The future starts today

In retail customer business, both consumer and mortgage loans will mainly be taken out online and processed by banks on a fully automated basis in the near future. An example for a scenario which can already be technically and legally realized in 2018 is that customers can choose the most favorable consumer financing option for e.g. a 3D printer while still in the store using their smartphone and a comparison platform and will have the funds available in their current account within minutes. Keeping customers’ current accounts or hoping that loans are processed through the main bank will therefore no longer be an advantage for banks. Even in real estate financing, binding loan approvals will be possible within only a few minutes—although this development will still take several years due to the market readiness of artificial intelligence. It is true that personal advisory services will continue to be requested by some retail customers. In contrast to today’s common practice, personal advice will become optional in the lending process and will be provided after the automated lending offers. In the more complex business and corporate customer segment, we will not see a fully automated loan approval process in the near future. Most of the currently still manual process steps will, however, be gradually automated and will thus limit the scope of human decisions. A particular challenge will be the combination of automated and manual process models in an intelligent work flow and along a continuous data flow to fully ensure processing speed and efficiency on the one hand and flexibility and personal advisory services on the other hand.

The authors are convinced that, to remain competitive, banks need to start with a comprehensive redesign of the entire end-to-end lending process even today. Some market players like SWK Bank in Germany or cashpresso in Austria already offer consumer financing for new customers exclusively online and on an almost fully automated basis. Corresponding market entries will increase and rapidly expand to more complex loan products.

Between the poles of technical possibilities and legal requirements

To respond to these challenges, a revolution of the lending process is necessary, which requires complete digitalization and comprehensive automation. Digital channels fulfill the customers’ need for convenience and continuous availability. At the same time, they offer banks new opportunities for growth. Paperless digital processes allow for efficient processing and thus also make competitive prices possible. Automated processing is possible wherever individual process steps or entire process chains can be standardized. However, the entire lending business also continues to be highly regulated and is subject to numerous legal and regulatory requirements. Interestingly, the partly revolutionary new technical possibilities also provide impetus to expand or adjust this legal framework.

Complete digitalization

A core legal requirement is the analysis of the customer’s credit scoring and debt servicing capability that the bank is required to perform based on sufficient data. As part of the analysis, all information and data on customer creditworthiness (e.g. income or annual financial statements) as well as on relevant collateral (real estate, securities accounts, sureties, etc.) need to be captured. For a long time, scans and partially OCR technologies (optical character recognition) that digitalize paper-based documents were used for digitalization. In this context, problems arose from the high error rate of text recognition and the fact that only previously defined document structures could be interpreted. Two major developments can be observed here. The preferred option is direct digital recording of relevant information using uniform data standards. For private customers, XS2A (access to the account) based on the EU regulation PSD II (Payment Service Directive II) can be applied. This regulation will enter into force in 2018 and envisages for example that a bank customer can grant read access to their current account to a third-party provider (e.g. another bank). Even today, similar solutions via web scraping or country-specific standards (e.g. HBCI FinTS in Germany) have been successfully implemented. Besides customer master data, the third-party provider receives transaction data that include the customer’s income, housing costs and existing loan repayments if applicable. Based on the electronic data, the customer’s creditworthiness and debt servicing capability are reliably and to a large extent automatically determined. For corporate customers, the international xBRL standard (extended business reporting language) can be used to electronically submit annual financial statements (balance sheet, P&L, revenue and expenditure calculation, annexes, etc.). Although this standard has been mandatory in Germany for reporting to fiscal authorities since 2011, it has been hardly used by banks. An initiative is currently piloting the “digital financial report”, which is specifically intended for credit rating by banks. Its comprehensive implementation is planned for 2018. Besides direct electronic data recording it will always be necessary to retrieve data from unstructured documents, e.g. deed registrations, insurance policies, construction plans and sureties. This is a possible use case for artificial intelligence which is able to also interpret such documents after a training period and convert them into structured data. Beyond this, artificial intelligence can be used for the legally required check of disbursement prerequisites (e.g. documentation of building progress).

Customer authentication and signatures on contracts and certificates present another obstacle for digitalization. On the one hand, local anti-money laundering regulations require a mandatory identity check of new customers. On the other hand, formal requirements for written loan agreements must be considered. For example, loan agreements with private customers in Germany generally require written form. For standardized consumer loans, however, special regulations may be applied. For sureties and charges on property, however, the written form is required for business and corporate customers without exception.

A solution is provided by qualified electronic signatures that clearly document both the identity of the signatory and their declaration of intent and that have the same legal status as handwritten signatures. Aside from a reliable local certification authority, for a long time qualified electronic signatures required physical signature cards and the respective readers (e.g. D-Trust) which could never be broadly established in private customer business. The EU regulation eIDAS (electronic identification, authentication and trust service) set out the legal framework across Europe for e.g. remote signatures (“cell phone signatures”) in July 2016. It is sufficient if the signatory’s certificate is centrally stored on the server of the certification authority. A smartphone is thus a suitable end device for the customer, which helps achieve a significantly higher market penetration. Remote signatures are already used as part of video ident processes. In this process, the bank directs the customer to a provider (e.g. IDnow, webID) for authentication through video ident. A certificate for the customer is then centrally stored and used for example to provide a qualified signature for a loan contract. This process has the advantage that there are no prerequisites for the customer except for a smartphone and a photo ID. The legal framework for video ident was only implemented in Austria at the end of 2016—long after the technology had already been established across Germany. Moreover, universally usable remote signatures are available (e.g. A-Trust) for which, however, personal authentication is still generally required. The eiDAS regulation also enabled electronic seals for legal entities. This gives companies the opportunity to include a uniform organizational signature in their outgoing digital correspondence which can replace traditional company stamps. Solutions for business and corporate customers are still based on a physical signature card (e.g. Secrypt, D-TRUST, A-Trust).

Finally, digitalization will be also introduced for physical inspections of collateral. Such inspections are particularly important for property as written documentation is usually insufficient here. Such inspections are currently performed by the bank or external surveyor. The current technical progress, however, will soon allow such inspections to be made by drones, which can reach the respective property in a very short time and document its state or building process. Equipping drones with special sensors would also make it possible to inspect the inside of the property, measure the size of rooms precisely or identify construction defects or damage (e.g. caused by water or mold). Besides general legal aspects such as data or privacy protection, legal issues related to loans remain to be solved. For example, interior inspections are still required for the eligibility of loans for covered bonds. Suitable drone technology could however provide similar analysis results just as well. The recorded data would then be submitted either to the bank or the surveyor and present the digital data basis for appraisals or building progress checks.

Far-reaching automation

Automation in the lending process is linked to two prerequisites. First, all relevant information must be available as electronic and structured data. Second, automation requires comprehensive standardization at least in the medium term—either of single steps and process modules or of the whole lending process. It is obvious that different variations will be possible, particularly regarding the potential for standardization, which will depend on the individual loan product (e.g. consumer loan vs. construction loan) as well as on the customer segment (e.g. private vs. corporate customers). Automation can include different decisions in the lending process and the necessary checks.

The fundamental decision if a loan is granted as well as the amount and terms play a crucial role in the lending process. Exclusion criteria, the creditworthiness and debt servicing capability of the customer (or of the group of associated customers) as well as the value of collateral are essential factors for decision making. All of these decision criteria can in principle be standardized and also automated (provided that digital recording is available). Regulations currently require banks to double check loan decisions as a basic principle while these checks can also be performed electronically in non-risk-relevant or standardized private customer business. In this segment, decision-making engines are already in use which however still need to be manually checked and, if needed, recalibrated by risk experts at more or less regular intervals. The complexity in corporate customer business is significantly higher due to more difficult customer creditworthiness checks and the wide variety of collateral. Completely automated decision-making engines are therefore not yet implemented in this business segment. Artificial, self-learning intelligence will gradually replace human discretionary decisions in the future. Based on historical data (e.g. loan defaults, payment delays or fraud), artificial intelligence systems will continuously adjust their decision-making algorithms to changing market conditions (e.g. economic growth, income levels, real estate prices) and thus improve the quality of decisions made. Artificial intelligence is able to assess significantly more criteria and to flexibly weight them than common rigid decision-making engines. Advantages include both the quality and transparency of loan decisions as well as the processing speed and efficiency. Here as well, new technical possibilities will drive the creation of the legal framework and force back the double-checking principle step by step. The standardization of processing steps and process modules still required today will also decrease with improving performance of artificial intelligence. However, human decisions will not be completely replaced in the medium term. For liability reasons alone, management boards of banks should make sure to check cases with high damage potential (large exposure and/or uncertain creditworthiness) themselves—even if a reliable recommendation has been provided by artificial intelligence. The same applies for the different checks in the lending process: Regulations require checking if all prerequisites or terms are fulfilled in the loan contract before disbursement. If all relevant information is available in electronic and structured form, such checks can also be performed automatically. Artificial intelligence will sometimes sort out cases for manual reviews if indications for e.g. fraud are detected or a considerably high damage potential is identified.

Conclusion

The technological possibilities described will fundamentally alter the way in which loans are granted, both in customer perception and in terms of the internal bank processes and organization. zeb advises all banks to face the revolution in the lending process as soon as possible in order to avoid losing competitive strength in the years ahead.

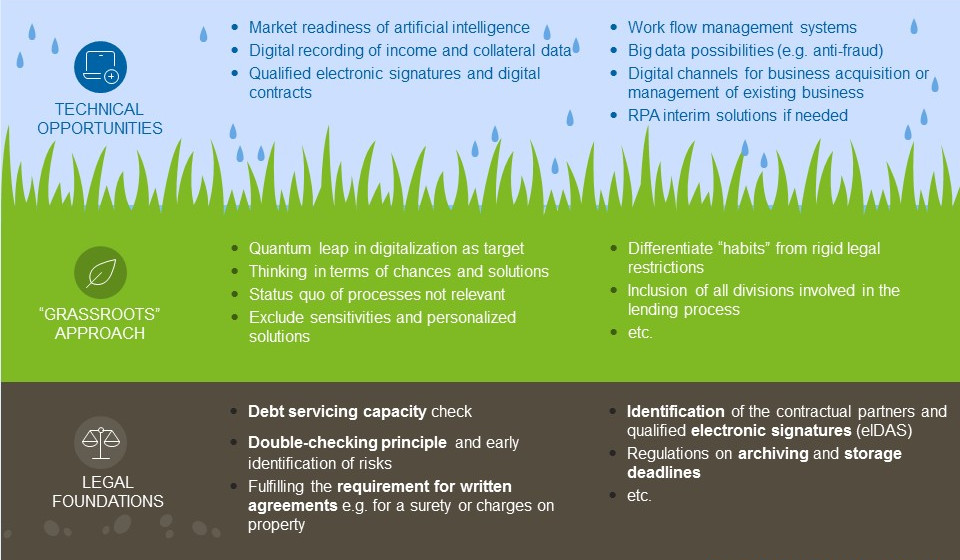

Figure 1: Grassroots redesign

Figure 1: Grassroots redesignThe evolutionary development of individual elements of the lending process is no longer sufficient. The lending process of the future has to be fundamentally reviewed and redesigned from the grassroots. In doing so, revolutionary technical possibilities as well as current and possible future legal foundations need to be integrated.

One response to “The future starts today: digital revolution in the lending process”

RAMA KUMAR

Need Regular updates