Trends with impact on payment systems

The first trend of them is the “Internet of Things” – “network of physical devices, vehicles, home appliances, and other items embedded with electronics, software, sensors, actuators, and connectivity which enables these things to connect and exchange data”[2] and related machine-to-machine (M2M) payments where networked devices automatically perform payments without the manual assistance of humans. Other trends are: “Virtual Economy” – commercial usage and trade of digital data and content; new purchase patterns where clients expect convenient micro payments and their instant processing and last but not least, increasing demand for data privacy. All these trends combined, accompanied by a massive switch to digital payments, will push the introduction of a completely new payment system on a peer-to-peer basis, constantly available 24/7, instant and incurring only low costs.

The most prominent idea of creating such a system was building it on blockchain technology, which enables the direct transfer of assets between participants without the presence of a third party. This feature seemed like a perfect fit taking into consideration new customers’ needs. Based on this approach, completely new payment systems were created, centered on various cryptocurrencies (e.g. Bitcoin, Ether, Dash). While this solution seemed very interesting and revolutionary at the beginning, many obstacles emerged and as for now, wide adoption of these means of payments seems impossible. First of all, the most significant hindrance is high volatility of cryptocurrencies. As the latest example shows, Bitcoin faces very serious value swings (e.g. at the beginning of December 2017 Bitcoin’s value was almost 20k USD which decreased to below 11k USD only within one month). Due to the inelasticity of Bitcoin supply (the maximum number of Bitcoins is locked), it will be more volatile than silver or gold, where the supply might be steered by mines opening and closing.[3]

In order to remedy this issue, ideas of issuing private “stable coins” or cryptocurrencies pegged by the Central Bank, where the exchange rate against the fiat currency is guaranteed, were analyzed. While the concept of coins pegged by the Central Bank turns out not be viable from a monetary perspective, so far privately issued “stable coins” either failed or their volume was insignificant.[4] Therefore, private stable coins could become part of a widely accepted payment system only in case of joint cooperation of major commercial banks on respective markets. Currently such concepts are being developed, either only for wholesale settlements between banks (e.g. Utility Settlement Coin jointly issued by Credit Suisse, Barclays, HSBC, Deutsche Bank and UBS) or individually for retail payments by Japanese banks – parallel initiatives of MUFG coin (Bank of Tokyo-Mitsubishi UFJ) and J-Coin (Mizuho Financial Group and Japan Post Bank).

An increasing regulatory backlash against cryptocurrencies, due to illicit activities connected to them and insufficient customer protection as well as a still relatively low acceptance rate constitute additional obstacles. Consequently, in the majority of cases privately issued cryptocurrencies are used only as speculation assets instead of typical means of payments.

Central Bank Digital Currency (CDBC) concept

One way to mitigate the aforementioned problems could be to create a completely new payment system of a Central Bank digital currency, based on the same logic as existing cryptocurrencies. However, in this case not a group of private entities, but the Central Bank would be fully in charge of the new decentralized payment system. The Central Bank would control the issue of cryptocurrency and guarantee a fixed exchange rate between digital currencies and fiat currencies. In such a setup, it will be possible to eliminate problems that hinder wide adoption of cryptocurrencies. Potentially, all central banks should be strongly motivated to implement such a system, because of their statutory duties. First of all, they are responsible for the development and introduction of a safe and efficient payment system, which contributes to the overall benefit of the society. Moreover, it will enable the creation of a new instrument which could replace cash in physical form, while still keeping its distinctive features (such as holder’s direct claim on Central Bank, guarantying its safety).

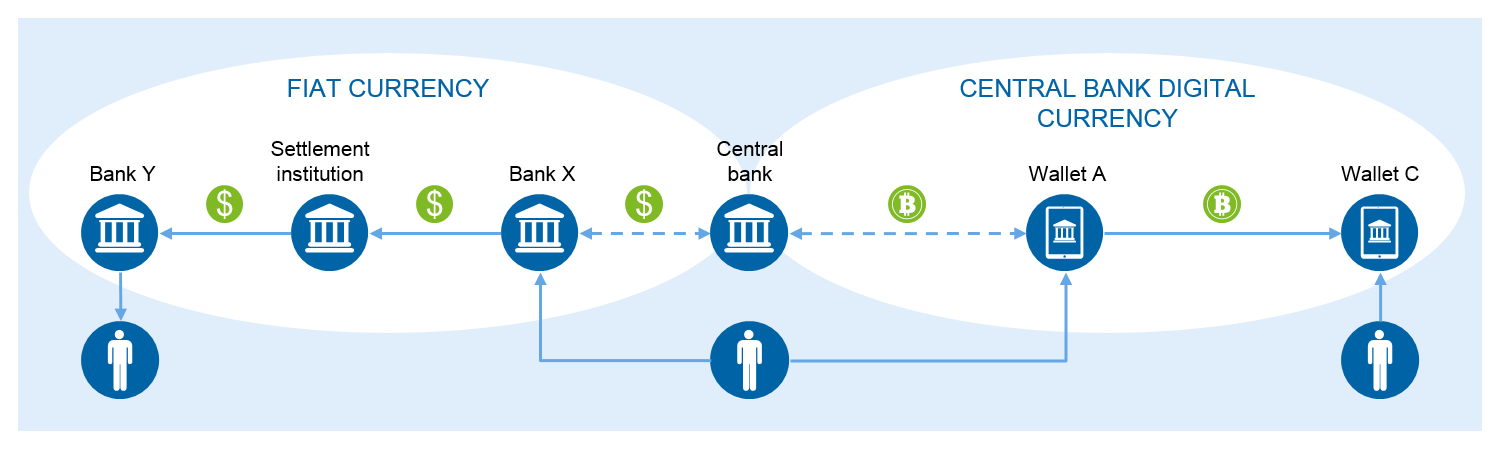

Figure 1: Dual Currency System - overview

Figure 1: Dual Currency System - overviewThe CBDC system will be an environment parallel to the one based on fiat currency. Unlike traditional fiat currency systems, the CBDC system will be based on an asset class held outside of the traditional banking system. Thus, any conversion of existing non-cash assets into the Central Bank digital currency will cause outflow of financial assets from existing banking system. Another distinctive feature of this system will be to conduct payments directly between participants, without engagement of third parties (such as clearing houses, settlement institutions, payment systems operators, etc.). This would lead to the elimination of all intermediaries that are currently present in traditional payment systems and revenues generated from them, also by banks.

Currently, several central banks are considering issuance of CBDC and they are working on the general design of such a system. There are various CBDC setups considered. Depending on the setup that is finally applied, there is a different impact on banks. The strength of this impact will be determined by several features of this newly designed system.

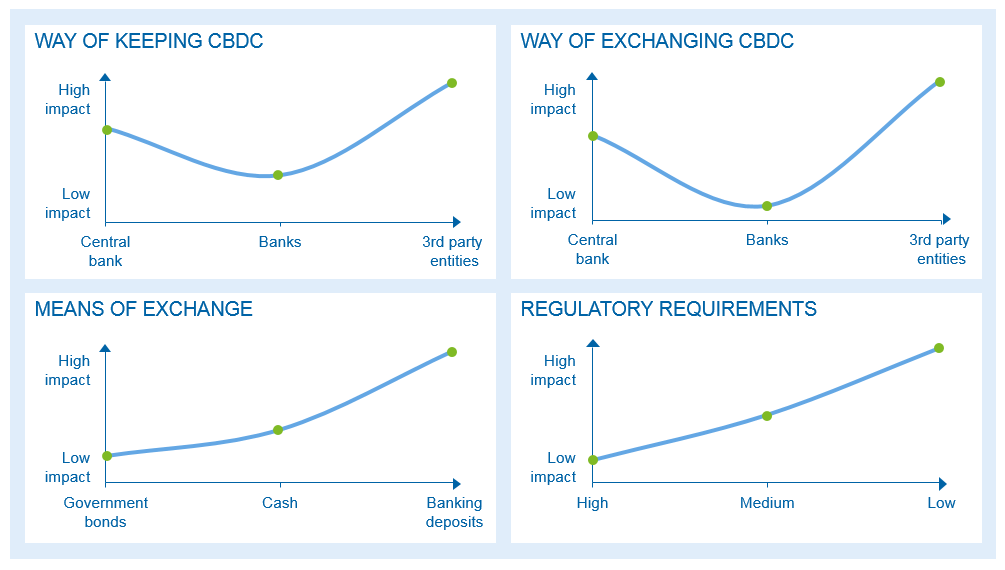

Figure 2: Factors determining CBDC system impact on banks

Figure 2: Factors determining CBDC system impact on banks- Way of keeping CBDC

One of the most important questions is how CBDC will be stored. It is assumed that there are three major options for this matter. It could be stored directly in accounts held at the Central Bank (where all retail clients have opened their personal accounts), in banks (it would work similarly as distribution of cash by banks, only the form of asset would be different) or at various third party providers (e.g. FinTechs, GAFA (Google, Amazon, Facebook, Apple)) as tokens in electronic wallets or combinations of the above options. From a bank’s perspective of course the least impactful solution would be a setup with CBDC assets stored only at banks. The most impactful one for banks would be a setup where various providers are entitled to keep CBDC and can offer additional payment services also related to fiat currency. Clients will be enabled to keep this currency (CBDC) on wallets provided by these third parties. - Way of exchanging CBDC

Same as for the aforementioned, it will be crucial from a bank’s perspective which entity will have an entitlement to exchange CBDC against fiat currency. Opening this service to various providers would have the most serious impact on banks, however restricting it to the Central Bank only, will also deprive banks of profits from transaction processing due to outflow of deposits in fiat currency to CBDC. - Means of exchange

Decision on how CBDC could be obtained will be another factor impacting the whole financial system and banks. There are different considerations which setup should be applied. The least impactful approach would be when only government bonds are directly exchangeable for CBDC. A more liberal approach would enable purchasing CBDC by cash. The most impactful approach would allow direct exchange of banking deposits in fiat currencies into CBDC. - Regulatory requirements

Minimum requirements defined by local regulatory bodies in order to offer services related to CBDC (e.g. a wallet for CBDC storage, payments and exchange) will determine the entry barriers and thus the competition in the CBDC system.

While these four features are the most important when analyzing the potential impact of the CBDC system on banks, there are also other considerations that should be mentioned. They include the approach to the CBDC implementation itself – whether it will be done gradually or issued as a one batch (“big-bang”). Moreover, there is the question whether CBDC will bear interest rates and if yes, how they are different compared to fiat currency interest rates. Also the level of existing interest rates and the economic situation in general will have considerable importance, because they will trigger general demand for CBDC (considered as a safe form of holding assets) and consequently the total value of assets converted into CBDC.

A model assessing the impact of CBDC introduction on banks’ revenues

As CBDC will have adverse effects on different participants of current payment systems (banks, settlement institutions, clearing houses, ATM operators, payment cards systems), we created a model to estimate the potential impact of CBDC issuance on bank’s revenues. In order to assess that, we simulated the impact on a selected bank in a given country, taking into account the characteristics of the particular market and institution.

The key assumption of our model is that CBDC will be merely an alternative payment system and that it will therefore negatively impact the banks’ profitability for two reasons :

- CBDC issuance will cause deposits churn, as funds held in banks will be converted into CBDC. In order to sustain the current level of lending business, deposits, which are the cheapest source of financing, outflow, they will have to be substituted by wholesale financing and/or debt issuance, which is significantly more expensive.

- CBDC issuance will cause more transactions moving to that system. This will translate into a lower number of card transactions and consequently lower revenue from interchange fees.

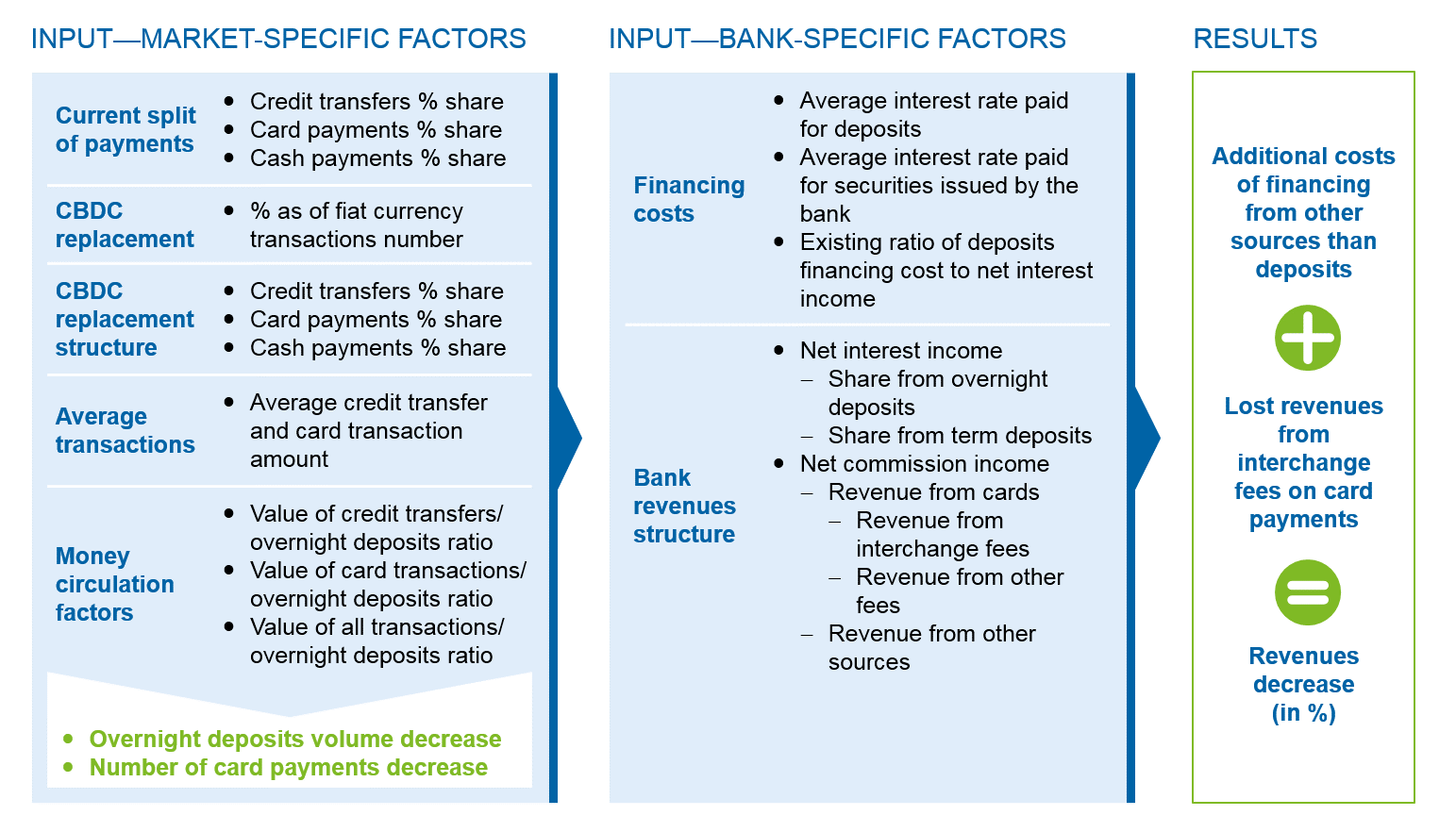

In order to estimate the impact on a bank’s revenues, the model is structured in two major parts. Firstly, it concerns all market-specific factors for a selected country. Here, inputs are: structure of current split of payments, CBDC replacement rate and its structure (i.e. what percentage of all transactions combined will be conducted in CBDC and which types of payments transactions (cash, card payments, credit transfers) would be replaced by it), value of average payments transactions in selected country and money circulation factors (i.e. ratios between volumes of different transactions types to overnight deposits volumes). Based on these values, we retrieve a volume decrease of overall overnight deposits and a total decrease of the number of card transactions (as other types of payment transactions typically do not generate direct transactional revenues). In the second part, we consider bank-specific factors, i.e. its financing costs in a given market and revenue structure. These two blocs combined enable the calculation of overall magnitude of two factors impacting a bank’s profitability.

Figure 3: CBDC impact assessment model

Figure 3: CBDC impact assessment modelWhile the model can be used for any type of bank in any country, we decided to run our analysis on a major Swedish bank. We selected this country because here adoption of digital payments is one of the highest in the world, the Central Bank Riksbank is well advanced in considerations of CBDC introduction and will very likely be the first country to implement it.

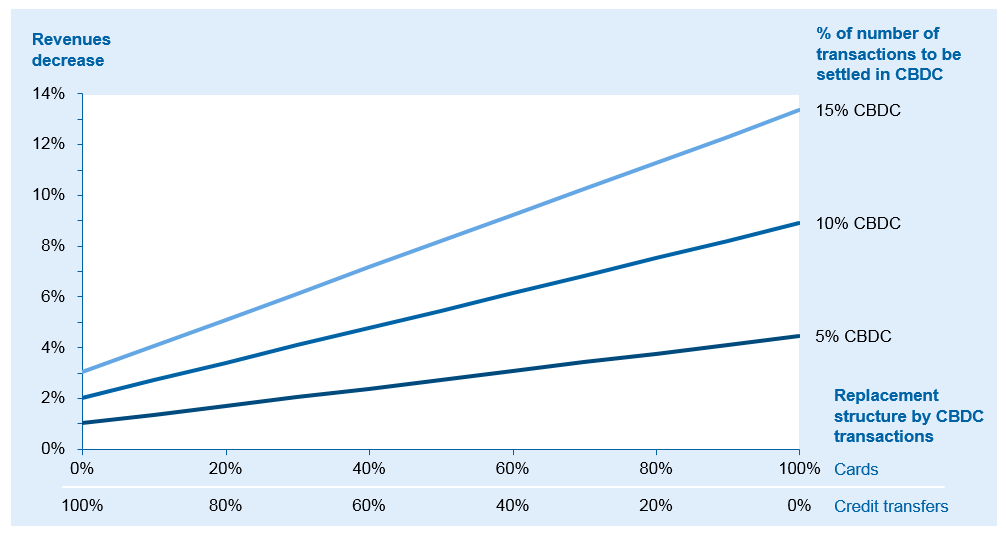

We ran three scenarios for various CBDC replacement rates (respectively 5%, 10% and 15%). All market specific factors were taken as for Sweden (e.g. structure of payments, average value of transactions… in this simulation are the same as in Sweden) and bank-specific factors as for a selected major Swedish bank.

Figure 4: Assessment model results

Figure 4: Assessment model resultsAs we can see in the above chart, in specific circumstances, in countries where cashless transactions are more prevalent, and a given bank is more reliant on card transactions and financing from retail deposits, potential issuance of CBDC may have significant negative impacts on its revenues, assuming a do-nothing scenario, especially if transactions in a new system will be replacing mostly card transactions.

Conclusions

Given current trends in social development, the introduction of CBDC does currently not seem imminent. In the next years however, it is highly likely, especially in countries where cash is being quickly displaced by digital means of payments. Since it would pose a serious threat for the banks’ profitability in the long run, the following set of options should be considered by banks as actions that would at least allow to mitigate adverse CBDC consequences – but could also enable leveraging on a new payment system:

- Prepare for participation in CBDC system – design various services that could be offered within the CBDC system (e.g. for consumers: consolidation of classic account and means of payments and wallet; for payment recipients (retailers, etc.): cryptocurrency collection/exchange/management services)

- Evolve payment cards offer – focus on features that will not be affected by CDBC (credit cards, multicurrency cards to be used abroad etc.)

- Create an attractive offer and solutions for international payments that will allow to offset shrinking revenues from domestic payments

- Invest in domestic instant payments/RTGS systems that will allow to offer payment solutions able to compete with CBDC payment scheme

- Expand corporate banking services – in order to fill the revenues gap that will arise in retail banking

- Consider building a payment system based on a stable coin as a joint initiative of banks in a given market – thus creating an effective system that could significantly reduce needs for CBDC introduction, still ensuring a source of revenues from payments