European Banking Study shows: core problem of the banking sector persists

Despite some undeniable improvements—for instance, many banks’ capitalization and liquidity are clearly above the minimum requirements—the sector’s key issue remains unresolved: many institutions are facing structural performance issues, or, to put it bluntly, they are simply not earning enough money in the core areas of their banking business. Unfortunately, this is not a new insight, but rather a consistent finding since the first European Banking Study six years ago. Although Europe’s top 50 banks were able to increase their post-tax return on equity slightly from 6.6% (in 2017) to 7.2% (in 2018), their profitability remains low and more than ten years after the financial crisis, it is still below the capital market’s requirements. Most of the large European institutions neither managed to achieve sustained increases in operating earnings nor to improve their cost basis to the required degree.

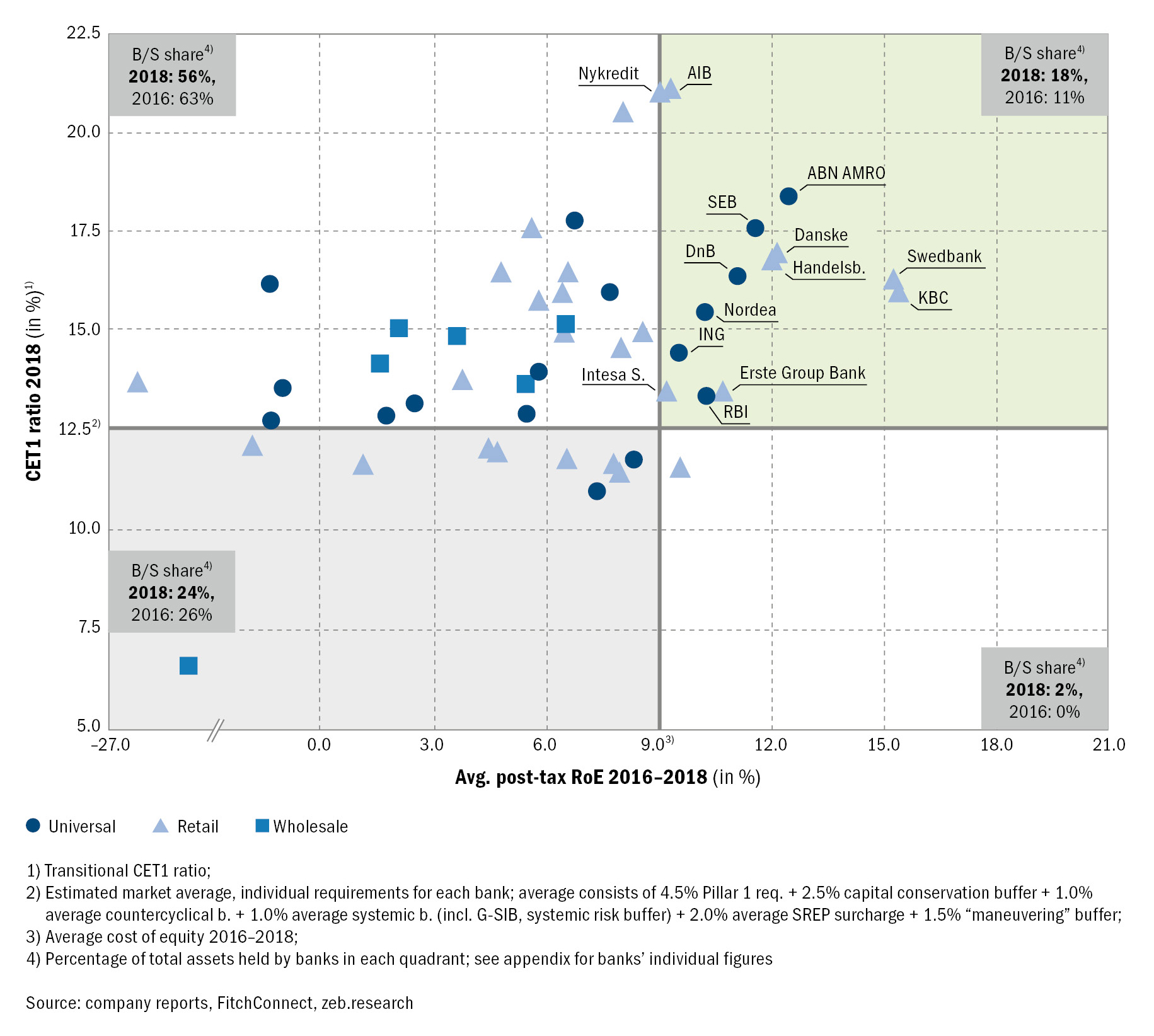

Of course, there are also successful banks in the market. Especially some mid-sized, less complex institutions focused on specific customers, products or regions are ahead of the pack. On the whole, however, only 14 out of the 50 largest European banks that we analyzed achieved a sufficient CET1 ratio and a post-tax return on equity above their cost of equity (see figure 1).

Figure 1: Profitability and capitalization of the 50 largest European banks

Figure 1: Profitability and capitalization of the 50 largest European banksScenario analysis reveals: structural problems of the European banking sector will increase

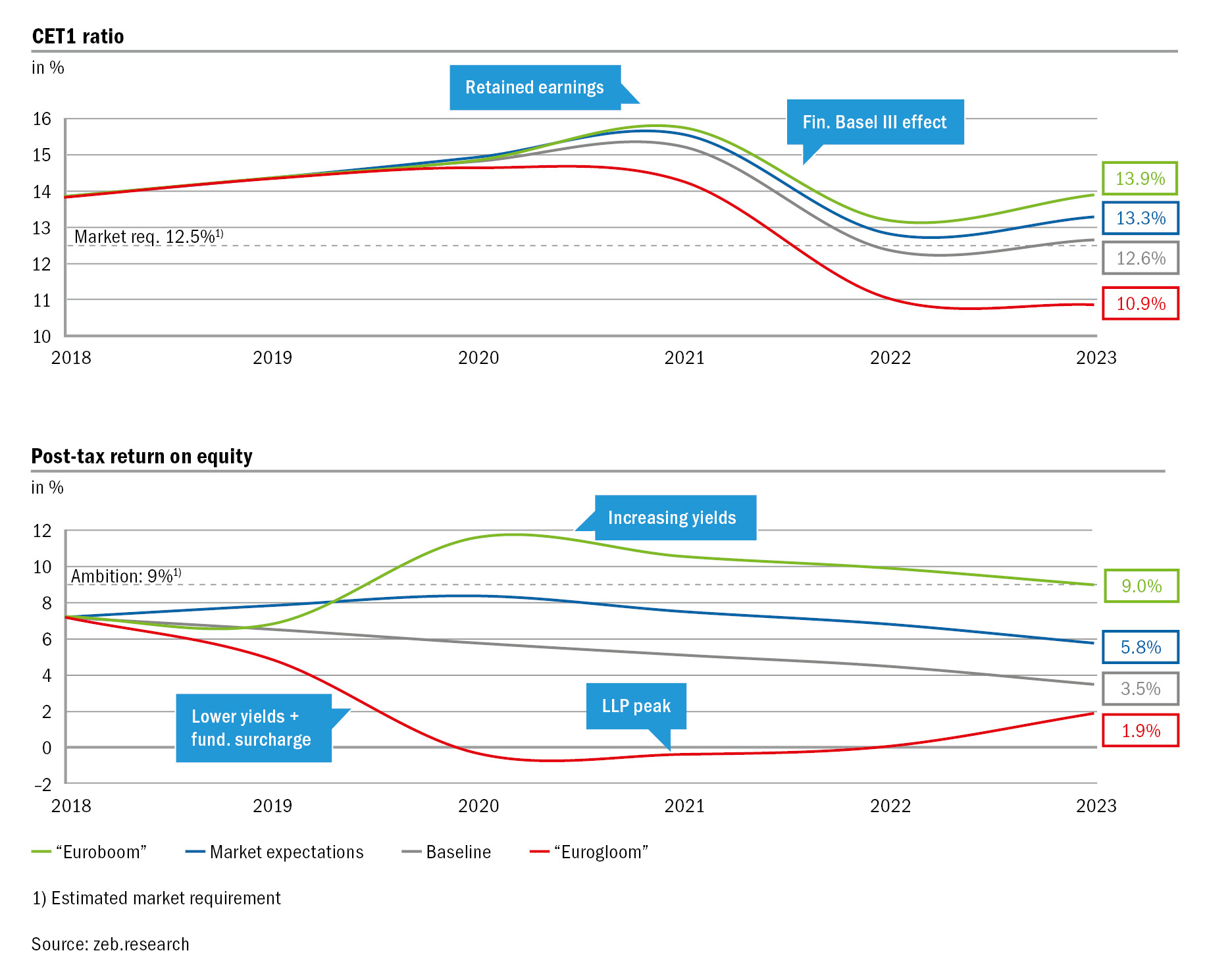

A look into the future using zeb’s holistic, proprietary simulation model indicates that the underlying problems of the banking sector are even likely to worsen. All our scenarios paint a troubling picture for an industry facing what could be a perfect storm of adverse economic and regulatory developments in the coming years. In this context, the European Banking Study examines three scenarios in detail.

In the most likely scenario (“Market expectations”) assuming moderately rising interest rates and increasing loan defaults, banks’ capitalization and profitability will both be lower in 2023 than they are today, unless banks manage to radically restructure their business models. Rising costs of risk and further increasing regulatory costs thus exacerbate the core problem that already exists today. Even in our most optimistic, yet also least likely “Euroboom” scenario, banks on average only just fulfill investors’ profitability expectations. Figure 2 summarizes the effects of the various scenarios.

Figure 2: Scenario analysis results—average of top 50 banks

Figure 2: Scenario analysis results—average of top 50 banksHow can Europe’s banks avoid sinking further into stagnation?

The latest edition of the European Banking Study investigates if and how digitalization—the hottest topic across the whole industry—could be the “silver bullet” that delivers long-term profits and saves banks from the impending storm. Taking a closer look at the various institutions and their level of digitalization, three main groups can be determined:

“Pioneers” that started focusing on digitalization early on,

“Challengers” that evolved their business model digitally only over the past few years, but then all the more intensively, and

“Followers”, currently exhibiting a lower degree of digitalization on an overall level compared to other banks (digital excellence in certain sub-areas, however, not excluded).

The group of “pioneers” consists mainly of banks with a strong retail or customer focus as well as less complex universal banks, while wholesale banks in particular and various complex, large universal banks (large bank groups) make up the “followers”.

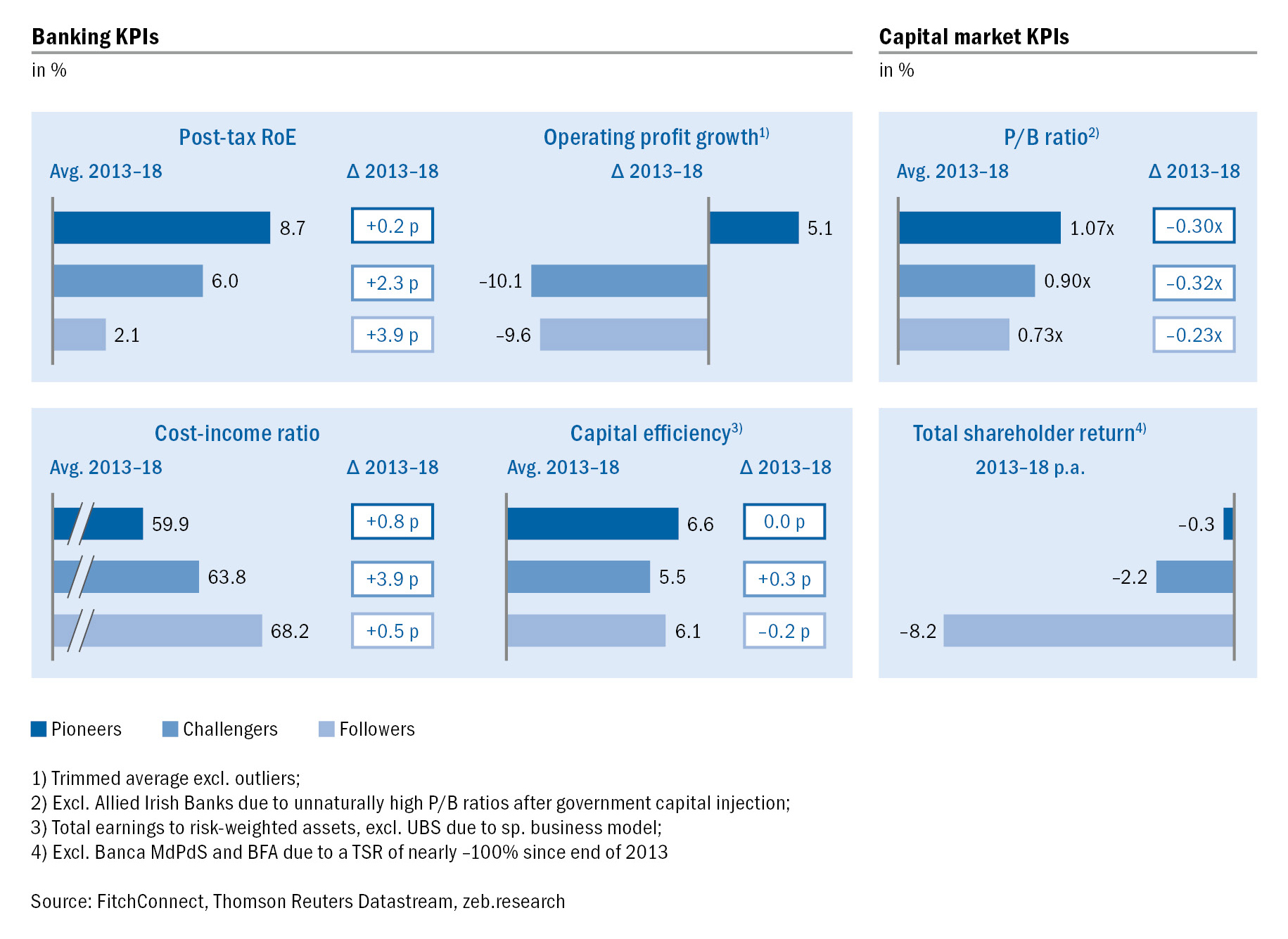

A significant—and perhaps surprising—result is that the three groups do not just differ strongly in their basic composition, but also in their performance. As it turns out, banks that are among the pioneers of digitalization within their industry outperform their less digitalized peers in terms of all significant banking and capital market KPIs (see figure 3).

Figure 3: Banking and capital market KPIs of the digital clusters

Figure 3: Banking and capital market KPIs of the digital clustersA closer investigation also shows that in their digital transformation process, the digital pioneers have clearly studied the progress and success of Big Tech companies such as Google or Amazon. In total, five key success factors can be identified:

- A consistent customer focus

- A simple, low complex, yet flexible product portfolio

- An innovation-led operating model

- An expandable infrastructure

- Omnipresence in customers’ daily life

These factors are also decisive for the success of European banks. It is obvious that the most profitable banks and digital pioneers leverage these five success factors of global Big Tech companies much better than less successful competitors. They have put their strategic focus on digitalization at an early stage, consistently implemented corresponding measures and communicated them transparently and confidently towards both the inside and the outside. These institutions are blazing a trail that shows how Europe’s banks can be successful in the future marketplace in spite of fierce competition and not only brave the storm, but turn it into a long-term competitive advantage.