So, what now?

Strong stock markets more than offset Q1 losses

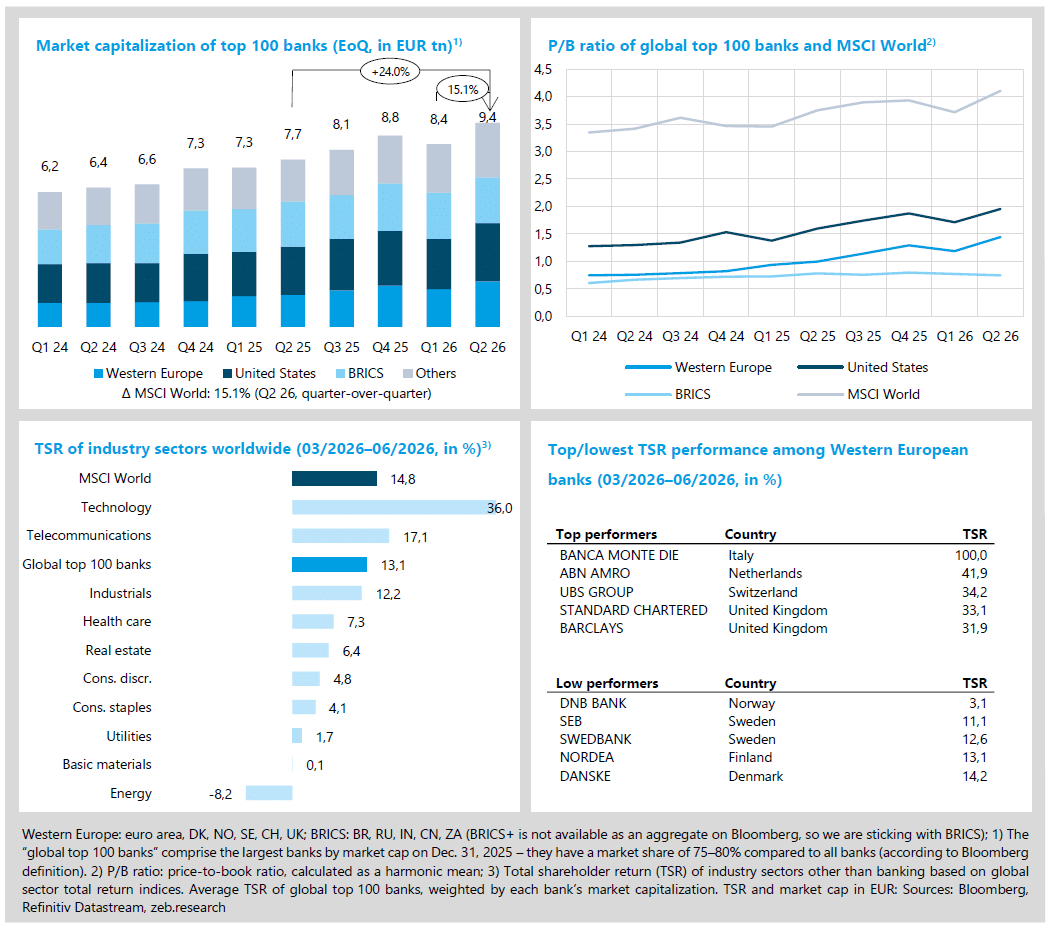

- Following losses in the first quarter of 2026 due to the war in the Middle East and the de facto closure of the Strait of Hormuz, total shareholder returns rebounded overall in Q2 2026 (MSCI World: +14.8% QoQ) – mainly driven by the technology and telecommunications sectors.

- Global banks followed the market trend and achieved a total shareholder return of +13.1% QoQ. European banks in particular posted significant gains (+24.8% QoQ). Strong quarterly earnings and the ECB’s somewhat surprising interest rate hike in June were the main drivers.

Resilient earnings in a volatile environment

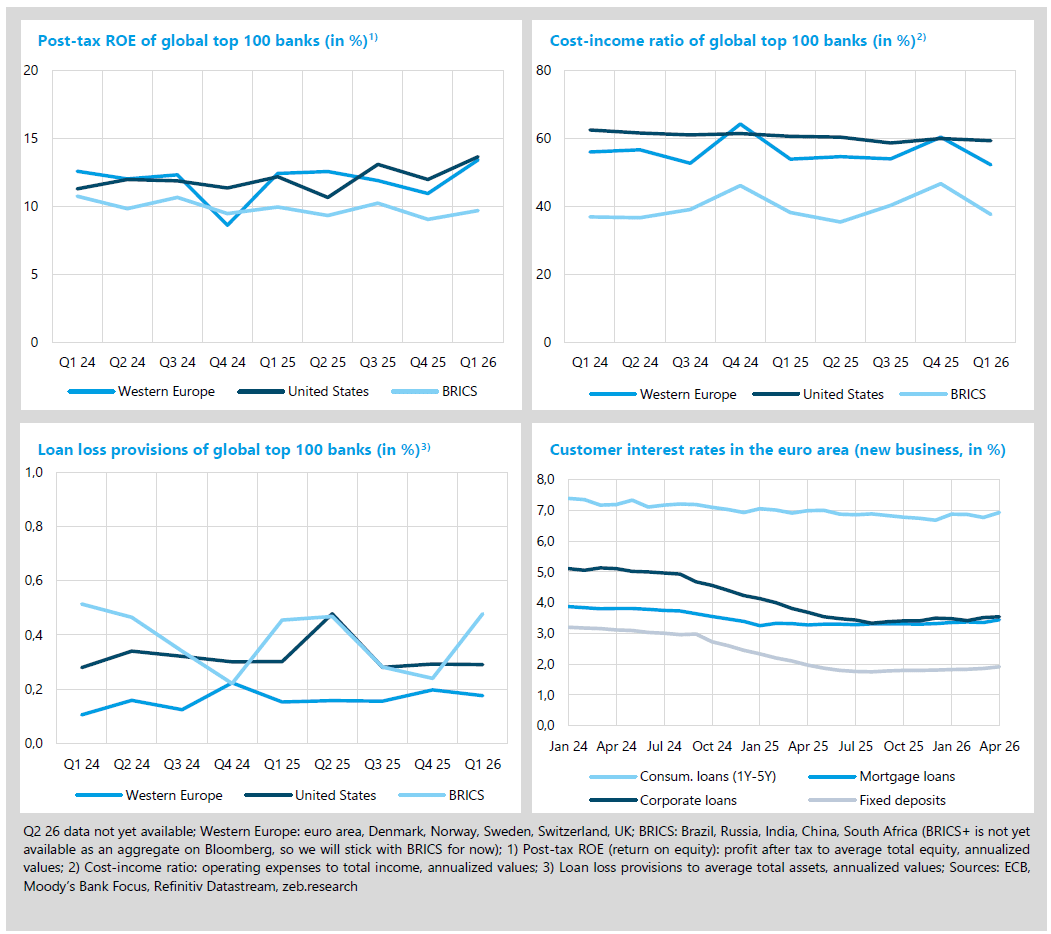

- Banks in Western Europe and the US got off to a strong start in 2026 and continued to increase their profitability. Western European institutions increased their ROE to 13.4% (+0.8 pp YoY), while US banks increased theirs to 13.7% (+1.5 pp YoY). This development was driven by solid earnings growth in both regions. In Western Europe, non-interest income grew more rapidly than net interest income, pointing to a more diversified revenue base; the ECB rate hike should provide additional support to European interest income.

- At the same time, the environment remains challenging: the war-induced energy price shock is adding inflationary and monetary policy pressure, while the growth outlook remains fragile, especially in Germany and Western Europe.

How did the world’s largest banks perform in Q2 2026?

Stock market rally despite uncertainties, inflation, and rate hikes

After the last quarter ended with losses for investors (MSCI World TSR Q1 2026: -1.6%, global top 100 banks: -2.9%), the stock markets returned to their original, long-term rally in the second quarter of 2026. Market capitalization and total shareholder return rebounded significantly. Yet many problems remain unresolved. Despite a memorandum of understanding between the United States and Iran, there is still uncertainty in the region, and shipping traffic in the Strait of Hormuz remains disrupted. The sharp rise in inflation expectations in March resulting from the energy price shock prompted the European Central Bank to raise its deposit rate by 25 bp to 2.25% in June. Especially European bank stocks (TSR: +24.8% in Q2 2026) benefited from the prospect of a “higher for longer” interest rate scenario. In the United States, too, hopes for interest rate cuts in the near future are steadily fading, despite the recent decline in energy prices – with positive effects for U.S. banks (TSR: 15.8% in Q2).

- The global stock market rose significantly in the second quarter. As a result, the MSCI World posted a TSR of 14.8% QoQ. However, this recovery was largely driven (once again) by technology and telecommunications stocks. Other sectors (e.g. consumer goods) lagged significantly behind.

- Among the top 100 banks, not only market capitalization but also PB ratios rose across the board.

- The strong performance of European banks was driven by good quarterly earnings, solid risk metrics, share buyback programs and hopes for a prolonged period of higher interest rates, fueled by the ECB’s latest interest rate decision. In addition to Banca Monte dei Paschi (takeover rumors), ABN AMRO, for example, reported success in its restructuring program and progress in the integration of its German subsidiary HAL as well as the takeover of Dutch bank NIBC. Hungary’s OTP continues to be rated positively for its expansionary CEE strategy (as well as for its strong KPIs).

Banks start the year strong – growth outlook remains bleak

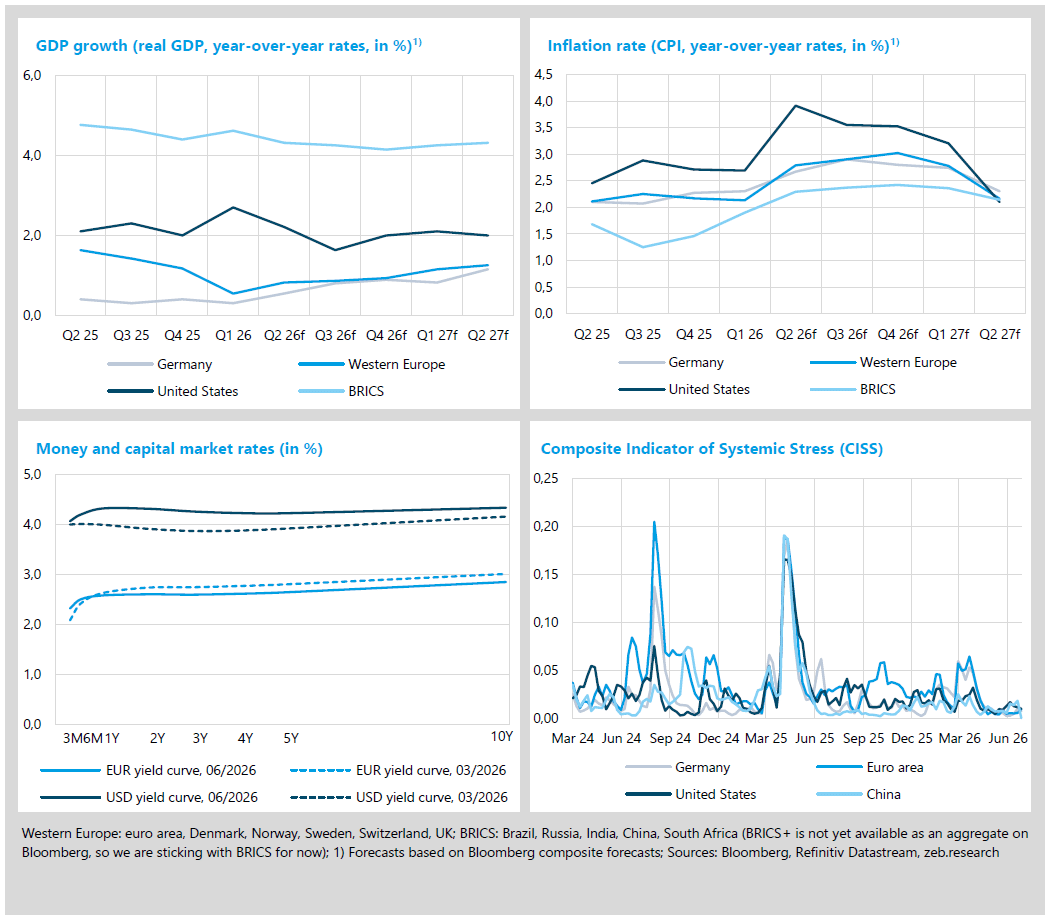

The war-induced energy price shock is now clearly reflected in the projected inflation rates for the second quarter: in Western Europe, the inflation rate will rise from 2.1% YoY in Q1 2026 to 2.8% YoY in Q2 2026; in the U.S., it is expected to rise temporarily to 3.9% YoY as a result of the energy price shock. Against this backdrop, the ECB raised its key interest rate by 25 bp in June. At the end of the quarter, however, the latest data suggest a certain easing on both sides. Falling oil and gas station prices are likely to further ease price pressures in July. At the same time, the economic outlook remains fragile: Germany’s economy grew by only 0.5% YoY in Q1 and is at risk of contracting again in the second quarter compared to the previous one; forecasts for Western Europe also suggest only a modest recovery. What is more, growth figures have repeatedly fallen short of projections – which were already modest – in the past. Although the U.S. economy continues to show greater resilience, its growth is heavily concentrated in net exports, consumption by high-income households, and AI- and technology-driven investments.

- The EUR yield curve has so far shown only a limited reaction to the ECB’s latest interest rate hike in June, but has flattened somewhat compared to the end of March, as expected: the spread between 10-year and 3-month bonds narrowed from 93 bp to 53 bp, bringing it closer to the US spread, which widened from 16 to 27 bp. Market movements suggest that the energy price shock is largely viewed as temporary and that no significantly tighter monetary policy is expected in the long term.

- The CISS has now returned to near-normal levels following the fluctuations caused by the escalation in the Middle East in Q1. As of the end of June, the indicators for Germany, the euro area and the U.S. are well below their March stress peaks. This indicates that the conflict is currently not being priced in as an immediate systemic risk to the financial markets.

In a challenging environment, banks on both sides of the Atlantic got off to a strong start in 2026. They further increased their returns on equity (ROE) in the first quarter compared with the same quarter of the previous year. Western European institutions increased their ROE year-over-year from 12.6% to 13.4%, while U.S. banks increased theirs from 12.2% to 13.7%. As a result of strong earnings growth, net income rose by 10.2% YoY in Western Europe and by 11.7% YoY in the U.S. At the same time, non-interest income in Western Europe grew at a significantly faster pace than interest income, indicating an increasingly diversified income base among the top banks. Potential consequences of geopolitical uncertainty may not yet be fully reflected in the reported Q1 earnings. The robust performance of the capital markets in the second quarter also points to continued strong profitability; furthermore, the ECB’s latest interest rate hike should support European banks’ net interest income.

- Banks in all regions under review improved their cost-to-income ratio (CIR) in Q1 26 compared with the same quarter of the previous year. Western European banks recorded the sharpest CIR decline: their CIR decreased by -1.7 pp YoY to 52.3%, as their income rose by +4.6% YoY– significantly faster than their costs (+1.3% YoY). U.S. banks reduced their CIR by -1.3 pp YoY to 59.4% (BRICS: -0.6 pp YoY to 37.7%); similar to European banks, income growth of +6.3% YoY outpaced the rise in costs of +4.0% YoY.

- In Western Europe, loan loss reserves rose slightly in Q1 26 by +2 bp YoY. This suggests that the growing global uncertainty and the weaker macroeconomic outlook have not (yet) been reflected in the risk provisions of European and U.S. institutions, although sharp increases can already be observed among BRICS banks.

- Customer interest rates in the euro area have risen in recent months across all types of loans. The main drivers are rising inflation expectations resulting from the escalation in the Middle East; the ECB’s interest rate hike in June is likely to further intensify upward pressure over the course of Q3.