Key Topics

I. State of the banking industry

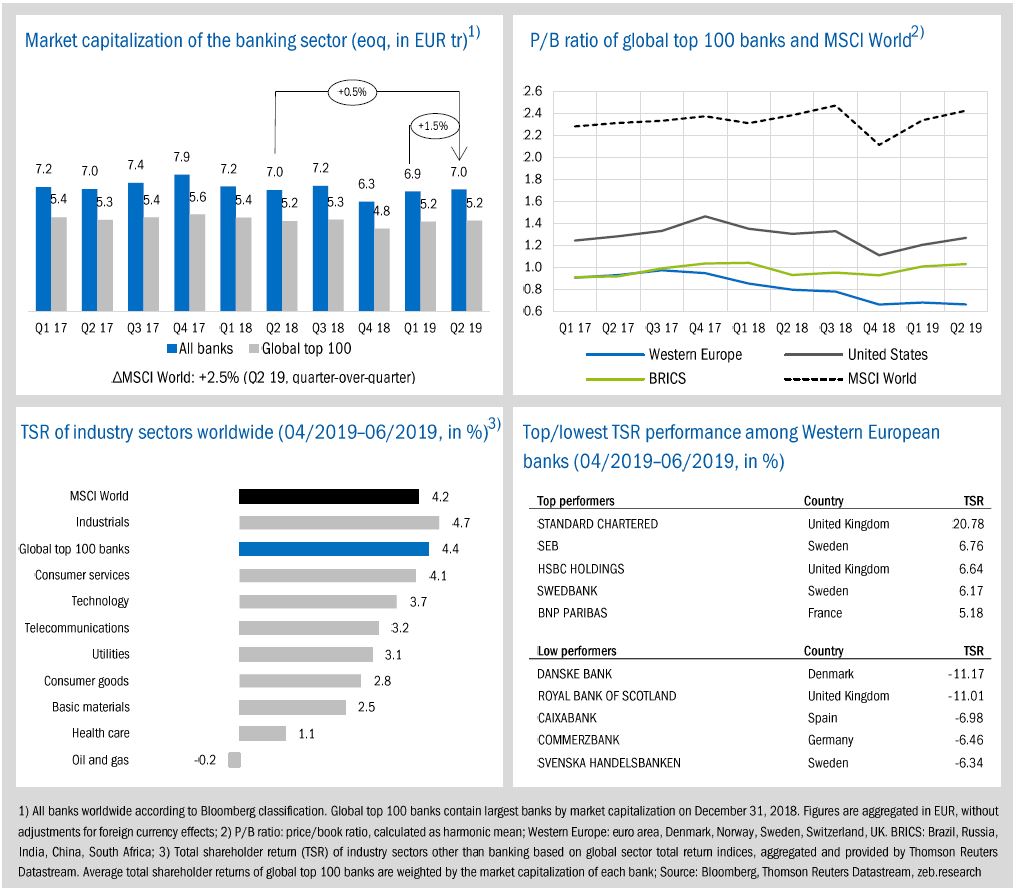

- Global top 100 banks reached the second highest TSR among all industry sectors (+4.4% qoq)—slightly better than the global market (+4.2% qoq).

- Western European banks showed, again, the lowest TSR compared to other banking regions (+0.6%). Their average P/B ratio decreased by -0.02x qoq to a rock bottom value of 0.66x.

II. Economic environment and key banking drivers

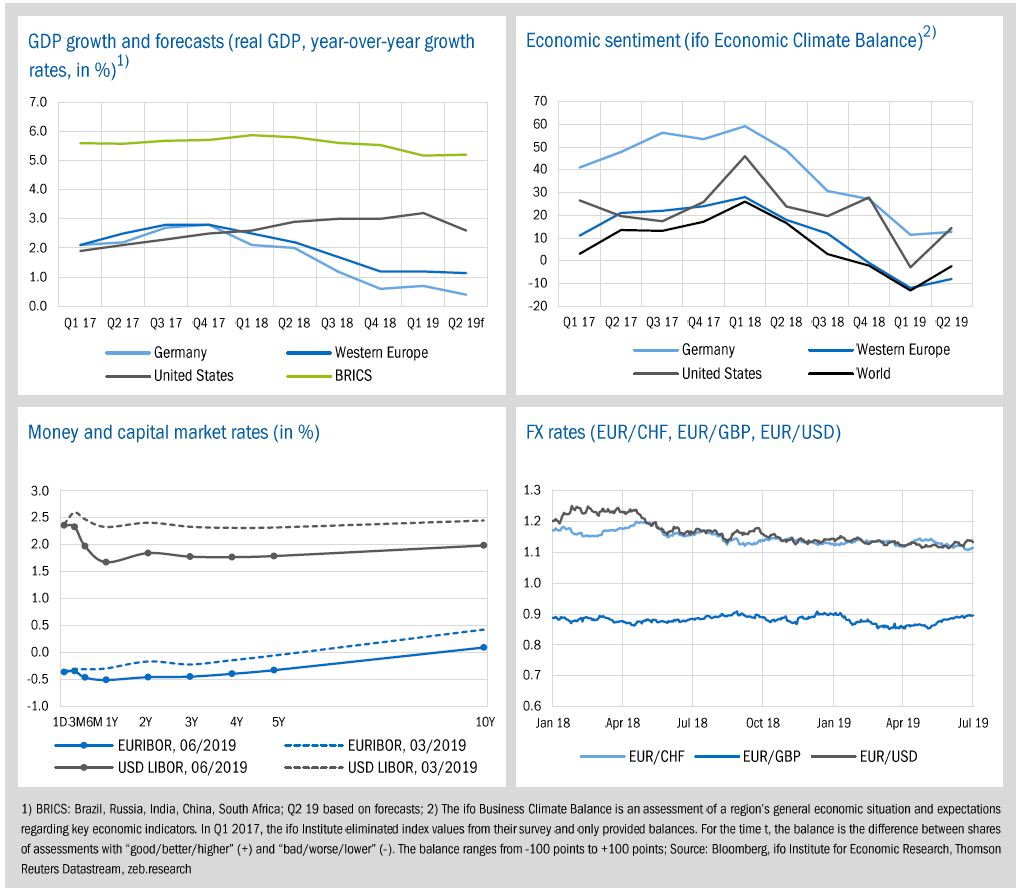

- Economic growth in Q2 is expected to slow down in nearly all considered regions in the world (U.S. -0.6pp, Germany: -0.3pp, Western Europe: -0.1pp).

- U.S. Fed as well as ECB responded to persisting economic uncertainty and lower inflation expectations with the possibility of rate cuts in 2019.

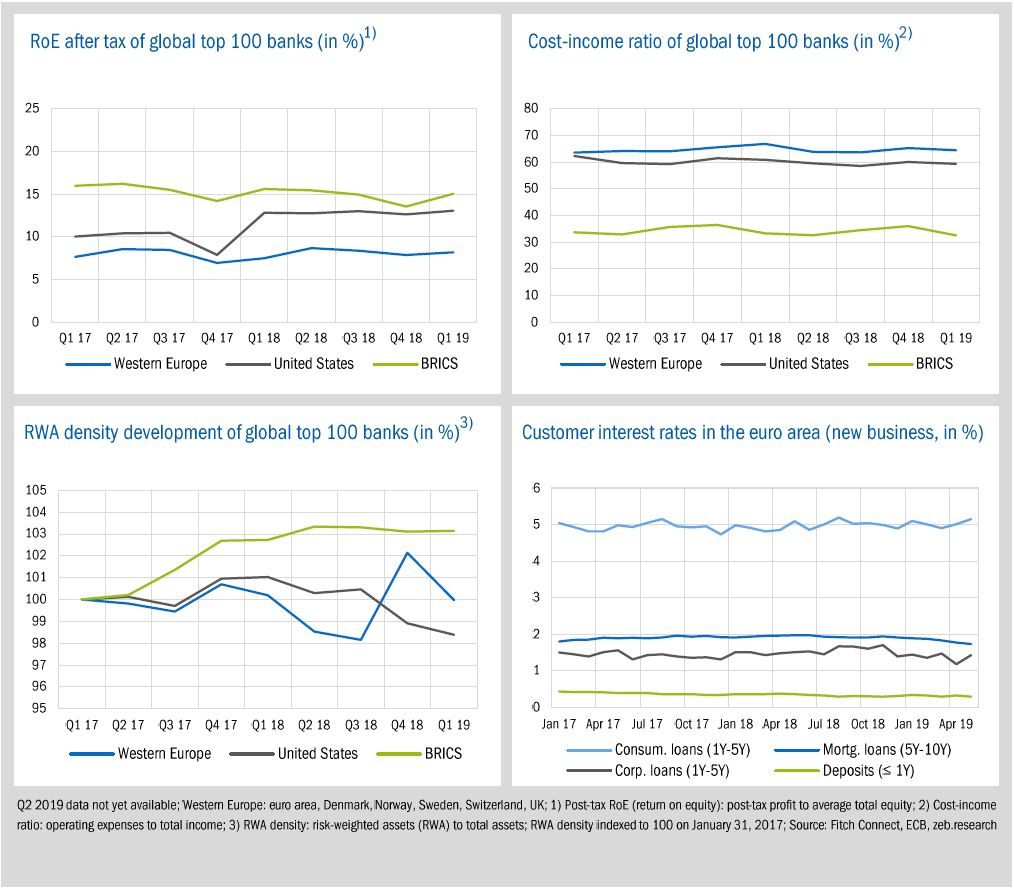

- Although average post-tax RoEs increased in Q1 across all regions (BRICS: +1.5pp qoq, U.S.: +0.4pp qoq, Europe: +0.3pp qoq), full-year RoE outlook has deteriorated due to increasing economic headwind.

III. Special topic: “TRIMming” European banks’ capital ratios

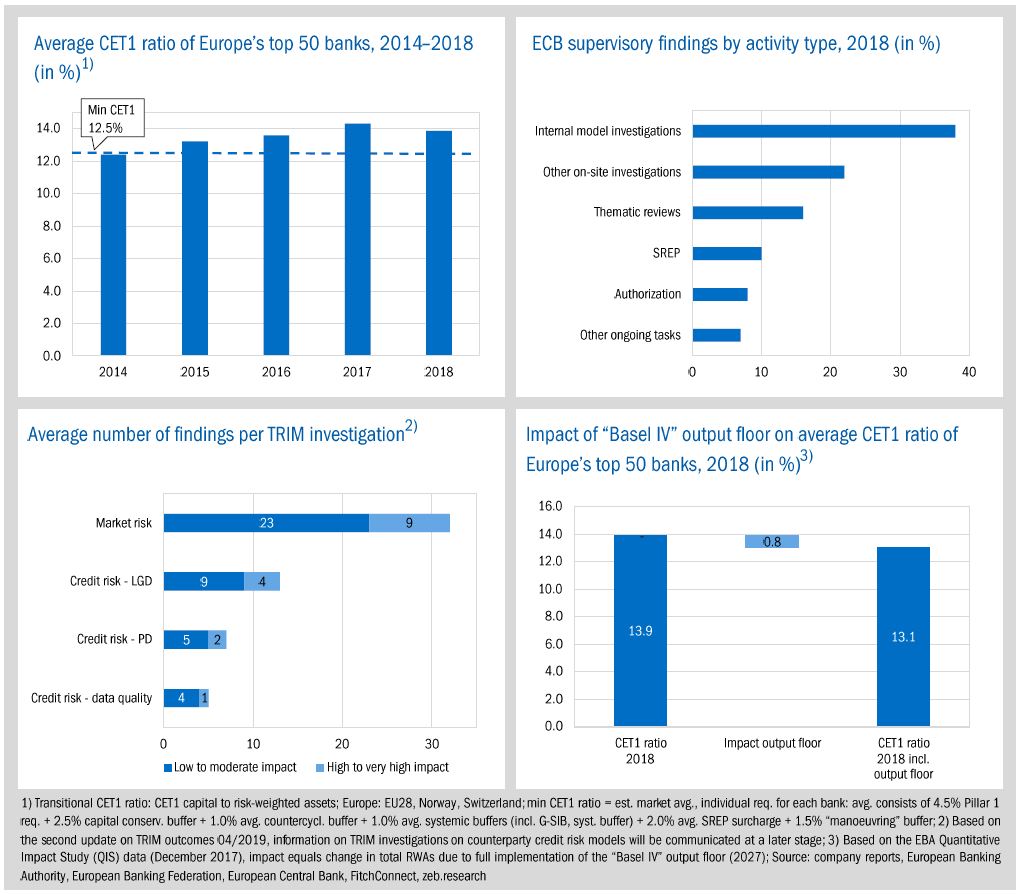

- At the beginning of April, the ECB published the project status update of its multi-year project TRIM (targeted review of internal models).

- TRIM goes hand in hand with other similar regulatory initiatives like “Basel IV” but the impacts will be noticed much earlier.

- Although bank-individual results are not published in total, additional RWA charges and therefore negative impacts on banks’ capital ratios are to be expected.

I. State of the banking industry

Capital market performance of the banking industry stabilized during the second quarter of 2019. Global top 100 banks reached the second highest TSR among all industry sectors (+4.4% qoq), slightly better than the global market (+4.2% qoq). Western European banks were, again, not able to keep up with the performance and showed the lowest TSR compared to other regions (U.S.: +6.6%, BRICS: +4.4%, Western Europe: +0.6%).

- In line with positive TSR developments, average P/B ratios of U.S. and BRICS banks improved further in Q2. U.S. banks’ average P/B ratio rose by +0.06x and BRICS banks’ P/B ratio by +0.02x. European banks, however, continue to fall behind these regions as the average P/B ratio decreased by -0.02x qoq to a value of just 0.66x—again reaching the low point of Q4 2018.

- Without considering dividend payments, market capitalization of the entire banking industry showed no considerable improvements. All banks’ market cap rose by just +1.5% qoq (MSCI World: +2.5% qoq) and reached a previous year level of EUR 7.0 tr. Global top 100 banks’ value increased by just +1.0% qoq (+0.5% yoy) and remained around the previous quarter’s market cap (EUR 5.2 tr).

- Among Western European banks, again, a Nordic bank was the lowest European TSR performer. Danske bank’s TSR decreased by -11.17%, likely influenced by the bank’s money-laundering scandal. On the contrary, UK bank Standard Chartered reached an exceptionally strong TSR performance of +20.78% due to good quarterly results as well as the announcement of a USD 1.0 bn share buyback program.

II. Economic environment and key banking drivers

In Q2 2019, economic growth is expected to slow down in nearly all considered regions in the world (U.S.: -0.6pp, Germany: -0.3pp, Western Europe: -0.1pp, BRICS: +0.0pp), in line with a still pessimistic overall economic sentiment. The U.S. Federal Reserve and the ECB responded to persisting economic uncertainty and lower inflation expectations with the possibility of a more expansive monetary policy in 2019.

- Especially for the U.S., expected GDP growth plummeted to 2.6%, mainly driven by the U.S. trade dispute with China. For Germany, private consumption has declined in Q2 and GDP growth is expected to reach a new low point.

- After four consecutive reductions, the economic climate of Western Europe and worldwide improved in Q2 but remained pessimistic (Western Europe: -8.0, World: -2.4).

- In June, the Fed decided to keep rates constant but signaled a possible 50 bp rate cut for 2019. As a result, the USD Libor curve has dropped. In the same vein, the ECB pushed possible interest rates hikes far into the future and rather discussed a possible cut or fresh bond purchases for 2019, leading to a further flattening EURIBOR curve. Except for 9 and 10-year EURIBOR rates (10y: 0.09%), yields are now negative.

- The GBP lost against the euro due to the extended Brexit deadline to October 31, 2019 and increasing uncertainty regarding a no-deal scenario. EUR/GBP rose to 0.90, the highest value since the beginning of the year.

For the first three months of the year, the average post-tax RoEs increased across all regions (BRICS banks: +1.5pp qoq, U.S. banks: +0.4pp qoq, Western European banks: +0.3pp qoq). However, RoE is by nature a lagging indicator and does not yet reflect the recent deterioration of the economic environment.

- Compared to previous year figures, only U.S. and Western European banks were able to improve their profitability in Q1 (Western European banks: +0.7pp yoy, U.S. banks: +0.2pp yoy, BRICS banks: -0.6pp yoy). Among European banks, however, the increase was mainly driven by UK banks, which reported significantly better Q1 results compared to 2018.

- In Q1 2019, average CIRs of global top 100 banks slightly decreased across all regions. On a year-over-year basis, especially Western European banks gained further efficiency (CIR Europe: -2.3pp, U.S.: -1.5pp, BRICS: -0.8pp).

- The risk density of European banks dropped significantly in the first quarter of 2019 (-2.2pp qoq), mainly driven by some Nordic banks. For example, the Norwegian bank DNB reduced their risk density by -2.5pp qoq.

- The flattening of the EURIBOR yield curve during the first months of 2019 is also reflected in the development of euro area customer rates. Compared to the beginning of the year, mortgage loan (5Y-10Y) rates decreased by -16bp and deposits by -5bp.

III. Special topic

“TRIMming” European banks’ capital ratios

At the beginning of April, the ECB published the project status update of its multi-year project TRIM (targeted review of internal models) as well as an aggregated summary of their main findings. Although bank-individual results are not published in total, first views from the market indicate a substantial impact on banks’ capital requirements. However, what changes are expected from TRIM and how are they connected to other regulatory initiatives like “Basel IV”?

European banks’ financial strength has improved significantly in recent years. Looking at Europe’s top 50 banks, the average Common Equity Tier 1 (CET1) ratio has risen steadily to 13.9% in 2018. Nevertheless, the resilience of this figure is still an important regulatory topic. One reason is the internal rating based approach (IRBA), currently used by several large European banks to calculate their risk weighted assets (RWA) and to determine their own capital needs. Although approved by national supervisory authorities, regulatory requirements for internal models are interpreted differently across European countries as well as over time and banks have certain degrees of freedom in order to design their own modelling approaches. Depending on national interpretation of IRBA requirements as well as the age of the models in use, significant differences in risk assessments across European banks are observable and therefore an inadequate capital backing of these risks is conceivable.

As a result, IRBA models have gained more and more of a supervisory focus. Since 2016, under the title “Future of the IRB Approach”, the European Banking Authority has successively published various guidelines to ensure a robust and clear IRBA framework, which will become binding from 2022 onwards. Also in 2016, the Basel Committee on Banking Supervision started similar efforts which ultimately ended in parts in the so called “Basel IV” rules which will also be effective from 2022. Predominantly banks with previous IRBA approvals might have a significant gap between formerly best practice and today’s regulatory understanding.

Last but not least, the ECB started the TRIM project in order to reduce the potential non-risk-based variabilities and inconsistencies in RWA calculations across significant institutions in the Single Supervisory Mechanism. Based on ECB’s latest annual report on supervisory activity, 38% of all ECB supervisory findings in 2018 have been originated from internal model investigations—most of them due to the TRIM project. In April 2019, the ECB provided an overview of the most common or critical shortcomings that were identified during TRIM. For instance, 80 credit risk investigations have taken place so far and led to on average 13 (4 severe) findings per investigation regarding the loss given default (LGD) parameter, 7 regarding the probability of default (PD) parameter and 5 concerning data quality. Many of these findings also address fundamental aspects of the EBA guidelines described above. However, the ECB argues that these guidelines only refine the existing capital requirements regulation and must therefore already be complied with in principle today.

TRIM is expected to be formally concluded in the first half of 2020. However, ECB’s critical examination of the internal models will probably continue beyond that date. Banks supervised by the ECB should keep in mind the validation reporting on internal models for credit risk which have to be submitted as of October 2019. Based on this specified procedure, the ECB will be able to identify anomalies in a European comparison and to proceed TRIM activities under the cloak of general internal model investigations. A similar procedure is already conducted by the EBA Benchmarking Excercise published in January 2019, which provides an industry-wide comparison of IRBA institutions and allows the regulator to precisely examine conspicuous banks and models.

Although audited banks are currently still quite hesitant regarding their individual TRIM impact, surcharges on banks’ RWAs and therefore negative impacts on banks’ capital ratios are to be expected. On the one hand, the elimination of the identified shortcomings will have a direct and immediate effect on banks’ RWAs. On the other hand, general surcharges on banks’ capital requirements from individual decision letters and following internal model investigations as well as the requirements from the annual SREP will result explicitly in additional and higher capital needs.

Overall, the outcome of the TRIM project will reduce the previous advantage of using internal models. This effect was actually expected with the introduction of the “Basel IV” output floor, which limits the amount of capital benefits banks can obtain by using internal approaches. As an indication, based on first assessments from the EBA, the effect of the full implementation of this output floor would lead to an additional charge on total RWAs for European banks of 6.3%.[1] However, the full implementation of the floor is scheduled for 2027 and is now strongly brought forward in time by TRIM. Compared to 2018 figures for Europe’s top 50 banks, this would be equivalent to an 82bp drop in the average CET1 ratio. Moreover, additional RWA charges will not only affect banks’ capital requirements, but could also significantly reduce the profitability of certain asset classes: an impact that is likely to be relevant for all IRBA institutions.

European banks using IRBA are therefore well advised to consistently work on their models and to adjust them regarding the “Future of the IRB Approach” guidelines. A timely alignment with these guidelines as well as TRIM requirements is needed to identify gaps and to derive tangible measures. Merging and prioritizing the measures in a TRIM roadmap will guide them through the process in order to avoid general capital surcharges or to get rid of them quickly. Finally, banks have to push ahead with the execution of strategic implications of “Basel IV”—like strategic capital/ asset allocation or adjusted pricing apporaches—as higher RWA burdens occur much earlier than expected.