Introduction

The Liquidity Coverage Ratio (LCR) is one such measure and has the aim of securing institutions’ short-term financial solvency in a hard 30 calendar day stress scenario at any time—also in times of crises. Another significant measure for strengthening banks’ medium to long-term liquidity profiles is the Net Stable Funding Ratio (NSFR). It requires banks to ensure a sustainable maturity structure of assets and liabilities. By limiting maturity mismatches, NSFR reduces rollover risk and promotes funding stability.

While NSFR will become a minimum standard by 2018 according to Pillar I requirements, banks already have to fulfill a minimum LCR of at least 70%. Within the next few years, the minimum threshold will be continuously increased until 2018, when supervisory authorities will require the fulfillment of the total 100%. Due to considerable challenges concerning the implementation of these liquidity ratios, institutions have mainly focused on appropriately calculating and reporting LCR and NSFR until now. Building on that, their focus will shift to integrating these liquidity ratios into the bank’s internal liquidity management system, with the aim of being able to analyze and forecast the ratios and conduct what-if analyses.

Requirements for LCR and NSFR simulation

Supervisory reporting and best practice standards drive the implementation of LCR and NSFR simulation. The following Figure 1 outlines the requirements for the implementation of LCR and NSFR simulation.

Figure 1: Requirements for LCR and NSFR simulation

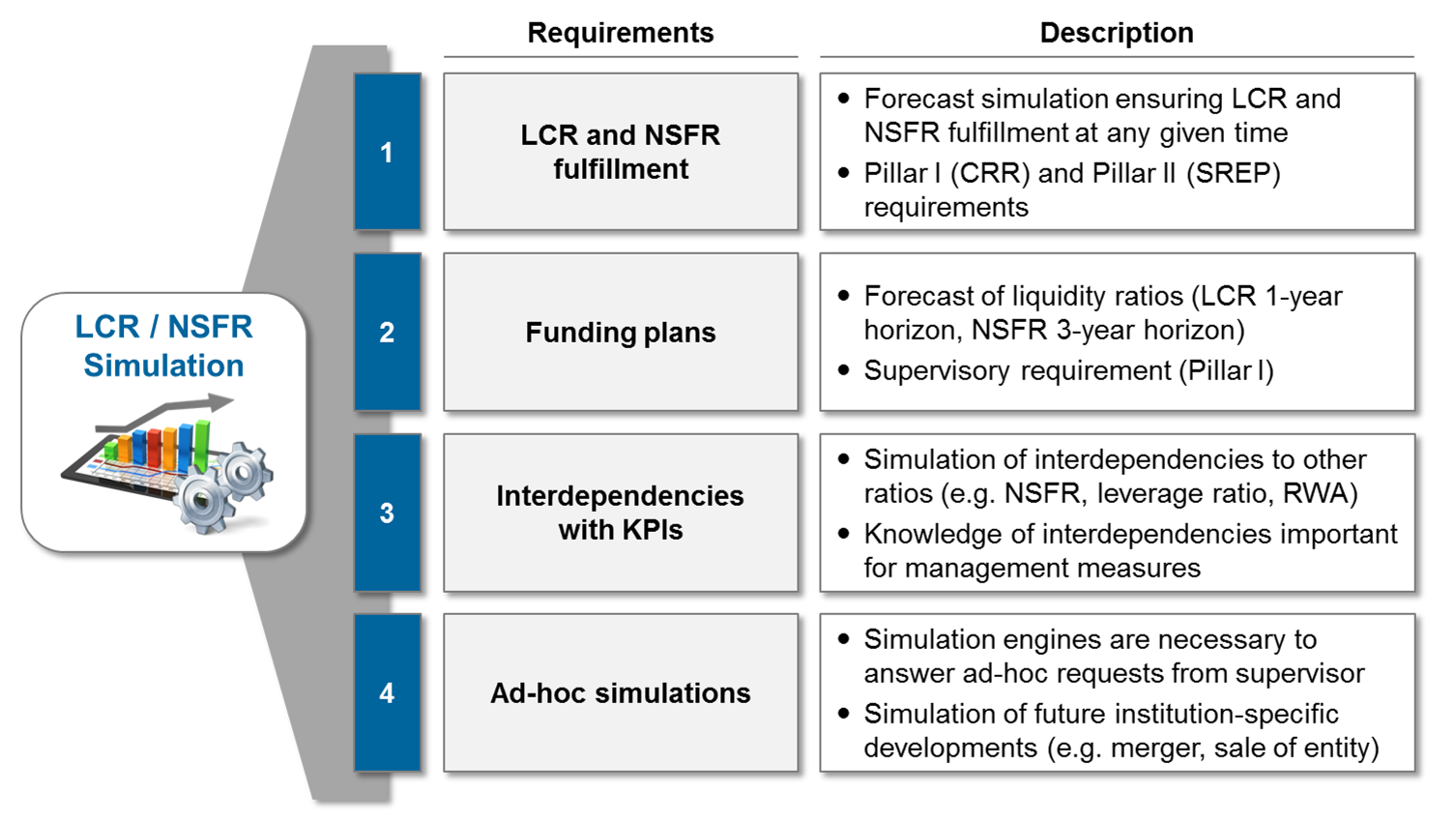

Figure 1: Requirements for LCR and NSFR simulation1) LCR and NSFR fulfillment

The LCR has been a minimum standard since October 2015. LCR currently has to equal or exceed a statutory threshold of 70% according to Pillar I requirements. LCR simulation and, in particular, forecasting ensures the fulfillment of the LCR at any given time. This is of particular importance due to specified regulatory consequences that banks have to bear if they fall below the respective minimum LCR standard. According to Article 4 (4) of the Delegated Act Liquidity, one of these measures is that institutions have to submit a plan for the timely restoration of compliance to the competent authorities, as laid down in Article 414 of the CRR. In addition to that, the competent authority can require reporting on a daily basis.

In contrast to LCR, NSFR is not yet a minimum standard. Nevertheless, NSFR should also be considered in the simulation framework for ensuring sufficient stable funding at any time.

2) Funding plans

In June 2014, the European Banking Authority (EBA) published guidelines on harmonized definitions and templates for funding plans of credit institutions. These templates also contain requirements regarding the simulation of LCR and NSFR. In particular, they require projections of LCR for one year and NSFR for up to three years.

3) Interdependencies with KPIs

It is important to determine interdependencies between different KPIs, specifically the impact of planned operational and strategic measures. As an example, banks should always be very interested in understanding the impact of LCR and NSFR optimization measures on other limited KPIs, such as the capital ratio, the cost income ratio and return on equity.

4) Ad-hoc simulations

Especially in the context of pillar II requirements, ECB is entitled to demand ad-hoc reports. In order for banks to fulfill these ad-hoc requests, they require a sound simulation solution so that they can respond to the supervisory authorities in a timely manner. Moreover, a simulation engine ensures the simulation of future institution-specific developments, such as a merger or sale of entity.

Best Practice IT simulation framework

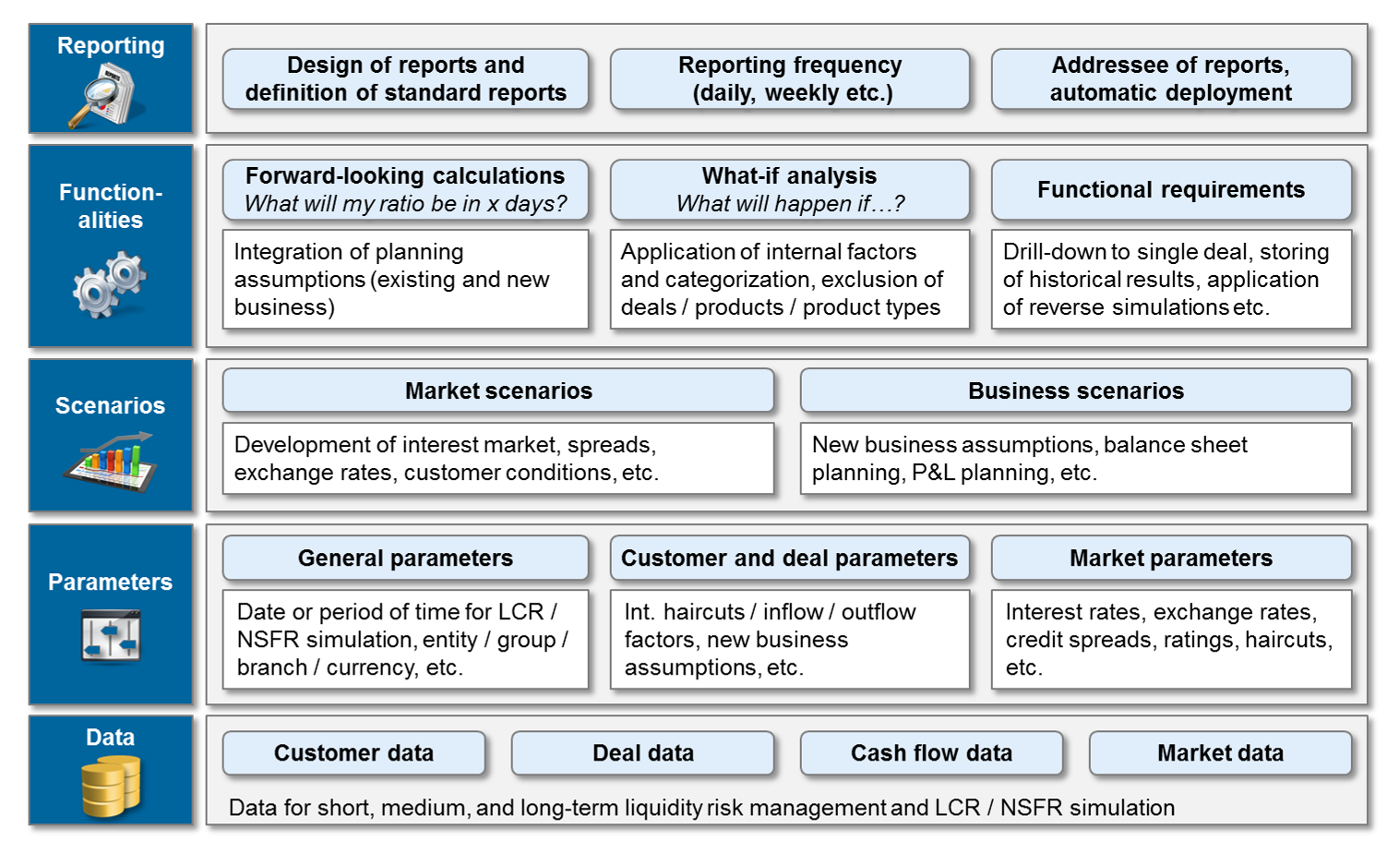

Based on the requirements for LCR and NSFR simulation, zeb has developed a best practice IT framework. The framework comprises five major building blocks that need to be integrated within banks’ internal liquidity management architectures, leading to sound and efficient LCR and NSFR simulation.

The building blocks and their characteristics are illustrated in Figure 2.

Figure 2: IT simulation framework for LCR and NSFR

Figure 2: IT simulation framework for LCR and NSFRData delivery and proper data quality are fundamental to a successful simulation environment. The data delivery has to comprise customer information, cash flows, market data and all relevant deals (including interest information). Depending on the required simulation detail, different levels of aggregated data can be used or even single deal level data. The calculation frequencies are the main driver for the data delivery schedule. In order to ensure timely delivery, harmonized system interfaces from the different source systems are required.

The parameters are used as input factors to characterize the single instance of an LCR and NSFR simulation run. Two types of parameters are differentiated. General parameters describe basic characteristics for each LCR and NSFR simulation run, e.g. for which date the simulation should be conducted and which dimensions (organizational unit, business area, currency, etc.) should be considered. The second type comprises customer, deal and market specific parameters. These parameters are used to define and parameterize the scenarios.

The scenarios are the centerpiece of the LCR and NSFR simulation framework. In general, market scenarios and business scenarios can be distinguished—the market scenarios describe the future market situation, e.g. the development of reference interest rates, while the business scenarios reflect the bank’s internal business assumptions, e.g. development of balance sheet growth. In particular, this refers to the application of institution-specific weighting factors, consideration or exclusion of single deals, products, portfolios, etc.

The parameters together with the data (customer, deal, cash flow and market data) under application of the defined scenarios become the input for the simulation run. The LCR and NSFR simulation tool should provide the following simulation functionalities:

- Forward looking calculations that allow the forecasting of LCR and NSFR for a specific timeframe under consideration of existing business, rollover assumptions and new business assumptions.

- A what-if analysis that determines how LCR and NSFR will be affected under application of specific measures within the market and business scenarios.

The results of the LCR and NSFR simulation run should be visualized in a dedicated reporting cockpit that provides a clear and structured overview. Among others, the following functionalities should be supported by the reporting cockpit:

- Overview of calculated ratio and drill-down to a predefined granularity level

- Selection of specific dimensions (e.g. organization, business area)

- Forecast and evolution of LCR and NSFR ratios

- Export functionality to Excel, PDF, etc.

Summary

Regulatory requirements and internal needs emphasize the importance of a comprehensive LCR and NSFR simulation solution that is incorporated in the institution’s bank management framework. To ensure that LCR and NSFR simulation is successfully implemented, the following questions about the five building blocks of IT simulation must be answered:

- Data: What data is required and from where and when can it be retrieved?

- Parameters: What input factors should be available for configuring the simulation run?

- Scenarios: What are the interesting scenarios (market / business) and how should these scenarios be represented?

- Functionalities: How are scenarios and parameters interlinked and which additional functionalities are required?

- Reporting: Who is the target reader of the simulation results and how should the results be presented?

To conclude, a simulation solution provides institutions with a powerful tool to not only fulfill regulatory requirements in the context of LCR and NSFR reporting but also allows them to understand impacts of changes in the business structure and provides reasoning for strategic decision making.

2 responses to “LCR and NSFR simulation”

Mahzad

Hello

I’m a postgraduate student in financial engineering field and my thesis is about modeling liquidity gap between uses and sources of funds in a bank. It was surprising to me that there is a group working on such a program. I don’t know what i exactly receive by subscribing but i would be thankful for that which may help me on my course.

With best regards and good luck.

Jonathan Rorobi

Yes a specific discipline in Banking Treasury Department called ALM (Asset Liability Management) handles this specifically.