Who in open banking is afraid of the “big bank”?

How do “winner-takes-all situations” come about?

Winner-take-all situations occur in environments where network effects are in play. Simply put, network effects are the phenomenon where an increased number of users adds value to the good or service they are using. Powerful network effects have been observed in various industries where the right factors were in place. In particular, the introduction of the Internet has greatly increased the number of network effects due to the increased accessibility to goods and services for all Internet users.

In economies where network effects are present a critical mass of users can be reached. This critical mass occurs when a single good or service becomes better than all others. As a result, the market for that specific good or service turns into a winner-take-all situation as all users gravitate to the best goods or service provider.

Network effect in practice: Facebook is an excellent example of a service where a winner-take-all situation took place. Before Facebook dominated the social media service, there were multiple competitors within the US and in various countries in the social media field. However, as strong network effects were in place, users naturally preferred to use a service with more users, in this case, where most friends were signed up. Facebook quickly achieved this critical mass and dominated the social media service.

Why we believe it is an opportunity for banking

There are multiple banking trends, but also general market trends, which are shifting banking towards a territory in which network effects can come into play.

- Clients are demanding that banking services are put into a personalized context and have shown that they are willing to share their data to enable that

- The entities consuming client data are able to easily customize the product and service provisioning (“mass customization”)

- The practice of securely sharing financial data, subject to customer consent through PSD2 results in a term known as open banking. This enables others, not necessarily banks, to make use of client data to push their own innovative products and services

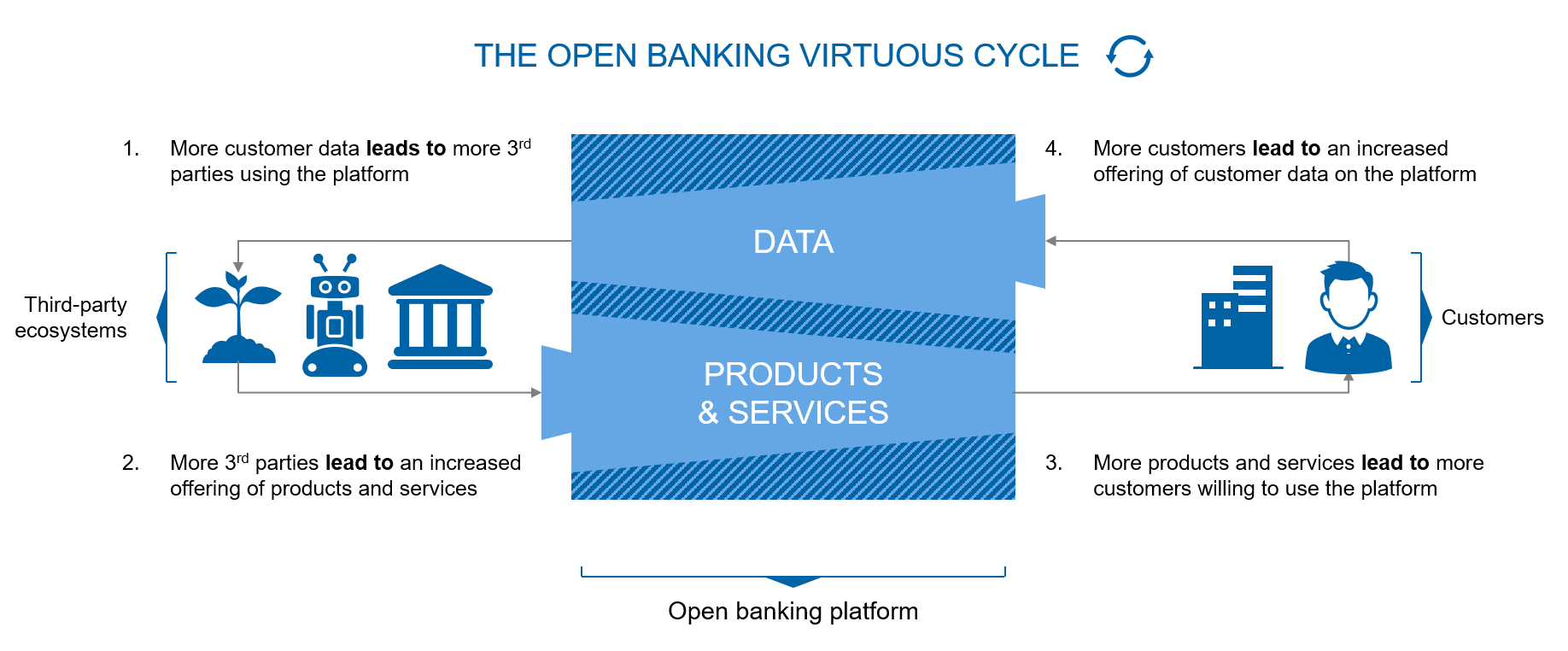

Below we have depicted a simplified illustration of the network effect which can occur in the banking market. We believe that, given the right incentives, open banking has the potential to create a self-fulfilling virtuous cycle which will result in a network effect. This network effect is possible if an entity manages to harness both sides of the spectrum, namely the customer data as well as the products and services, on a single platform.

Banks are already making use of this possibility through their aggregation strategies, e.g. through managing all clients’ current accounts in their online banking and adding nearbanking value adding services on top, such as personal finance and/or subscription management. A prominent example of such an offering is that of Swedbank with a fintech cooperation partner Minna, as well as Erste Group’s George environment.

Just as in any network effect, if an increased number of users adds value to the good or service they are using, it will create a gravitation of users towards fewer platforms, until only one single platform will come to dominate the market. We would like to further explore this theoretical possibility.

Figure 1: The open banking virtuous cycle

Figure 1: The open banking virtuous cycleWho is able to become “the banking platform” in open banking?

Banks and bigtech companies are currently in a prime position

There are two types of players who currently have the capabilities to become the ones to dominate the open banking market and therefore potentially become the winner-take-all open banking platform: incumbent banks and bigtechs, major technology companies (GAFA).

Both players have three of four key success factors. Banks are currently in a prime position as they have the client data, the financial services know-how and the capital to successfully react to the developments in the open banking market, whereas bigtechs provide modern IT capabilities instead of financial services know-how.

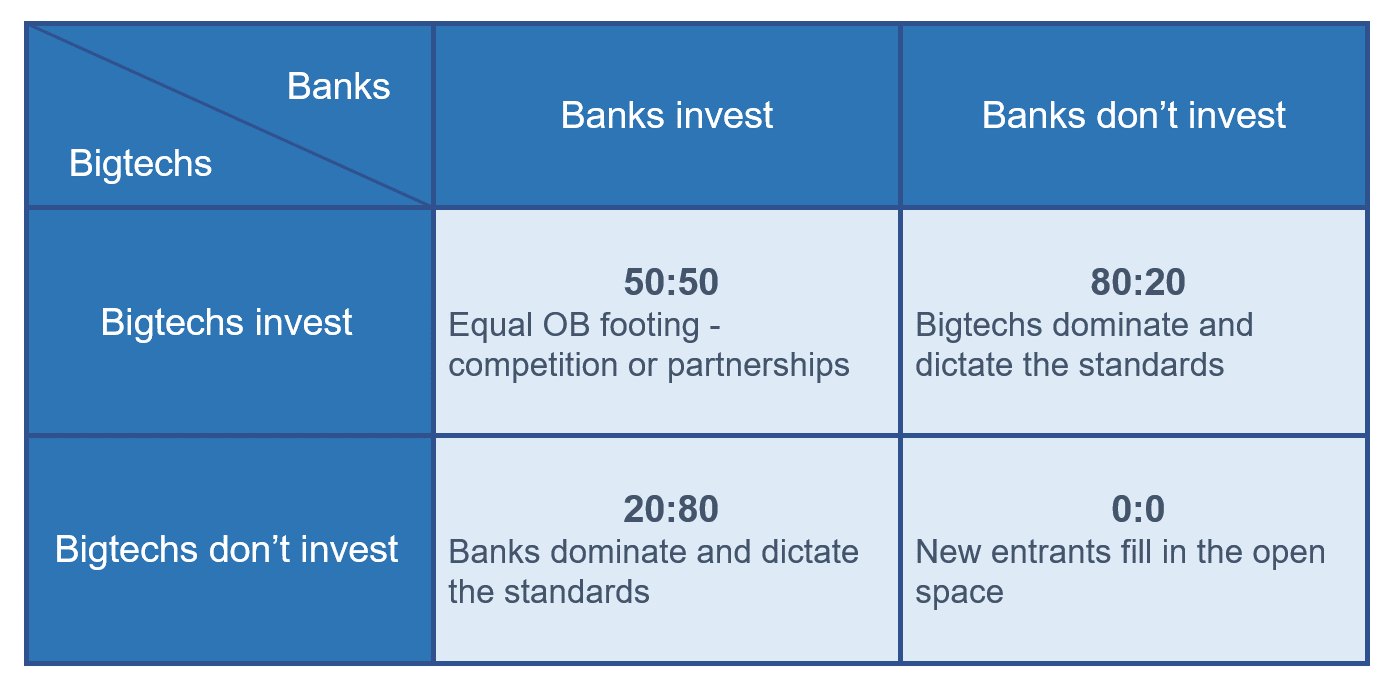

In the figure below we take a look at the choices banks and bigtechs are currently facing. This creates a classical prisoner’s dilemma in which banks and bigtechs are hesitant to fully open themselves towards open banking due to the investment this entails. Therefore it can be said that the open banking market is currently in the bottom-right quadrant, where third parties fill in the space left by their larger counterparts. The game depicted is played periodically. However, there are significant future benefits for players who are investing now, which forces banks to act now in order to remain relevant in the open banking market.

An important takeaway from the open banking prisoner’s dilemma is that it is clear that the players who do not react on time will be left behind as their current temporary advantageous positions gradually degrade relative to the other players, whether these are other banks, bigtechs, or up-and-coming third parties. Further, it highlights that instead of competing head-on against the big techs, it might be a good idea to think about partnerships and cooperation.

Figure 2: Open banking: Prisoner's dilemma and related payoffs

Figure 2: Open banking: Prisoner's dilemma and related payoffsAs bigtechs are already investing into banking use cases, banks basically have to follow. If they cannot partner on equal terms with bigtechs, they can build on partnerships with up-and-coming players who offer technological affinity as a strength.

Additional considerations on winner-takes-all situation in open banking

Banks were never able to fully consolidate large chunks of the European market due to persisting regulatory and regional barriers. These barriers were exploited, allowing national and regional banks players to entrench themselves in their respective markets.

This entrenchment strategy and regional exclusivity will weaken as the barriers surrounding banks are gradually opened. With the infrastructure and data of banks being shared and accessible to all, building the “single banking platform” is possible across a market with a single set of standards (regulatory and technical). PSD2 is a first step into the direction of setting a single standard for a secure exchange of information for the benefit of customers across Europe.

We believe in a further alignment of regulatory and technical standards in Europe, which will gradually reduce the value of local market presence and enable bigtechs to move into banking more aggressively. This is why even an extreme winner-take-all scenario needs to be considered in strategic planning for the period 2020–25…