How are the boundaries of proportionality shifting in banking supervisory law?

Since its introduction, SNCI status has been regarded as a key component of the proportionality concept in European banking supervisory law. Small and non-complex institutions have been intended to benefit from simplifications, which are reflected in reduced reporting and disclosure obligations, simplified ratios and less supervisory effort overall. Specifically, institutions with SNCI status can, for example, take advantage of the proportionality relief provided by MaRisk and apply the simplified sNSFR. Many banks are making the most of these benefits and are consistently gearing their processes and resources towards a “light supervisory regime”.

In recent months, however, a remarkable trend has emerged: more and more institutions, especially those in a phase of heightened supervision, of prevention or even in an early form of recovery, are losing their SNCI status – often despite meeting the objective, quantitative criteria. What initially appeared to be a marginal phenomenon is now developing into a structural pattern in supervisory practice, resulting in increased requirements for many small institutions.

What does SNCI actually mean and why are increasingly narrow definitions taking hold?

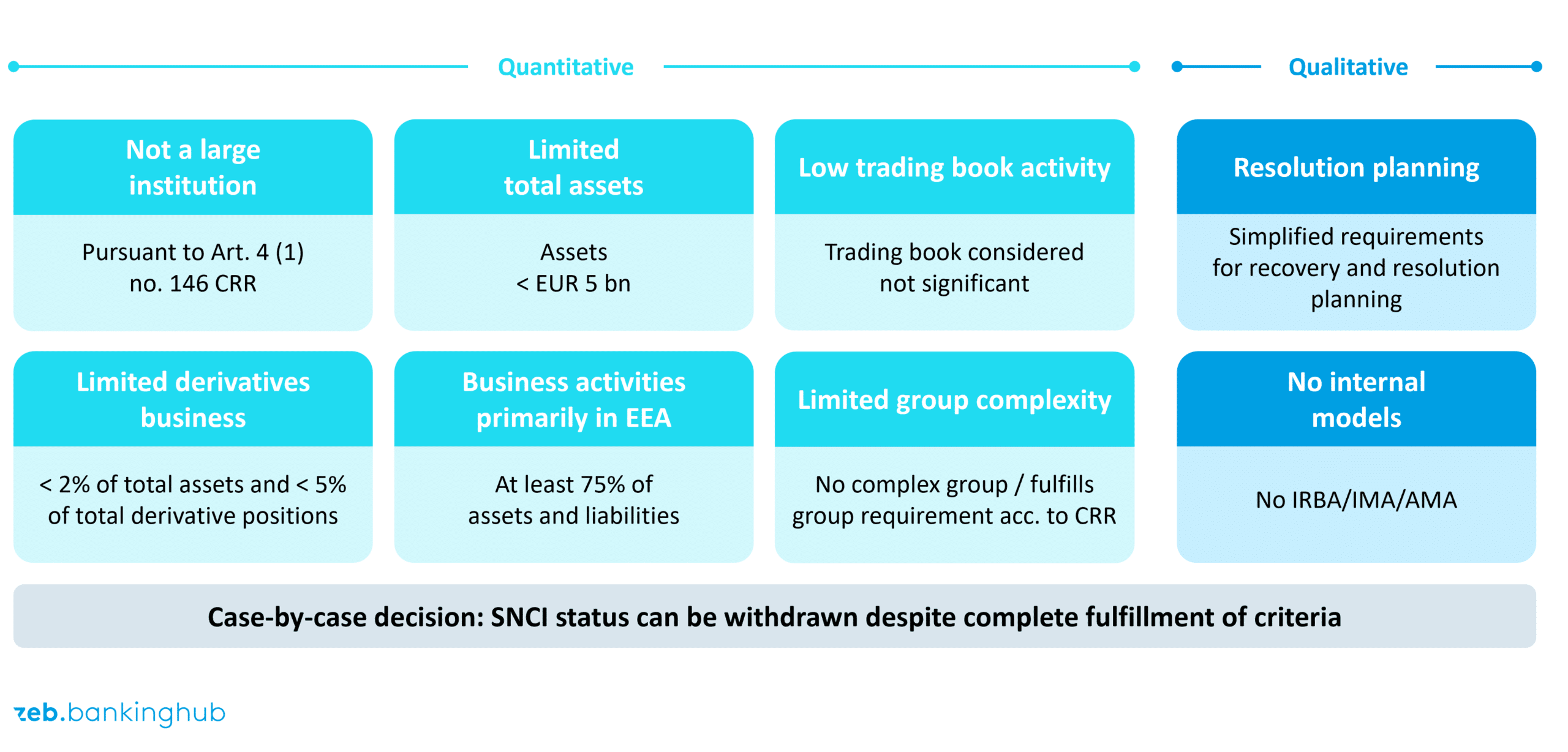

The basis for classification as an SNCI is provided by Article 4 (1) no. 145 CRR. It defines various criteria which are essentially intended to ensure that the institution represents a limited risk for the financial system because of its size, balance sheet structure, complexity and risk profile. In practice, this mainly relates to institutions with little interdependence, without an extensive trading book and without complex derivative business, as well as with relatively stable business models and clear governance structures.

These criteria, however, are only part of the truth. This is because the supervisory authority also has a significant discretionary option: according to paragraph j of the same article, it may classify an institution as a non-SNCI irrespective of the objective criteria if the risk profile makes this appear necessary. For a long time, this provision was not particularly prominent – but it is precisely here that the current trend comes in.

How is the supervisory opt-out increasingly becoming the standard rather than the exception?

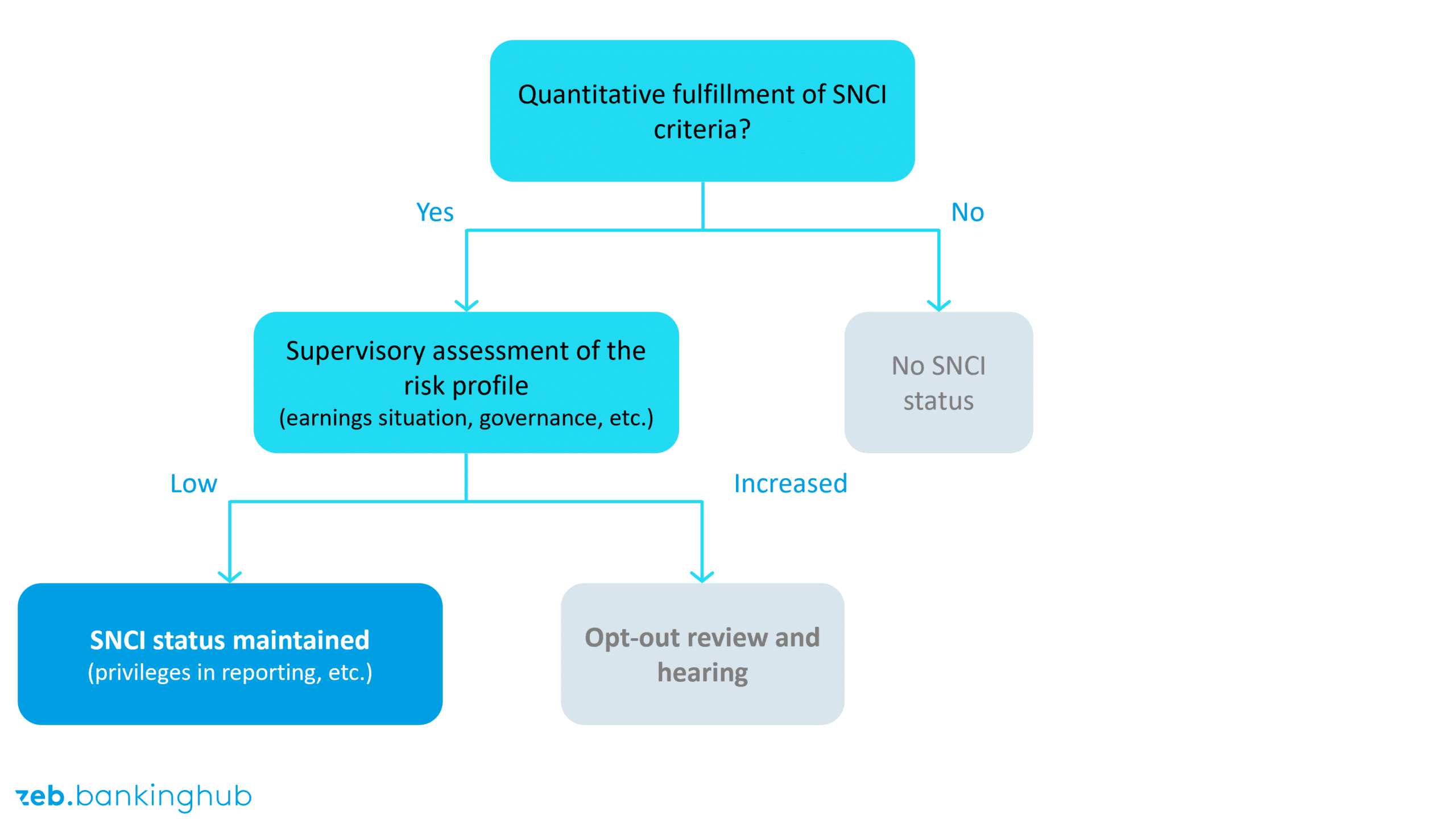

What used to be the exception is becoming increasingly common. BaFin and – in the European context – the ECB are exercising their classification powers much more actively. More and more frequently, SNCI status is being withdrawn, even though the institution formally fulfills all quantitative requirements. The supervisory authority justifies this with an “overall assessment of the risk profile”, which in certain cases is no longer compatible with that of a small and non-complex institution.

What is particularly noteworthy is way these decisions are explained. Several current supervisory letters expressly point out that a deterioration in earnings, structural weaknesses in the business model or a tense risk situation are already sufficient to no longer justify SNCI status from a supervisory perspective. The fact that the objective criteria are still fulfilled is openly acknowledged – but considered to be of secondary importance.

Why do supervisory authorities withdraw SNCI status from institutions that are undergoing restructuring or under increased observation?

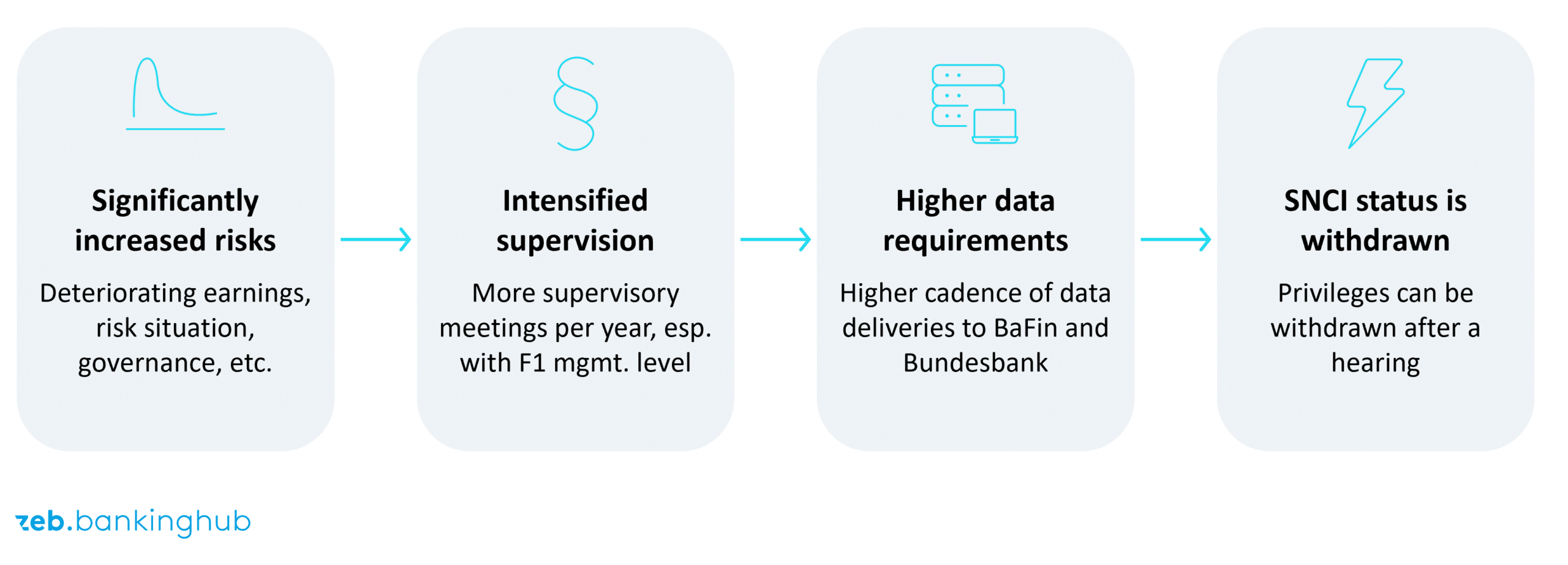

It is noticeable that this practice primarily affects institutions that are already subject to intensified supervision. Withdrawing their SNCI status is often the first step, especially in the context of prevention measures, early intervention or possible recovery.

From a supervisory perspective, the reason for this is understandable. For supervisory authorities, an institution that bears increased risks – whether due to a strained earnings situation, a deterioration in the capital or liquidity situation or structural challenges in the business model – no longer fulfills the core principle of the SNCI definition: low complexity and a manageable risk profile. Moreover, they argue that simplifications for such institutions contradict the goal of stabilization. Closer supervision, more frequent data deliveries and more in-depth analyses are required for institutions undergoing prevention or recovery measures. The SNCI regime, which is designed for reduced data requirements, is no longer appropriate.

As a result, we can see a clear pattern: for institutions in intensive supervision, losing their SNCI status is de facto a foregone conclusion.

What impact does the loss of SNCI privileges have on banking operations?

Losing SNCI status has far-reaching consequences that are often underestimated in practice. The end of those privileges not only leads to additional obligations, but also to short-term pressure on staff, IT and the data warehouse.

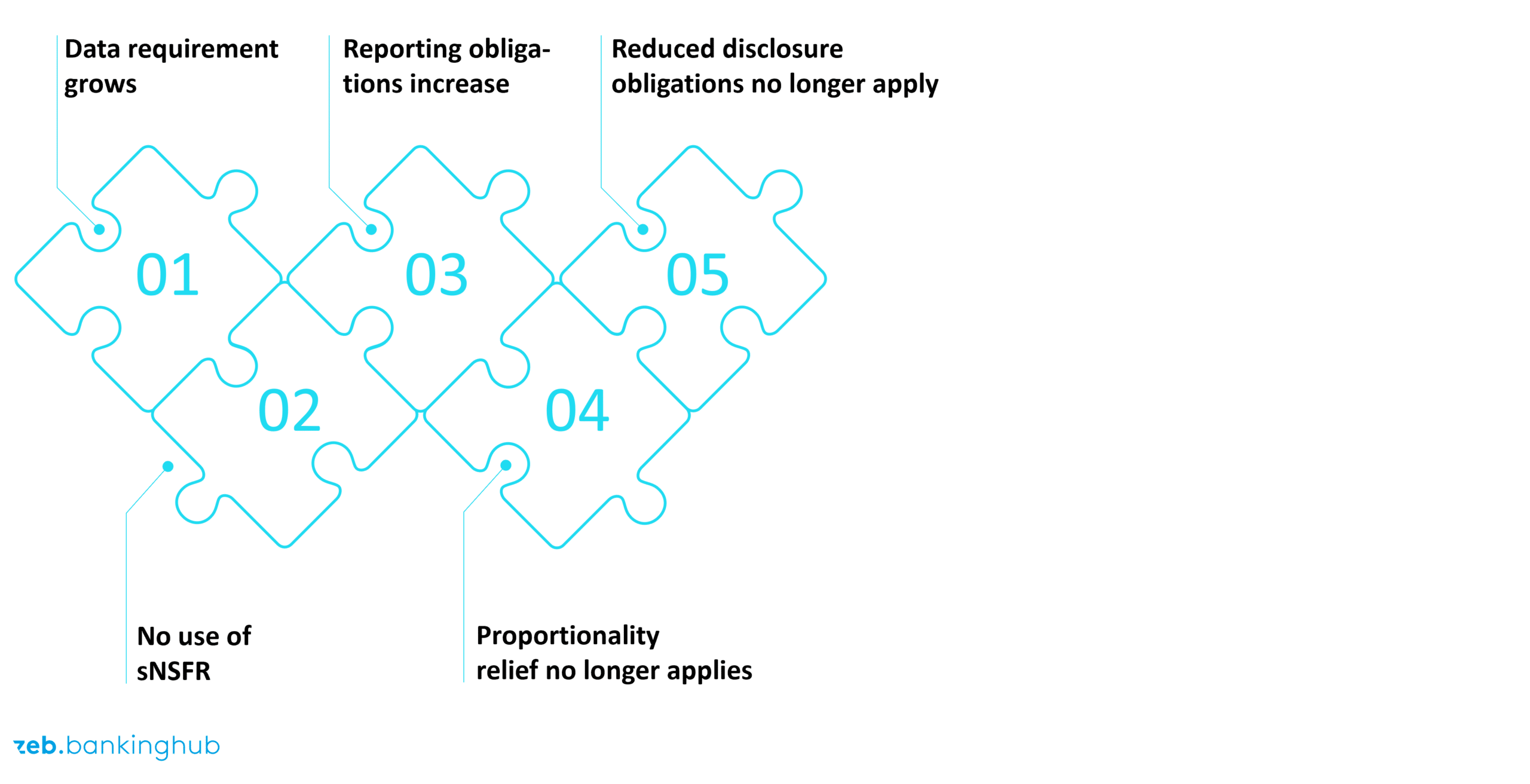

Within a short period of time, institutions have to go back to preparing full reports, calculate additional ratios and, in some cases, implement completely new processes. The simplified sNSFR no longer applies, more extensive reporting forms must be used for IRRBB reporting, disclosure obligations as well as the frequency of data collection and reporting (e.g. AMM reporting) increase. Especially for smaller banks, which have deliberately geared a “lean” operating model to the SNCI regime, this results in significant additional burdens and often considerable coordination effort.

At the same time, direct supervision is intensifying. Discussions are becoming more frequent, inspections more detailed and the requirements for governance and risk management are increasing noticeably. In a situation in which an institution is already facing structural or financial challenges, this additional burden often has a compounding effect and can further exacerbate operational bottlenecks.

Attention should also be paid to the fact that the simplifications published by the German supervisory authority in 2024 (see BankingHub (2024): MaRisk – Regulierung für kleine Finanzinstitute: BaFin schafft Luft zum Atmen (only available in German) are also no longer (fully) applicable. However, this requires a case-by-case assessment.

How can bank management teams respond proactively to the risk of losing SNCI status?

Current developments show that SNCI status is not permanently guaranteed and can only be actively “controlled” to a limited extent. Although institutions can consciously comply with the formal criteria of the CRR, the qualitative case-by-case assessment by the supervisory authority is largely beyond operational control.

The actual management task is therefore not to actively control SNCI status, but to anticipate SNCI risk at an early stage and to build up organizational resilience in case of status withdrawal. A key element is consistent compliance with and ongoing monitoring of the formal SNCI criteria (total assets, volume of derivatives, trading book activities, use of internal models, etc.). These represent the basic prerequisite for being able to defend the status at all.

At the same time, institutions should systematically monitor their qualitative risk signals – especially earnings situation, equity development, cost of risk, governance stability and business model viability. Business model analysis is a suitable starting point for this forward-looking approach. It provides a structured framework to make qualitative developments visible at an early stage and allows an integrated assessment of the business model’s long-term viability (see BankingHub (2025): Geschäftsmodell Regionalbank – von Hoch zu Hoch oder zurück zu längst vergessenen Herausforderungen?!) (ony available in German). The supervisory case-by-case decision on the SNCI status is largely based on an overall assessment of the factors mentioned, so that the business model analysis can be used as an integral part of an SNCI self-assessment.

Since a withdrawal of SNCI status can occur at short notice and have immediate operational consequences, precautionary planning of additional efforts is becoming increasingly important. These include:

- early identification of additional reporting and disclosure obligations,

- assessment of IT and data warehouse capabilities for extended COREP/IRRBB and liquidity reports,

- estimating staff and resource requirements in the event of being downgraded,

- integration of possible additional efforts into multi-year and capital planning.

Dealing with SNCI status thus becomes a matter of organizational robustness: institutions that secure formal criteria at an early stage and realistically price in the additional operational efforts can significantly cushion the impact of a status withdrawal – even if the supervisory decision itself cannot be controlled.

If the status is actually withdrawn, the previously identified operational measures must be implemented swiftly and integrated into the bank’s standard processes. At the same time, it is important to analyze the reasons for the withdrawal and work towards regaining the status in close dialog with the supervisory authority.

Outlook: Under what conditions does the principle of proportionality continue to apply to small institutions?

The regulatory framework for SNCIs will remain in place in the future. At the same time, recent practice clearly shows that supervisory authorities are increasingly focusing on qualitative criteria and the institution as a whole. Therefore, the real message is this: proportionality ends where risks become visible.

For institutions aiming to secure their privileges in the long term, this means a change in culture. Complying with threshold values is no longer enough. What is needed is robust, well-documented risk management and active communication with the supervisory authority.

Conclusion: SNCI is not a status written in stone, but a promise – and a risk

SNCI status is valuable – but it cannot be taken for granted. Recent supervisory practice has shown that qualitative assessments of the risk profile are increasingly becoming decisive. Especially institutions undergoing prevention or recovery measures must expect to lose their privileges at short notice.

For banks this means that SNCI status is not a label but a management issue. Those who analyze at an early stage, manage in a quality-oriented manner and communicate transparently can secure their privileges in the long term. However, those who find themselves in a phase of increased risk must take into account that SNCI status is one of the first supervisory privileges to be withdrawn.