IRRBB calculation is now exclusively based on the change in EVE under the supervisory interest rate scenarios and no longer includes a calculation of changes in net interest income (NII).

Finally, the treatment of behavioral assumptions (non-maturity deposits and embedded customer optionalities such as early prepayments of loans) has become more lenient and thus has a significant impact on risk calculation:

- The assumptions on customers’ behavior regarding changes in the conditional prepayment rate in different supervisory interest rate scenarios are less extreme compared to the consultation paper.

- The assumptions for determining the core deposits allow for a larger and more realistic volume of core deposits from NMDs.

The standardized framework consists of five stages as illustrated below:

Conclusion

The publication of the final standards resolves uncertainties and reveals the current demand for action. In fact, the implementation deadline has been set to 2018. Thus, a road map based on gaps in complying with regulatory requirements should be determined shortly. A timely implementation is of utmost importance as supervisors can request mitigation actions or additional capital demands in case of non-compliance.

According to the principles for supervisors (10, 11 and 12) and the requirements in the Supervisory Review and Evaluation Process (SREP), the determination of bank-specific capital requirements in Pillar 1 will be implemented soon.

The shift of focus—from the standardized approach under Pillar 1 to the internal measurement of IRRBB under Pillar 2—is accompanied by several tasks. Institutions will need to carry out a range of proprietary analyses including a cost-benefit analysis arising from entering IRRBB as well as a gap analysis revealing the level of compliance with the principles. If the IMS of an institution does not fully comply with the principles and is considered deficient, supervisors can impose remediating actions and force institutions to use the standardized approach, raise additional capital, reduce the IRRBB exposure (e.g. through hedging), tighten modeling assumptions within the IMS or improve the existing risk management system. There is reason to believe that the standardized approach needs to be reported in order to establish benchmark comparisons. Thus, the need to implement the standardized approach as well as to regularly apply the standardized measurement becomes evident.

zeb recommends adequate and timely elaboration of how to handle BCBS #368. The implementation process should begin as soon as possible due to the impact on institutions mentioned above. In order to professionally deal with BCBS #368, zeb offers its rich expertise regarding the IRRBB requirements set out by BCBS and the new EBA guidelines for the management of IRRBB and supports banks in the process of both the conceptual and technical interpretation and implementation of requirements. For the technical implementation, zeb provides field-tested software for the integrated management of Interest Rate Risk in the Banking Book—zeb.control.risk–ALM (formerly known as zeb.integrated.treasury manager)—which allows for an economic and earnings-based perspective on interest rate risk while taking additional EBA and BCBS requirements into account.