How is the current market environment changing the way forbearance is handled?

Business conditions are challenging: economic uncertainties, elevated interest rates, high cost burdens and industry-specific crises – for example in real estate or in the SME sector – are leading to a noticeable increase in financially distressed borrowers and more cases where forbearance is used as an instrument.

A similar trend could already be observed during the financial market crisis: banks responded to their customers’ financial difficulties with concessions such as repayment suspensions/reductions or interest rate adjustments in order to relieve liquidity constraints and at the same time avoid having to set aside risk provisions for themselves. However, this practice often led to a distortion of the actual risk situation, particularly when measures were implemented without a structured assessment of their viability or without transparent documentation.

What used to be handled in a pragmatic and generally unstructured manner is now subject to clear regulatory requirements. The EBA guidelines on management of non-performing and forborne exposures (EBA/GL/2018/06) and MaRisk have established forbearance as an independent management tool in the credit process. The combination of a challenging market environment and growing audit pressure clearly shows that forbearance requires greater operational and strategic attention in credit institutions.

Audit reality: what are the current requirements?

Current special inspections bring to light that although many institutions have introduced initial provisions, they have not yet established consistently robust structures. Here are some typical findings:

- Lack of business model-specific requirements: the written rules and process specifications do not meet regulatory requirements.

- Unclear allocation in the loan management structure: forbearance measures are not systematically taken into account as a criterion for intensified or problem loan management.

- Lack of effectiveness monitoring: there is no adequate systematic monitoring of the effectiveness of the forbearance measures granted.

These points show that forbearance is no longer just a reporting obligation for banks, but a strategic element of credit management – with direct relevance for risk assessment, reporting and governance.

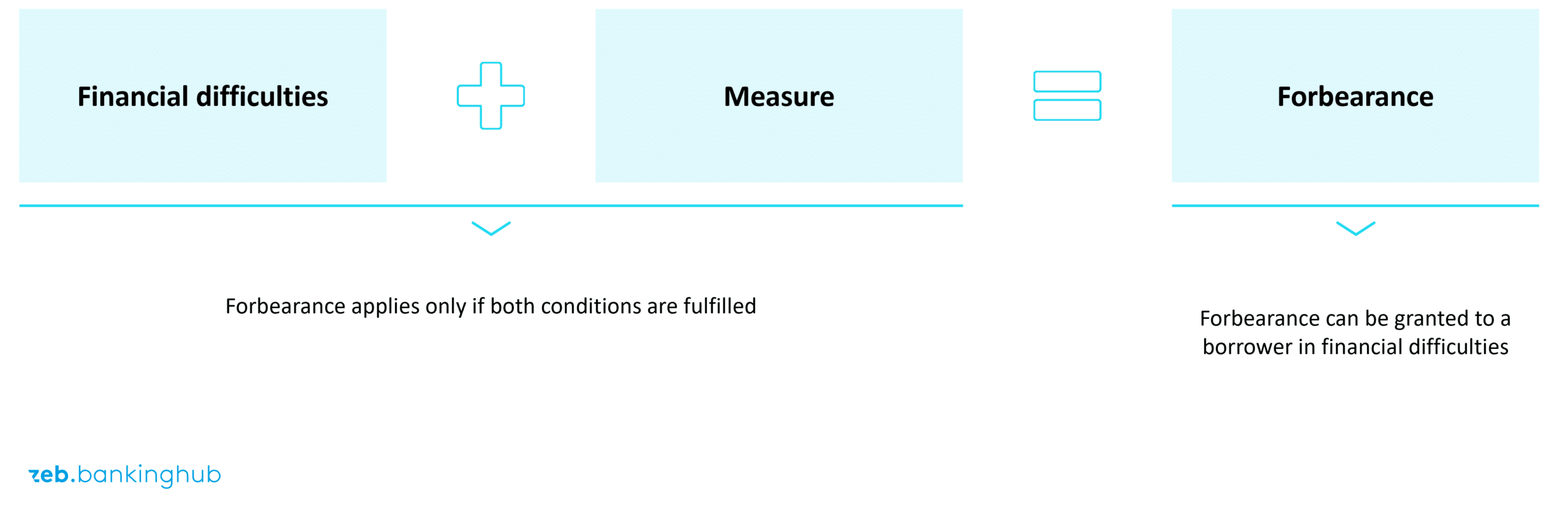

How can financial difficulties be reliably identified at an early stage?

A key starting point for every forbearance measure is the systematic identification of the borrower’s financial difficulties. If a customer is then granted a measure, the definition of forbearance applies.

In practice, there are often uncertainties when it comes to identifying financial difficulties, both in terms of the criteria to be applied and with regard to the distinction from purely cyclical, temporary burdens which can nevertheless lead to a sustained impairment of debt-servicing capacity. This is particularly evident in the lack of consistency in identifying forbearance cases when measures are granted. A consistent assessment is particularly challenging for front-office units due to the large number of individual cases to be assessed by different people.

An informed assessment requires a comprehensive analysis of the borrower’s overall situation. Not only internal factors specific to the company such as liquidity bottlenecks, declining earnings or operational difficulties should be taken into account. External influences also play a decisive role – for instance, industry-specific trends, macroeconomic developments or regulatory changes that can have a direct impact on the company’s business situation.

Two methodological approaches to recognizing financial difficulties have established themselves:

- Rule-based approach: early warning indicators or standardized criteria provide an objective assessment basis – particularly suitable for homogeneous portfolios.

- Expert-based approach: in the case of complex exposures, a qualitative assessment is required – for example on the borrower’s debt-servicing capacity, the industry situation or personal circumstances.

The decisive factor is that the assessment must be documented transparently and applied consistently.

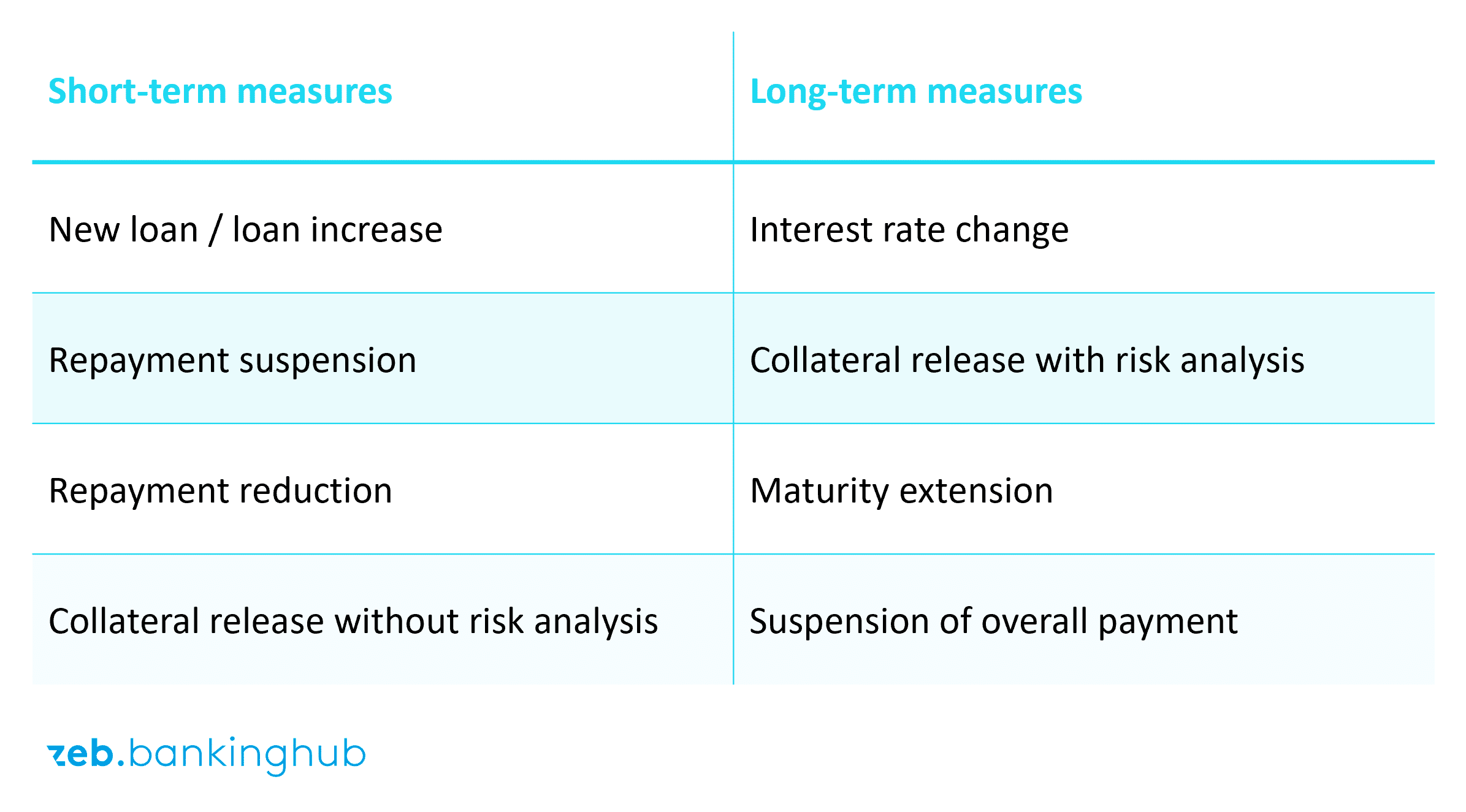

What instruments are generally available to credit institutions?

Institutions have various measures at their disposal that they can grant their customers. A fundamental distinction is made between short-term and long-term measures. Some examples of possible measures are listed in the table below.

How can their viability be reliably assessed?

When granting forbearance measures, banks need to assess whether the respective measure can be classified as viable. A measure is considered viable if it is likely to contribute to a reduction in the borrower’s risk position. This assessment is based on an informed (ex-ante) assumption about the borrower’s future solvency and business development.

Another key aspect of the viability assessment concerns so-called re-forbearance cases where an exposure that has previously been granted a forbearance measure is granted another one. Such cases are generally not considered viable, as the measure has already been applied before without having a lasting effect. However, this must be assessed on a case-by-case basis and does not constitute a general rule.

The duration of the measure also plays a role: if forbearance measures exceed a term of 12 months (project financing and commercial real estate under construction) or 24, the borrower is assigned to problem loan management regardless of the assumed viability, and the exposure is regarded as a regulatory default.

In principle, credit institutions are also free to grant forbearance measures that are not viable, especially if this has the potential to stabilize the current status of the exposure and no further deterioration in the customer’s financial situation is to be expected. The assessment of the viability of a measure has a direct impact on the loan management level and the default status of the exposure. Viable measures are generally associated with intensified loan management, while non-viable measures are handled in problem loan management. Purely identifying financial difficulties while maintaining a regular loan management level is criticized by the supervisory authority.

Effectiveness analysis: what can be derived from existing forbearance measures?

The regular effectiveness analysis required by supervisory law is a central element of an audit-proof forbearance process. The aim is to retrospectively evaluate the success of individual measures while also gaining insights that could be decisive for the future design of possible forbearance measures. The mere aggregation of quantitative KPIs does not comply with regulatory requirements. Qualitative analyses on a case-by-case basis are required.

In practice, this leads to considerable challenges:

- There is often a lack of consistent and reliable data.

- Many measures were not systematically documented in the initial phase of implementation.

- The methodological know-how for assessing forbearance effects is often insufficiently developed.

Nevertheless, such analyses are essential in order to meet regulatory requirements – and to establish forbearance as an effective management tool in the long term. For standardizable portfolios, it makes sense to develop predefined forbearance solutions where the effectiveness can be derived from their history.

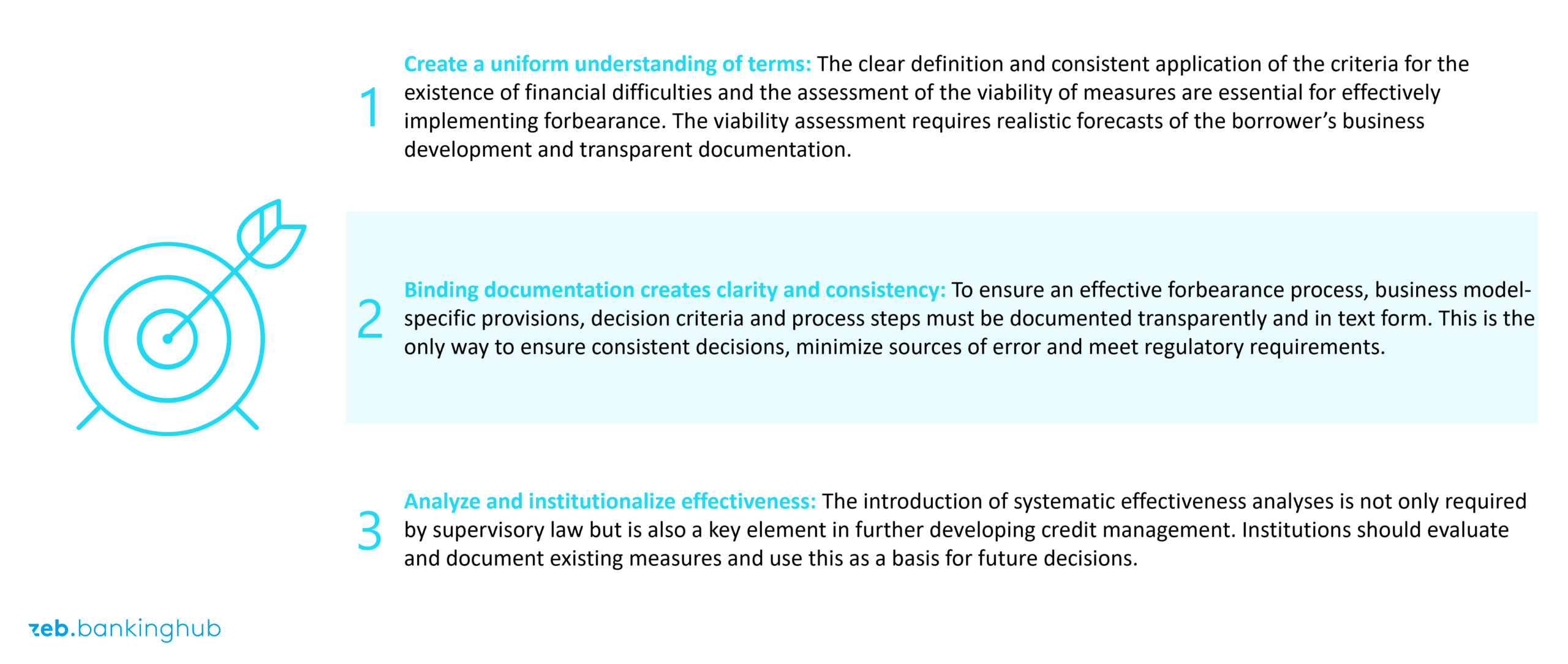

What recommendations for action can be derived for banks?

Three key areas of action for banks can be derived from current developments.

Conclusion: between regulatory obligation and strategic opportunity

Forbearance has long been more than just a regulatory measure to stabilize individual exposures. It is an integral part of a modern lending strategy, especially in volatile market phases. At the same time, the requirements regarding process quality, risk assessment and documentation are increasing.

The supervisory authority has clearly formulated its expectations, and it is now up to the credit institutions to implement them. zeb supports banks in implementing the regulatory requirements and optimizing their credit processes – with tried and tested best practices and a deep understanding of the regulatory framework. Based on these, the balancing act between regulatory compliance and sustainable customer management in lending can be achieved, even in challenging market phases.