Reviews of the operating model are quite rare despite the urgent need

It is self-evident that elaborating a strategy is not the end of the story but rather the beginning, as the changes to the business models have to be implemented. Here, answers to an equally comprehensive set of questions need to be found, such as: How do I have to organize myself in order to support the future business model? Which of my processes will shape the customers’ experience in future? How can I ensure the utilization of scale effects without compromising customer proximity? Will differences in banking regulations allow for a globally harmonized process model? Can my IT architecture support my ambitions in digitization and cost cutting?

Clearly, these are questions that banking executives have been asking themselves for decades. Yet, since industry attractiveness for financial institutions will be challenged for a certain time, finding effective and practicable ways to redesign or even reinvent a bank’s value chain becomes ever more important in order to maintain a strong market position or to remain in the market. It is obvious that against the backdrop of current mega-trends in banking such as digitization, regulation, consolidation and their impact on business models of banks, operating models are to be considered and rigorously challenged.

Given that these mega-trends have already been prevalent for some time, one would expect that revisions of operating models have taken top priority for most financial institutions today. However, if you take a closer look at the project portfolios of most banks, projects related to implementing new regulations (MIFID II, FATCA or the like) and quick-wins on cost-cutting (which often compromise a coherent operating model) are currently being carried out. A comprehensive and systematic review of the operating model (i.e. on who is performing which function, where and how with what IT against recent or current business model alterations) is quite rare despite the urgent need induced by increasingly adverse market conditions.

Moreover, current project experience suggests that adaptions in the operating model, if any, are often very limited in scope (e.g. focus on organization but not on IT, sole view on Back-Office without looking at Mid-/Front-Office). This is mostly for the argument of keeping project complexity on a low level e.g. by segregating organizational from IT initiatives or by just having one business line in scope. That approach might reduce risks of failure of a single project to some extent. However, it comes at the price that this approach falls way short of aligning the business model with the operating model as it neglects the interdependencies and interconnectedness of the relevant dimensions of a TOM.

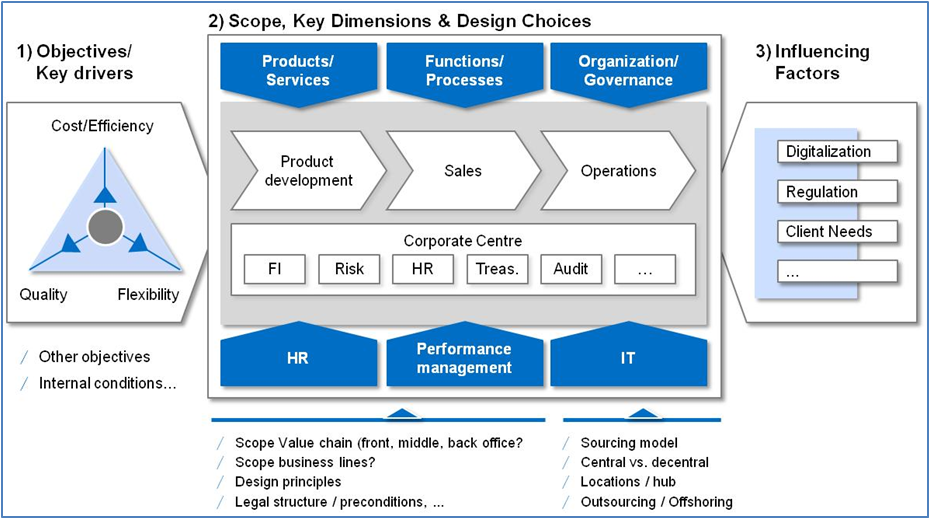

Dimensions of TOM projects

zeb project experience suggests that successful TOM projects in general address six dimensions (see Figure 1):

(Internal) products and services

Products and Services that are provided by a bank to its customers but also within a bank (e.g. from back-office to front-office). Typical questions include: Are there services /products that could be canceled or reduced, as they present little or no value to the customer? Which service shapes the customers’ experience?

Functions and processes

Functions and processes define how a bank’s value chain is organized. Typical questions include: How can processes be harmonized /streamlined across locations and/or business units? How can process complexities or excessive controls be reduced? How can idle time be minimized and the use of resources be optimized? How can customer value be increased?

Organization / governance

Organization and governance comprise the legal structure, a company’s superstructure (primary business units and P&L responsibilities), the decision-making structure and reporting lines as well as the organizational setup and collaboration rules across business units and locations. Typical questions include: What decisions are to be taken locally, i.e. close to the customer, which ones are to be taken centrally? How can economies of scale and scope be achieved without losing the customer and organizational flexibility out of sight?

HR

Talent requirements to make the Target Operating Model a success. Typical questions include: What skills are required to achieve strategic targets? How can we attract the necessary talents? How can labor cost be minimized without compromising service quality?

Performance management

Metrics and indicators that measure the effectiveness of the operating model. Typical questions include: What are the most relevant metrics for measuring the effectiveness of my operating model? How can they be measured? Which tools are to be used? How are reporting processes designed?

IT

Technology in use in order to achieve a high degree of automation, robust processes and the fulfillment of client expectations towards obtaining information and executing transactions online. Typical questions include: How can the STP rate be maximized? How can IT complexity be reduced? How can IT costs be cut without compromising quality and reliability?

Figure 1: Objects, key dimensions and influencing factors of a TOM

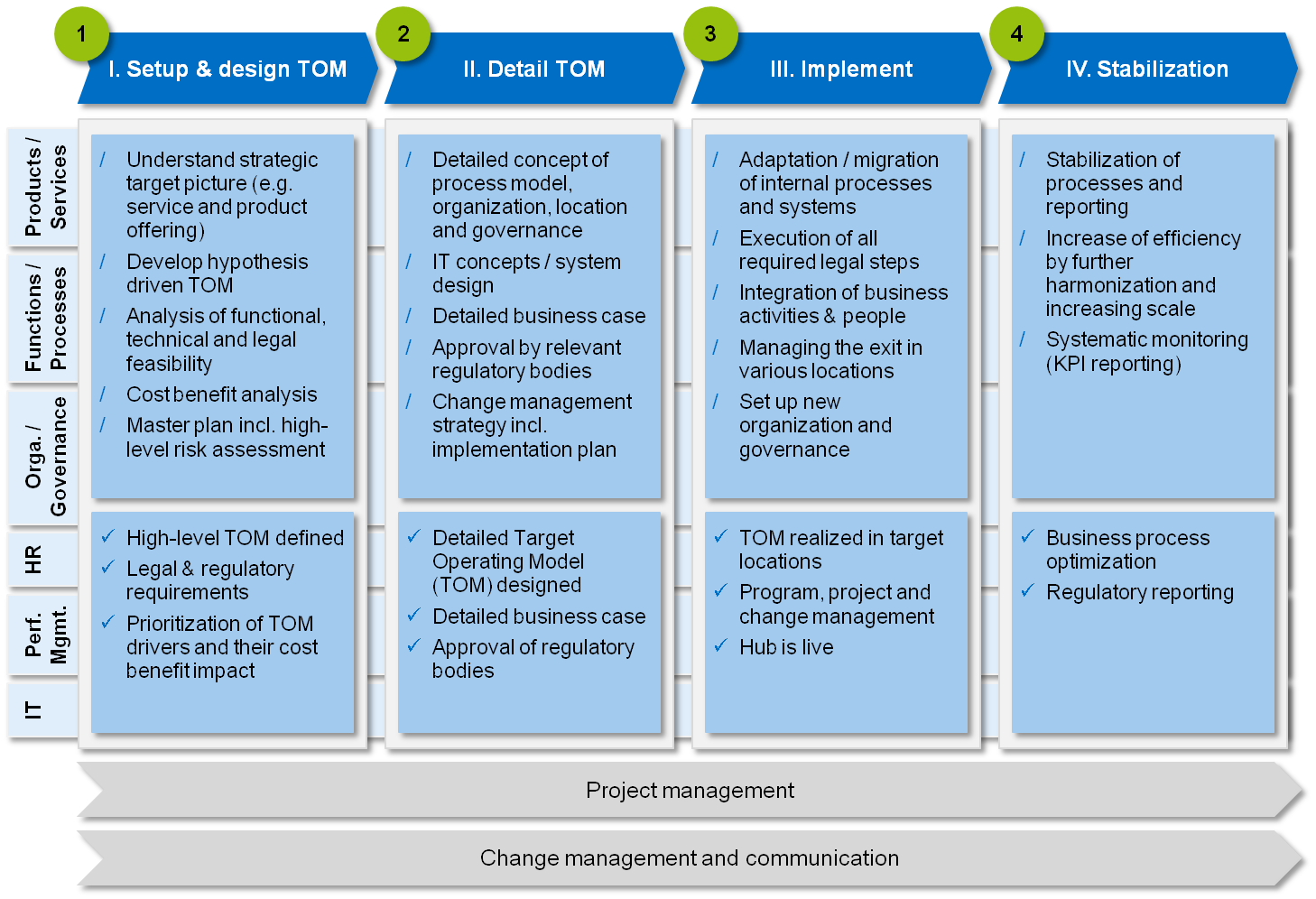

Figure 1: Objects, key dimensions and influencing factors of a TOMTOM projects are highly complex and thus require vast resources due to their broad scope and their impact on the entire organization and usually last several years from initialization to stabilization. In order to maintain the risk of failure of such a comprehensive assignment at a manageable level, a robust project governance needs to be established and an effective project roadmap is to be developed (see Figure 2). Governance and roadmap must, for instance, address the strong interdependencies between the various TOM dimensions and enable efficient decision-making. Equally, due to the long duration of TOM projects, governance and roadmap must be somewhat flexible in their scope in order to be able to absorb external as well as internal changes, which have an impact on the operating model.

Figure 2: Phases of a TOM

Figure 2: Phases of a TOMSuccess factors

Apart from a comprehensive view of the six relevant dimensions (see Figure 1) as well as a robust project governance and roadmap, zeb’s project experience in TOM projects suggests further key success factors:

Stakeholder commitment

Obtaining top management commitment is of paramount importance in any material change initiative. The particular challenge of TOM projects is to achieve cooperation amongst a very broad and diverse group of stakeholders ranging from top management to work councils /trade unions to financial supervisory authorities (e.g. in case of offshoring/outsourcing of activities). Furthermore, the cooperation needs to be maintained over a long project duration. Experience shows that commitments tend to diminish over time without constant interaction. Thus, continuous involvement of stakeholders is a key success factor.

Multidisciplinary project team

TOM projects, as outlined above, typically comprise a very broad spectrum of issues, which have to be addressed effectively. Consequently, a very broad set of skills is required in a project team to cover all relevant topics. The required set of skills typically ranges from specific functional expertise in order to effectively design the future organization and processes to technical know-how for shaping the future IT landscape as well as legal, compliance and tax expertise in order to prevent pitfalls. Furthermore, HR expertise is a necessity for planning and implementing adequate personnel related measures.

Project setup / governance

Due to the large scale of such change projects with many stakeholders and project participants, attention has to be paid to the setup of the project. Efficient project management as well as a strong PMO are key for success. In addition, a clear project governance has to be established so that—in case of any conflicts—a quick, central and irrevocable decision can be made.

Conclusion

zeb’s project experience in designing and implementing target operating models with leading universal and private banks suggests that, if done properly, TOM projects do have a tremendous positive impact on costs, service quality and operational risks. For instance, around 40% of personnel expenses have been cut, the STP rate has increased by a double-digit rate and the number of failed or late settlements has been reduced drastically in a TOM assignment for the investment banking division of a leading European bank. Of course, as any large-scale project, TOM assignments bear a significant risk of failure. However, with a clear focus on all relevant dimensions and the critical success factors, TOM projects will result in a winning operating model, that will enable the handling of increasingly hostile market conditions.

One response to “Target Operating Model (TOM) – Building solid grounds for your business model”

Andrew Campbell

Gregor and Sven, Nice article. Financial services companies clearly need root and branch reviews of their operating models. I like your chart – although I might suggest some changes to some of the specifics. You might like to look at the Operating Model Canvas – see http://www.operatingmodelcanvas.com – as another way of representing either an as is or to be operating model.