The following article summarizes the findings of Fidelio Tata (2018)[1]:

Corporate and investment banking (CIB) includes sales and trading in fixed income, currencies and commodities (FICC) as well as equities and derivatives, origination of debt and equity products (DCM and ECM, respectively), advisory services (including M&A) and prime services. European CIB is currently highly concentrated in London. If the United Kingdom were to leave the EU single market by the spring of 2019 (“hard Brexit”), UK- and, thus, London-based banks would lose their passport rights to do direct business with their clients in the other 30 European Economic Area (EEA) countries.

Utilizing available CIB data from various sources, we developed a simple framework that helps quantifying the impact of a hard Brexit on the other financial market hubs in Europe. Its main propositions are:

- Anywhere between 20 and 35% of the CIB business currently conducted out of London for clients headquartered inside the EEA (ex-UK) will migrate into the remaining EEA locations in case of a hard Brexit.

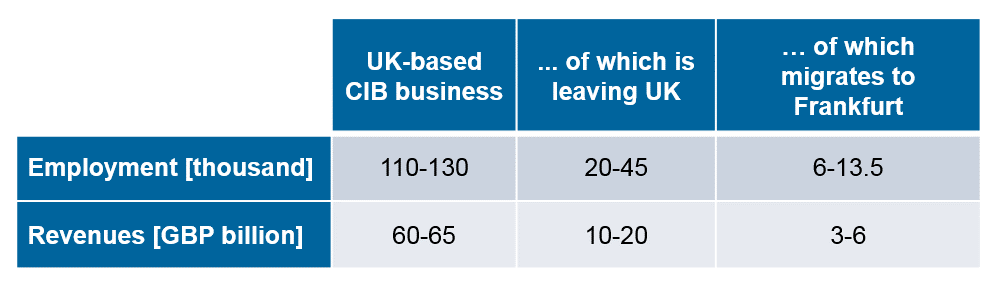

- This translates to some 20–45 thousand CIB employees leaving London for other EEA countries, resulting in a loss of CIB revenues of approximately GBP 10–20 billion per year.

- The most important criterion for selecting a new home of a bank’s CIB unit is close proximity to the CIB client base.

- Assuming a distribution of CIB business leaving London according to customers’ locations, weighted by sales and assets, Paris and Frankfurt would each capture roughly one-third, Amsterdam, Milan and Madrid each about 11%, and Dublin 3%.

Because Frankfurt and Paris benefit almost equally from CIB business leaving London, it is not likely that one of them can assume a market dominating position right after a hard Brexit.

For the financial market hub of Frankfurt, a hard Brexit would imply some 6-13.5 thousand additional jobs and GBP 3-6 billion in incremental annual CIB revenues.

Figure 1: network effects

Figure 1: network effectsWhile Frankfurt and Paris are expected to increase its CIB market share, London will continue to remain the prominent financial market hub. In addition, Frankfurt and Paris will continue to have a roughly equal market share in the near future. Even when assuming positive network effects in CIB banking, we do not expect any of the non-UK EEA financial centers to gain a dominating market position comparable to that of London any time soon.