The initiative from BCBS, however, does not only affect those banks that calculate their credit risks according to the standardised approach (so-called SA institutions), but also those that use the internal rating-based approach (so-called IRBA institutions). The reason for this is the planned introduction of a new capital floor, which is based on the revised standardised approach and represents a floor for the risk-weighted assets (RWA) of an IRBA institution. However, when making amendments to the standardised approach, the Basel Committee expressed their intention to not increase overall capital requirements. The analysis in this article shows, however, that there is major potential for increasing the capital requirements for the 50 largest banks in Europe due to the capital floor mentioned above.

The capital floor: Present and future

The floor rule currently in force was introduced as part of Basel II and represents a floor for capital requirements calculated under the internal model approaches. It is determined as a percentage of the bank’s capital requirements based on the standardised approach according to Basel I.[2] The floor has been 80% since 2009. If the institution’s capital requirements according to the IRB approach are below 80% of the capital requirements according to the standardised approach, then the corresponding difference should be treated as an additional capital requirement, and thus, must be backed with own funds. The type of own funds that are used for this purpose is not specified, so the use of Tier 2 capital is both permitted and common practice.

In future, the floor regulation will be based on the revised standardised approach and will fundamentally be changed in terms of its design and desired effect. As opposed to the current regulation, the new floor will be applied to the RWAs and not to the own funds requirements. Therefore, the IRBA and the SA calculations will have to be compared while taking into account that the floor factor and the minimum of both will have to be applied. Thus, any RWA savings achieved using internal models will be effectively limited. To apply the proposed floor rule, it is first necessary to compare the own funds requirements under IRBA and SA. BCBS proposes two options for this:[3]

- Comparison of capital ratios according to the SA and the IRBA. Here, the RWA under the standardised approach are reduced using a calibration factor (currently 80%). The lower of both ratios is applied.

- Comparison of RWAs according to the SA and the IRBA. Here, the RWA under the standardised approach are reduced using a calibration factor (currently 80%). The higher RWAs of the two approaches are used for calculating all capital ratios.

Both options have a direct effect on the Common Equity Tier 1 (CET1) ratio. Therefore, institutions will not be able to serve the additional capital requirements using solely Tier 2 capital. In order to satisfy the regulatory minimum CET1 requirements but also institution-specific target ratios, banks will have to cover capital requirements arising due to the floor using CET1 capital.

Besides the floor options named above, the specific design of the floor considering all relevant risk types is still under discussion. The BCBS did not specify the calibration level (the lower limit) and the aggregation level of the floor (applicable for option I—comparison of RWAs) in the first consultation paper. There are three options being currently discussed regarding the aggregation level:

- A floor based on total RWA

- A floor based on risk types

- A floor based on exposure classes

The major difference between the three options is the possibility to settle negative floor effects.

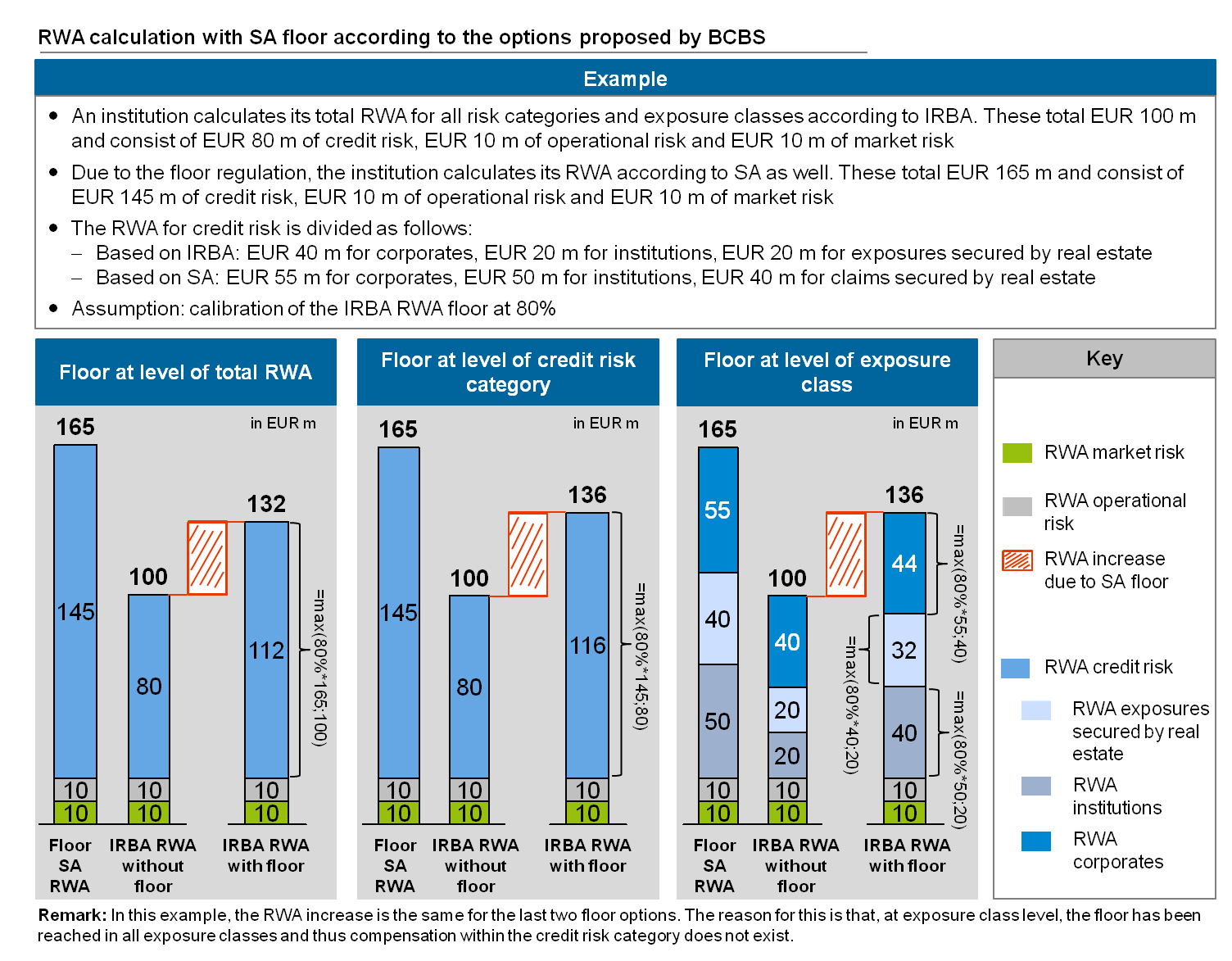

Under option 1, the total RWA under the internal approaches for credit risk, market risk and operational risk are calculated (if no internal model is accepted for a certain risk type or a certain portfolio, then the standardised approach is used) and compared to the total RWA under the standardised approaches.[4] This option allows a settlement between individual risk types. This means, for example, that if a bank uses the internal approach for its credit risk and standardised approach for the other risk types, then the additional capital requirements due to the floor rule would be lower than if the floor was only applied for the credit risk.

Under option 2, the RWAs are compared at the level of the risk types: the RWA of an exposure type according to the respective internal model is compared to the RWA according to the respective standardised approach. In this way a settlement between the individual risk types as per option 1 is not possible (however a settlement between exposure classes is still possible) and is, consequently, seen as more conservative than option 1.

Under option 3, the RWAs for each exposure class according to the internal approach are compared with the RWAs for the respective exposure class according to the standardised approach. This is the most conservative of the three options because it allows neither a settlement between risk types nor a settlement between exposure classes (as per option 2). The three options are briefly illustrated in the following example. Effects arising due to the revision of the standardised approach for market risk (Fundamental Review of the Trading Book) and operational risk are not included here.

Figure 1: Calculation of the floored RWA according to the 3 floor options

Figure 1: Calculation of the floored RWA according to the 3 floor optionsThe next section discusses how the three options for the planned floor will affect the top European banks.

Impact of the revised standardised approach for credit risk on IRBA banks in connection with the new floor

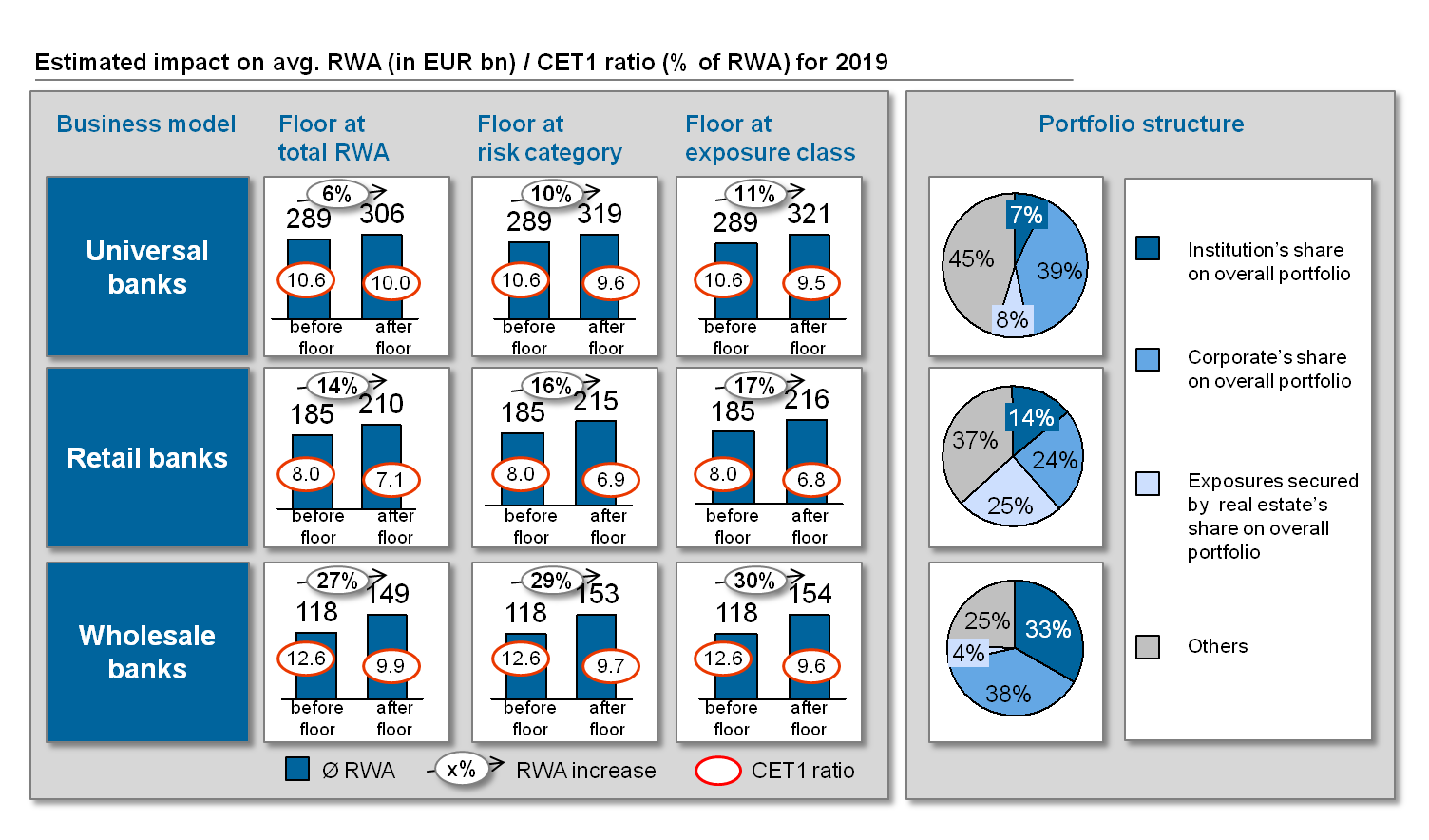

To assess the quantitative effects of the new standardised approach in connection with the new floor for IRBA banks, the 50 largest European institutions by total assets were observed. Their cumulated total assets at the end of 2014 added up to approx. two thirds of the cumulated total assets of all European banks. Further, the institutions were classified into one of three business models—either retail banks, universal banks or wholesale banks—in order to simulate the effects on various business models.

For the following analysis, the planned changes of the standardised approach were applied on the three largest exposure classes (by exposure volume) of the observed institution groups: “institutions”, “corporates” and “exposures secured by mortgages on immovable property”. In order to show the effect of the different floor options, they were simulated individually. Furthermore, option 2—comparison of IRBA RWA and SA RWA—was applied and an RWA floor calibrated at 80% of the SA RWA was assumed (as per the current floor regulation).

Data from the European Banking Study was used as a basis. The data is taken from publicly available annual and disclosure reports of the observed institutions as well as from Bloomberg’s company database and zeb’s internal Research department. The official company reports were used for deriving the portfolio structure and for determining regulatory parameters like current RWAs and capital ratios. Bloomberg’s and zeb’s databases include risk factors that are necessary for calculating RWA under the revised standardised approach.[5] The different impacts of the revised standardised approach were simulated for the three exposure classes “institutions”, “corporates” and “exposures secured by mortgages on immovable property” based on representative reference portfolios with various portfolio compositions. Thus, an average of 60% and 130% risk weights were determined under the revised standardised approach for exposure class “institutions” and “corporates”, respectively.[6]

The reference portfolios for “exposures secured by mortgages on immovable property” were built based on values (esp. loan-to-value ratios) observed in studies concerning these types of credits as well as on zeb’s own experience.[7] On this basis, we have determined an average risk weight of 45% for exposures secured by residential real estate and of 100% for exposures secured by commercial real estate according to the revised standardised approach.[8]

Results

The analysis reveals that the implications of the revised SA vary substantially depending on the bank’s business model and portfolio structure, as shown in figure 2.

Figure 2: Implications of the floor regulation by business model

Figure 2: Implications of the floor regulation by business modelThe greatest implication is observed in the wholesale banks segment. For institutions with this type of business model, the planned changes lead to an average RWA increase of between 27% and 30% and a reduction of the CET1 ratio by 2.7 to 3 percentage points depending on the floor’s aggregation level applied.

The absolute implications for retail banks seem to be lower with a CET1 ratio decrease of between 0.9 and 1.2 percentage points. Nevertheless, they are particularly badly affected due to their comparatively low CET1 ratios on average.

Universal banks are affected the least. For these institutions, an average RWA increase of between 6% and 11% and CET1 ratio decrease of between 0.6 and 1.1 percentage points are observed.

In addition, some key drivers for the RWA increase have been identified as a result of the impact analysis:

- Exposures to institutions: Especially banks having a large institutional portfolio are expected to experience a major RWA increase based on the current BCBS proposal. The reason for this is the large gap between currently applied IRBA risk weights and significantly higher IRBA risk weights for exposures to institutions resulting from the new proposed rules. The largest European banks apply an average risk weight of 17% to their exposures to institutions (universal banks 21%, retail banks 15%, and wholesale banks 17%). In contrast, the current BCBS proposal prescribes risk weights for the standardised approach between 30% and 140%, as well as 300%. This leads to a significant increase in the risk weights for IRBA institutions, even after the floor is applied. This is the main reason why we observe significant reductions in the CET1 ratios of wholesale banks having relatively large institutional portfolios. This is a key factor for the CET1 ratios reduction for retail banks as well.

- Exposures to corporates: The share of small and medium enterprises (SME) in a company portfolio has proved to be a driving factor for the RWA increase in this customer segment. The reason for this is that company turnover is planned to be one of the risk factors that determine the risk weight to be applied in this exposure class. Following, companies with smaller turnover will be assigned higher risk weights. Consequently, retail banks are particularly negatively affected due to their comparatively higher proportion of SMEs.

- Exposures secured by mortgages on immovable property: The higher the share of exposures secured by commercial real estate in a mortgage portfolio, the higher the observed RWA rise in this segment. This is attributable to the comparatively higher risk weights increase for such exposures as well as to the introduction of separate exposure class for special lending with a minimum risk weight of 120% or 150%. Even though the observed average risk weights increase is lower for exposures secured by residential real estate (from approx. 20% before floor application to approx. 36% after floor application), it could have a sensible effect depending on portfolio size as well. From the business models analyzed, retail banks have the highest share of exposures secured by real estate. Therefore, the explained effects could be clearly observed for this business model.

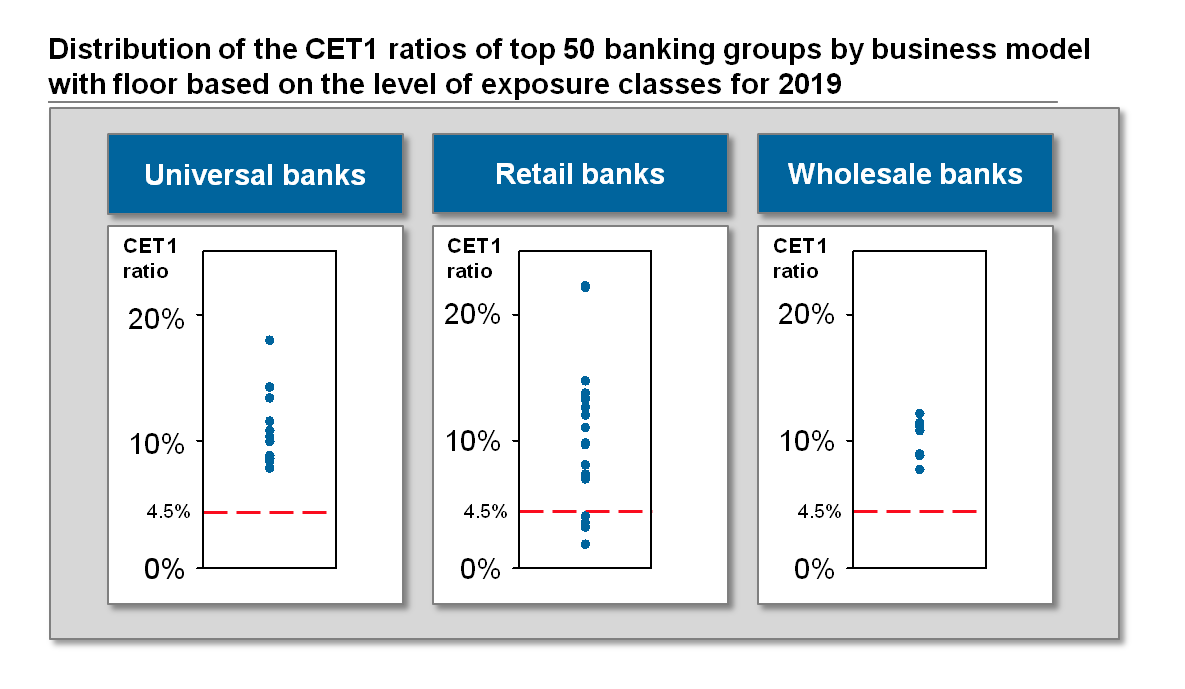

In addition to the observation of average values per business model (figure 2), figure 3 shows the distribution of CET1 ratios at institutional level (for option 3 – floor at the level of exposure class). While the average CET1 ratios for all three business models in the analysis are above the minimum level of 4.5%, the individual analysis reveals that some retail banks do not comply with this limit. This should be seen as particularly critical, especially in light of the fact that many institutions will have to fulfill higher capital requirements in future, for instance due to SREP requirements.

Figure 3: CET1 ratios of top 50 banking groups by business model for a floor based on the level of exposure classes

Figure 3: CET1 ratios of top 50 banking groups by business model for a floor based on the level of exposure classesIn addition to the results of the conducted simulation, zeb experience shows that the effects for an individual institution can be very different due to further specific provisions of the proposed revised standardised approach. For example, institutions with relatively large portfolios of exposures to corporates secured by other physical collaterals will be disproportionately negatively affected by the proposed floor regulation. The reason for this is that under the revised standardised approach, physical collaterals will no longer be eligible for corporate exposures, what will lead to a great increase in the RWA for these exposures.

Conclusion

Despite the Basel Committee’s explicitly expressed intention not to cause any increase of capital requirements with the revision to the standardised approach, in many cases IRBA institutions will be faced with significant additional capital charges. The effect will vary depending on the final design of the revised regulations.

Besides the possible capital impact that results from the introduction of a floor based on the revised standardised approach, additional negative effects are to be expected due to further ongoing European regulatory initiatives such as the “Fundamental Review of the Trading Book” or the new treatment of interest rate risks in the banking book. Furthermore, discussions about a fundamental revision of the IRBA are ongoing – “Future of the IRB Approach”. The overall effects of these initiatives vary depending on the business model and are to be analyzed and evaluated for each institution individually.