The CBDC system will be an environment parallel to the one based on fiat currency. Unlike traditional fiat currency systems, the CBDC system will be based on an asset class held outside of the traditional banking system. Thus, any conversion of existing non-cash assets into the Central Bank digital currency will cause outflow of financial assets from existing banking system.

Another distinctive feature of this system will be to conduct payments directly between participants, without engagement of third parties (such as clearing houses, settlement institutions, payment systems operators, etc.). This would lead to the elimination of all intermediaries that are currently present in traditional payment systems and revenues generated from them, also by banks.

Currently, several central banks are considering issuance of CBDC and they are working on the general design of such a system.

There are various CBDC setups considered. Depending on the setup that is finally applied, there is a different impact on banks. The strength of this impact will be determined by several features of this newly designed system.

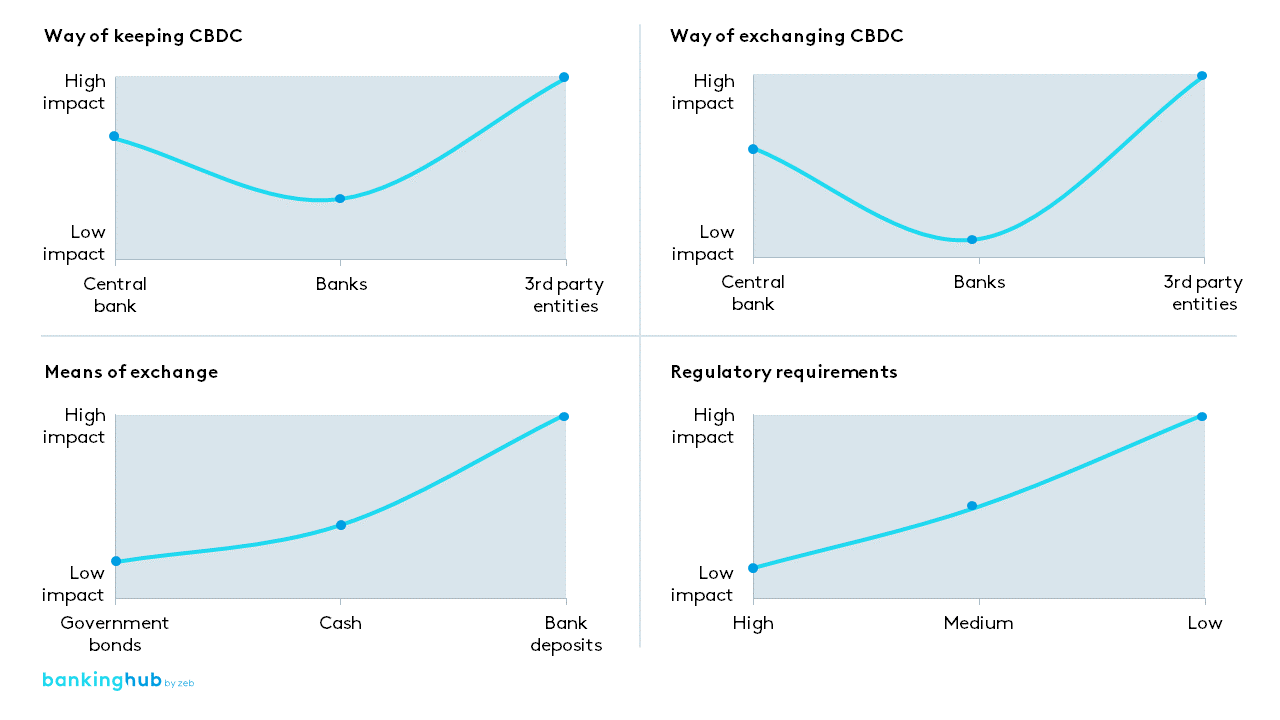

- Way of keeping CBDC

One of the most important questions is how CBDC will be stored. It is assumed that there are three major options for this matter. It could be stored directly in accounts held at the Central Bank (where all retail clients have opened their personal accounts), in banks (it would work similarly as distribution of cash by banks, only the form of asset would be different) or at various third party providers (e.g. FinTechs, GAFA (Google, Amazon, Facebook, Apple)) as tokens in electronic wallets or combinations of the above options. From a bank’s perspective of course the least impactful solution would be a setup with CBDC assets stored only at banks. The most impactful one for banks would be a setup where various providers are entitled to keep CBDC and can offer additional payment services also related to fiat currency. Clients will be enabled to keep this currency (CBDC) on wallets provided by these third parties. - Way of exchanging CBDC

Same as for the aforementioned, it will be crucial from a bank’s perspective which entity will have an entitlement to exchange CBDC against fiat currency. Opening this service to various providers would have the most serious impact on banks, however restricting it to the Central Bank only, will also deprive banks of profits from transaction processing due to outflow of deposits in fiat currency to CBDC. - Means of exchange

Decision on how CBDC could be obtained will be another factor impacting the whole financial system and banks. There are different considerations which setup should be applied. The least impactful approach would be when only government bonds are directly exchangeable for CBDC. A more liberal approach would enable purchasing CBDC by cash. The most impactful approach would allow direct exchange of banking deposits in fiat currencies into CBDC. - Regulatory requirements

Minimum requirements defined by local regulatory bodies in order to offer services related to CBDC (e.g. a wallet for CBDC storage, payments and exchange) will determine the entry barriers and thus the competition in the CBDC system.