European banks are at a crossroads

At the beginning of 2018 it seems to us that European banking is at a crossroads. The turbulent and stormy times following on from the banking crisis of 2009 and the euro zone crisis of 2010–2015 are, so to speak, in the rear view mirror. We have entered a period of relative calm with little immediate danger from bank failures or sovereign debt crises. Indeed, countries right across Europe are registering relatively strong GDP growth, the euro is strengthening against the dollar and the pound, the ECB is beginning to think about removal of stimulus, and European stock markets are recovering strongly. Banks are no longer in disaster prevention mode, but can instead take a moment for sober reflection on their situation and that of the industry in order to define the tasks ahead. It is likely they will conclude that while many exciting opportunities for improvement and growth do exist, the overall health of the industry is not good.

Poor profitability of European banks is the core challenge

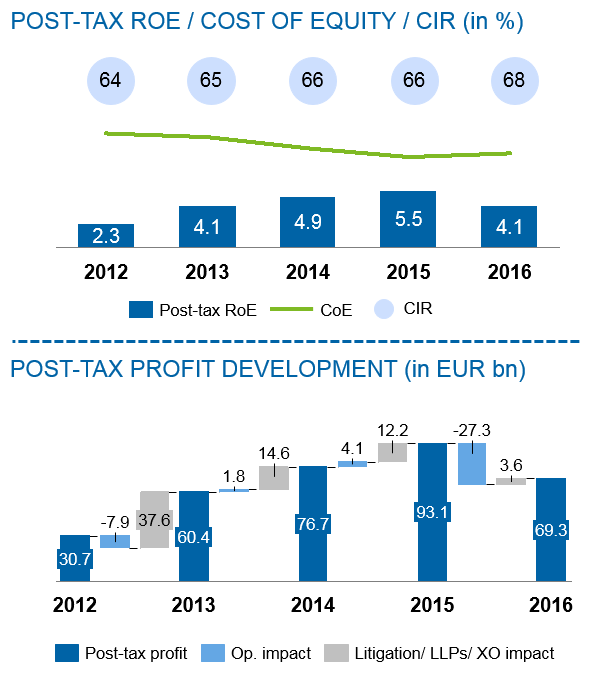

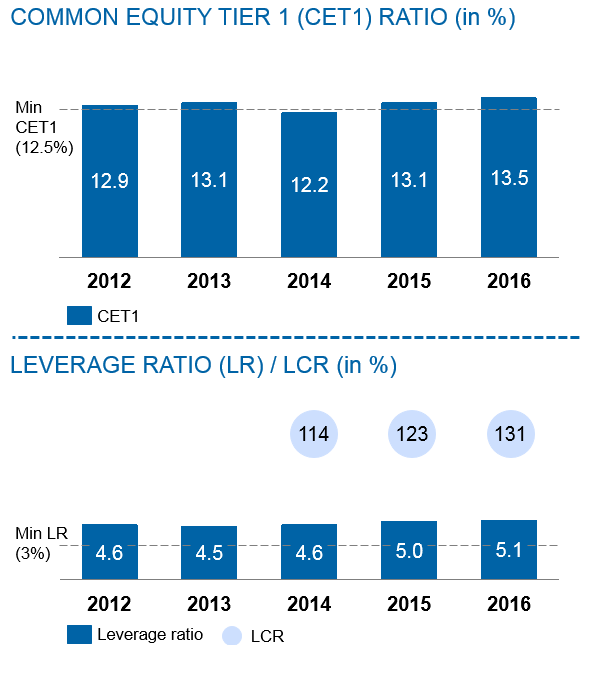

The most pressing problem facing the European banking industry is profitability. The average RoE of the top 50 banks in Europe, accounting for 61% of all assets in the industry, was 4.1% in 2016, down from 5.5% in 2015. This level of profitability is about half of what shareholders should expect based on a standard cost of equity calculation. Predictably, this poor performance is reflected in European banks’ share prices which are depressed with price-to-book ratios of less than 1. A drill down into the figures does not improve the picture: all of the improvement in European bank profitability since 2012 has arisen from year-over-year reductions in loan loss provisions and extraordinary items associated with the crisis period. Actual organic profitability of Europe’s top 50 banks, on the other hand, has declined significantly since 2012. This is an unimpressive performance and it is certainly concerning that organic profitability is lower in 2016 than it was in 2012. The top 50 banks have succeeded, however, in strengthening their capital positions with a common equity tier 1 ratio of 13.5% in 2016. As if to add insult to injury, upcoming regulation and a continuation of the relatively low yield environment will increase the burden on these banks. Without management action, we estimate in a baseline scenario that return on equity (RoE) might fall to 1.5% and common equity tier 1 ratios (CET1 ratios) below the average market and regulatory minimum.

Management can transform the profitability of European banks

The poor level of profitability is clearly an overriding issue for the industry. We are, nevertheless, confident that European bankers can and will solve this problem successfully. Classic cost and revenue management, when done with skill and energy, can transform the profitability of these institutions to a level that will satisfy shareholders. Aggressive balance sheet management using new risk management techniques can preserve and enhance capital ratios even as regulators stiffen prudential regulation. Non-traditional competitors may challenge banks with innovative digital initiatives but banks will respond with interesting digital initiatives of their own that will create new, profitable growth opportunities. And banking industry consolidation will continue and accelerate: with 7,110 banking institutions in the European single market and 8,179 if we add the markets in Norway, Russia, Switzerland and Turkey it is time for a more sensible industry structure to emerge. Our view, therefore, is that four major trends will dominate the European banking scene from now until 2021 in response to the current unhealthy situation of the industry. These are:

- Aggressive cost and revenue management with continuous restructuring and a constant flow of tactical initiatives aimed at improving cost-income ratios;

- Restructuring of balance sheets as banks shed their most capital intensive assets to improve capital ratios. Alternative financing vehicles for risky/capital intensive lending will (re-)emerge such as securitisation for example;

- Serious experimentation with radical new business models in the digital space. This trend will be about leveraging data and customer insight while moving away from big balance sheets and heavy infrastructure. Non-traditional players will be challenging banks in this space. Whilst we do not expect disruptive change to emerge, we can already observe a steady and sustainable move in this direction;

- Widespread industry consolidation, particularly in the most fragmented markets such as Germany and Austria, in order to maximise economies of scale and efficiency. A number of efficient large banks will become expert at “hoovering up” smaller and less efficient banks.

Our exhaustive financial modelling of the top 50 banks, described in more detail in the body of the report, demonstrates that these development paths can totally transform the profitability of European banks while preserving their capital positions and financial strength. Pursuing these opportunities is a must: our modelling also shows that without decisive management action profitability and financial strength could actually deteriorate over the next five years.

Mastering the challenge will require determination and vision

These next few years will therefore be a time of intense activity for European bankers, regulators and politicians. The need for change in European banking is evident, but it will not occur without effort and, indeed, risk, for all stakeholders. The driving forces of increased capital regulation, low yields, shareholder pressure for results and rapid digital innovation will weigh heavily on traditional European balance sheet banking. Regulators

and politicians, for their part, will have to decide whether ever harsher regulation has its own negative systemic effects in terms of helping to create an unhealthy low return banking sector that struggles to retain profits or attract private capital. European bankers, on the other hand, must strive to create more efficient banks by aggressively pursuing the opportunities described above. So while the volume of change and innovation we expect to see is very necessary to restore the health of the banking system, it will certainly test the flexibility, vision and determination of European bankers, regulators and politicians in the years to come.

For further information please contact london@zeb.co.uk.