To what extent is the escalation in the Middle East weighing on the capital markets?

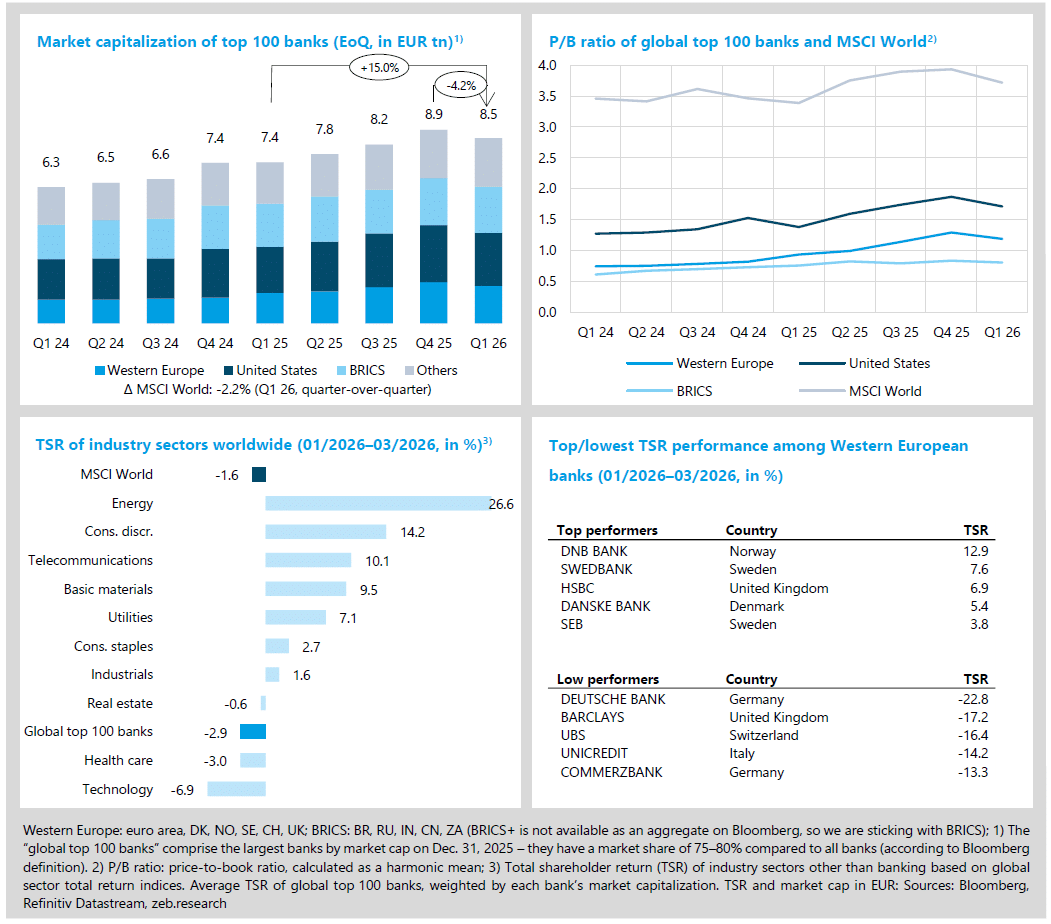

- After a good start to the year, the financial markets tipped into a new shock regime of rising energy prices, inflationary pressure and greatly increased uncertainty in Q1 2026 due to the escalation in the Middle East and the de facto closure of the vital global shipping route Strait of Hormuz (MSCI World market capitalization -2.2% QoQ).

- For banks, the negative factors predominated in the new market environment: the global top 100 banks lost -4.2% QoQ in market capitalization, the first QoQ decline in eleven quarters.

Does the current high level of profitability come with increasing risks?

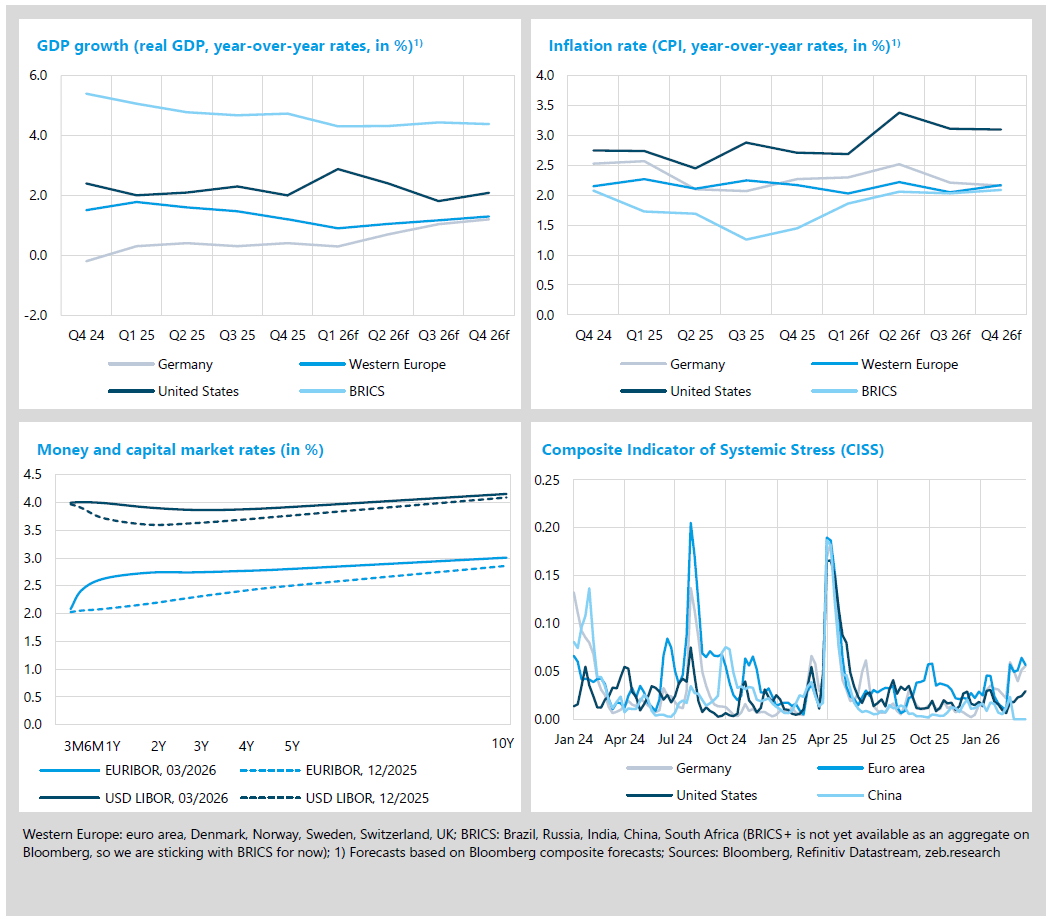

- After a slight decline in inflation in Western Europe in Q4 2025 (-0.08 pp QoQ to 2.17%), upside risks are once again emerging for 2026. Higher energy prices and potentially rising food prices as a result of the war in Iran are reinforcing price pressure and exacerbating the ECB’s monetary policy conflict of objectives in an already weak growth environment.

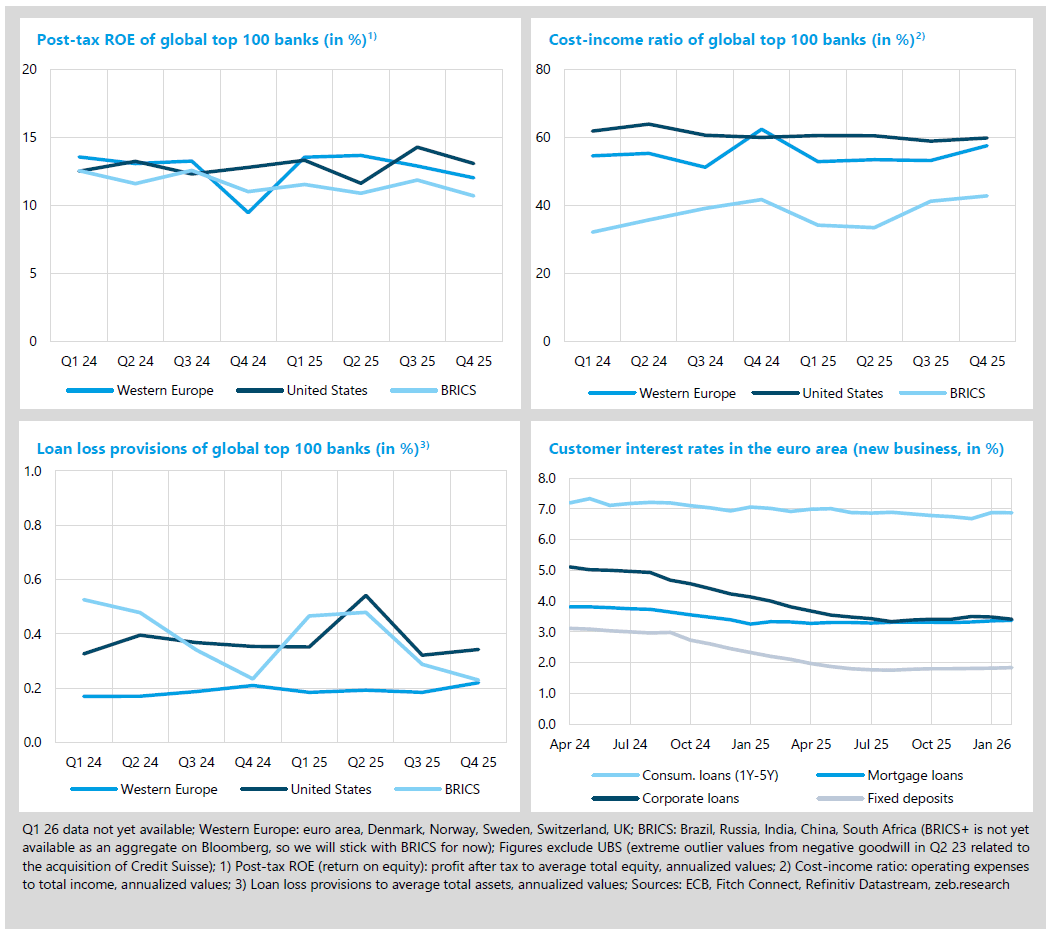

- The ROE of Western European banks rose year-over-year from 9.5% to 12.0% in Q4 2025, underlining their strong financial performance in 2025. However, Q1 2026 signals from the capital markets point to a normalization; under heightened geopolitical risks, the sustainability of the increased profitability is now being put to the test.

How are the capital markets developing in the context of the Iran war and inflation?

In Q1 26, after a good start to the quarter, the global capital markets saw a geopolitically triggered energy and inflation shock (MSCI World market cap. -2.2% QoQ) caused by the military escalation in the Middle East and the de facto closure of the Strait of Hormuz. The acute supply shock on the oil market led to the strongest inflation-adjusted increase in the Brent price since 1988 and was a major driver of the energy sector’s strong TSR performance (+26.6% QoQ). In contrast, the global top 100 banks recorded their first QoQ loss in eleven quarters (market cap. -4.2% QoQ). From an investor perspective, the negative implications for the banking industry – particularly stagflation risks, potentially weaker credit growth and rising cost of risk – currently dominate over the potential positive effects (“higher for longer” interest rates are bolstering deposit business; trading activities are benefiting from high volatility and trading volumes in the short term).

- Within the top 100 sample, the PB ratios dropped broadly in Q1 26: US banks fell to 1.72x (-0.15x QoQ) and Western European banks from 1.29x to 1.19x (-0.10x QoQ). Among the Western European banks, only three institutions managed to increase their PB ratio in the first quarter: DNB (+0.11x to 1.62x), HSBC (+0.05x to 1.28x) and BNP Paribas (+0.01x to 0.78x).

- Among the sectors, the oil price shock, higher real interest rates and a reassessment of the AI narrative are driving performance – energy (TSR +26.6% QoQ) is benefiting from tight global supply, strong margins and persistent geopolitical risks. Technology (TSR -6.9% QoQ) is bringing up the rear.

- TSR top performers among Western European banks were DNB with +12.9% QoQ (share buyback program in March, strong capitalization and relatively resilient domestic market) and Swedbank with +7.6% QoQ (DOJ money laundering investigation closed and released capital).

What macroeconomic headwinds are Europe’s banks facing?

Inflation in Western Europe in Q4 25 was slightly below the previous quarter at 2.17%. For Q1 26, however, inflation risks have increased again on both sides of the Atlantic. Rising energy prices due to the war in the Middle East and additional upside risks for food and goods prices are once again boosting price pressure. The inflation and growth forecasts shown in the charts are therefore likely to be too low, as the consequences of the conflict – due to the time lag in analysts’ forecasts – have not yet been fully taken into account. This is also indicated by the yield curves in Europe and the US, which flattened significantly again in Q1 26. Higher inflation expectations put pressure on the short end in particular; in the US, the curve at the short end turned inverse again, while the 10Y–2Y spread remained positive at around 25 bp. Central banks thus remain caught between already subdued growth and the fight against inflation – interest rate cuts for 2026 have become much less likely.

- In Western Europe, growth in Q4 25 remained moderate at +1.2% YoY, but the outlook has deteriorated noticeably due to the Iran war. The US grew significantly more strongly at +2.0% YoY, but the conflict is also likely to dampen growth prospects there – despite robust expectations for the first quarter so far.

- The CISS index measures the systemic stress in the financial system using 15 market-related indicators from money, bond, stock, foreign exchange and banking markets. In Europe, Germany and the US, the indicator has recently picked up again slightly in the context of the war in the Middle East. However, the swings have so far remained well below the level of 2025, when the markets came under noticeable pressure in the wake of President Trump’s tariff announcements and the resulting increase in trade tensions.

Profitability showed a mixed picture in a year-over-year comparison. In the US, ROE rose slightly from 12.8% to 13.1%, while net income fell by -4.5% YoY. In Western Europe, ROE improved significantly from 9.5% to 12.0%, accompanied by an increase in net income of +38.3% YoY. The Western European institutions thus once again confirmed their strong banking year 2025. By contrast, the ROE of the BRICS banks fell from 11.0% to 10.7% YoY. However, the weaker capital market data in Q1 26 suggests that the banking market is gradually normalizing after the strong (Western European) year before. It should now become clear how sustainable the institutions’ profitability is under less favorable conditions. Additional uncertainty is brought about by the conflict in the Middle East, as geopolitical tensions are exacerbating market conditions and putting further pressure on the risk environment for the banking industry.

- In Western Europe, the cost-income ratio (CIR) improved significantly by -4.8 pp QoQ to 6%.

Although income fell by -2.6% year-over-year, costs dropped even more sharply by -10.2% YoY, as efficiency programs and lower variable remuneration made an impact. In the US, the CIR in Q4 25 was 59.9% and thus only slightly below the previous year’s figure (-0.16 pp YoY); income and costs there declined almost in tandem at -4.8% YoY and -5.0% YoY respectively. - Loan loss provisions were roughly constant year-over-year; in Western Europe they increased slightly by +1 bp YoY, while in the US they fell slightly by -1 bp YoY.

- Customer interest rates have remained largely stable in recent months. However, consumer loans (1–5 years) have recently shown signs of a slight increase, also against the backdrop of higher inflation expectations as a result of the Iran war. In the future, this upward pressure is also likely to become increasingly noticeable in the other customer interest rates.