EBA defines uniform methodological requirements for the IRB approach

EBA recently finalized the third phase of the initiative dealing with the requirements for risk parameter estimation. While the new definition of default (Phase 2) will have to be applied from January 1, 2021, EBA recently postponed the deadline for implementing the methodological requirements from Phase 3 by one year to January 1, 2022.[1]

Apart from the guidelines for PD/LGD estimation, which were finalized at the end of 2017, the discussion in Phase 3 was in particular focused on the requirements for determining downturn parameters.

The reason for this is that institutions are currently taking economic downturns into account inconsistently in the LGD and CCF models and are often unable to explain in a transparent manner how downturns are identified and how their impact on the risk parameters is quantified. Since the downturn LGD has a direct proportional effect on the Risk Weighted Assets (RWA) in credit risk, the quantification procedures are strong levers with regard to the institutions’ capital requirements.[2]

After two consultation phases, draft regulatory requirements have been finalized in March this year (2 years after the first consultation). This gives reason to analyze the final RTS and Guidelines (GL) in more detail to show changes compared to the last consultation phase and to highlight the main challenges for institutions.[3]

Substantial changes compared to the second consultation

1. Specifying the influence of LGD components on the downturn LGD

In the final version of the GL, EBA specifies how downturn effects on LGD components (e.g. recovery cash flows, recovery rates and loss durations) are to be taken into account when quantifying the down-turn LGD. The LGD effects of the components affected by the downturn are to be aggregated to form the downturn LGD. The LGD component with the most severe value compared to its long-term average is the starting point. Other components must also be taken into account if they continue to drive the (aggregated) downturn LGD—but not necessarily beyond the LGD level observed during the downturn.

2. Simplification with LGD in-default and irrelevant downturn LGDs

Regarding LGD in-default, EBA made some concessions to the institutions in terms of scope and complexity of the requirements. According to the final version of the GL, the quantification of the downturn adjustments for both the LGD non-defaulted and the LGD in-default should now be based on the same downturn period. Furthermore, an individual downturn adjustment does not necessarily have to be calculated for each reference date relevant for the LGD in-default as long as evidence is provided that this simplified procedure tends to be conservative.[4]

In addition, irrelevant downturn LGD calculations according to the final GL can now be omitted. If several downturn periods have been identified for a calibration segment, institutions are now allowed to take a shortcut. If it can be reasonably demonstrated that certain economic factors are not relevant for further downturn analysis (e.g. if a factor refers to an industry that is not relevant for the calibration segment), no downturn LGD needs to be determined or estimated for the non-relevant factors.

3. Obligation to adopt the haircut approach and extended application of the extrapolation approach

In the final GL, EBA has implemented a further prioritization of the approaches to downturn LGD estimation. Within the so-called Type 2 approaches, the haircut approach now becomes mandatory if a relevant cyclical risk driver is present in the model.[5] EBA justifies this change with the insight that high estimation uncertainties in the extrapolation approach may lead to insufficiently conservative results.

In order to keep the application of the Type 3 approaches low, which are comparatively disadvantageous for institutions, the EBA has also extended the scope of the extrapolation approach.

The precise classification of the approaches and methods mentioned here as well as a general explanation of the procedure model for determining the downturn components are subject to the following chapter.

Determination of downturn LGD on the basis of a structured process model

Overview of the process model

LGD estimates (and also CCF estimates) should reflect the conditions of economic downturns. Institutions have interpreted and methodically implemented this requirement in different ways. When read in context, the final RTS and GL provide clarification on the process of parameter estimation. A possible procedure for estimating the downturn parameters is shown in Figure 1.

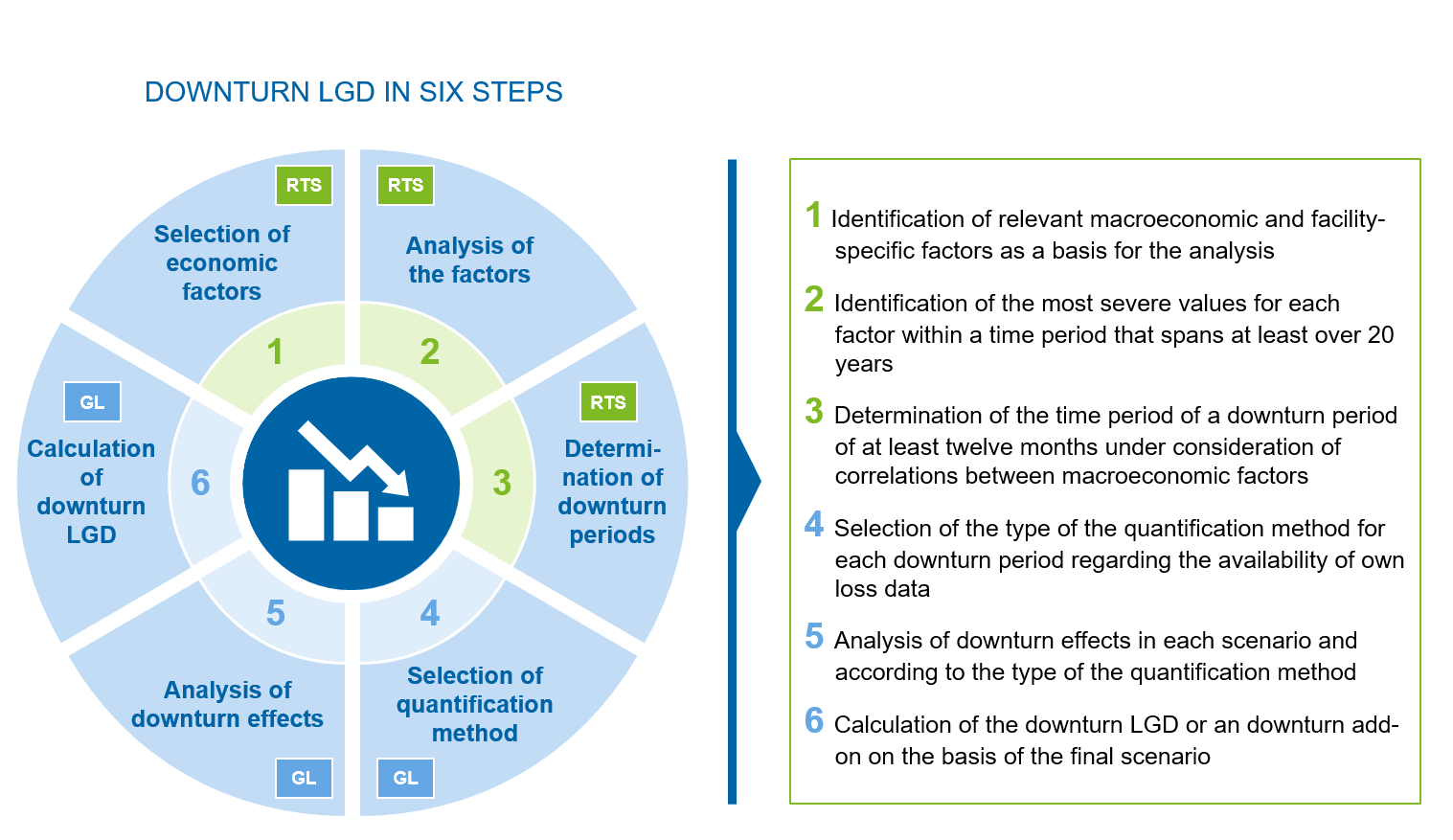

Figure 1: Overview of the procedure for determining downturn LGD

Figure 1: Overview of the procedure for determining downturn LGDIdentification of downturn periods according to RTS (steps 1–3)

The procedure set out in the RTS serves to identify downturn periods in the sense of relevant time windows, which are then used to quantify the downturn LGD on the institution’s own loss data (see the next subsection on steps 4-6).

Downturn periods are identified on the basis of a catalog of economic factors specified by EBA, which must be supplemented individually by region-specific or exposure class-specific indicators. The factors must be examined for each relevant jurisdiction and, if necessary, adjusted for regional or sector-specific influences. Depending on the economic logic, the absolute level or relative change of the factors, or both, should be taken into account.

A downturn period is defined as the twelve-month period where at least one economic factor shows its most severe realization. For each factor, a 20-year time series should be used, which should be extended if no clearly discernible downturn can be identified. The duration of a downturn period may be more than twelve months if a relevant factor remains at a weak level for a longer period. Adjacent downturn periods may be merged if this can be economically justified, e.g. in the sense of a coherent economic cycle.

Quantifying downturn LGD according to Guidelines (steps 4–6)

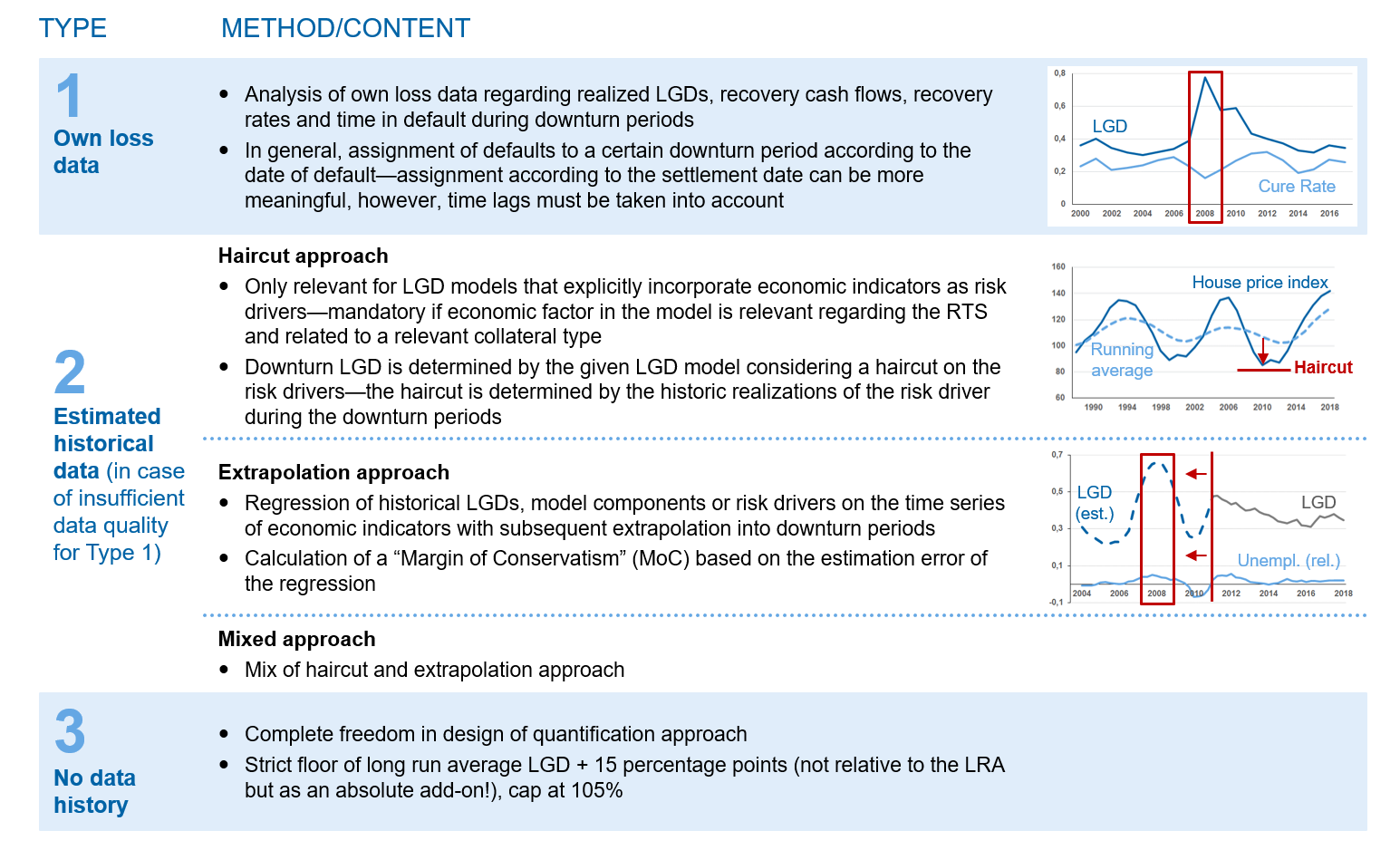

For the identified downturn periods, the loss data of the institution must be analyzed for the relevant pool of exposures and jurisdiction.[6] Since not every institution has extensive data histories on hand, EBA defines a set of differently prioritized alternative quantification approaches for the corresponding downturn periods, depending on data availability. They are briefly characterized in the figure below.

Figure 2: Prioritized quantification approaches for the downturn LGD

Figure 2: Prioritized quantification approaches for the downturn LGDAll approaches that completely rely on an institution’s own data history are prioritized (Type 1). In addition to the realized LGDs, annual recoveries, cure rates and the time in default must also be analyzed.

If no or only a limited amount of loss data is available for a specific downturn period, approaches can be used that estimate historical loss data (Type 2). If an LGD model contains an economic factor as a risk driver, a haircut must be derived according to the factor’s realization during the downturn period (so-called haircut approach). Alternatively, LGDs or LGD model components can be extrapolated using regression analyses (so-called extrapolation approach). With this approach, however, an additional Margin of Conservatism (MoC) is required.

Only if no relevant downturn period can be analyzed according to the approaches mentioned, may a fallback solution be applied, where the institution may use procedures that are not based on own loss data (Type 3). In this case, a strict LGD floor of 15 percentage points applies to the long-run average LGD.

As a result of the downturn estimation, each calibration segment receives an “add-on” that is added to the long-run average LGD and leads to an LGD that is appropriate for an economic downturn or a calibration target to which the LGD can be directly calibrated.[7]

The final add-on or calibration target to be used is the one that leads to the most conservative LGD estimates. If the downturn period of an individual downturn scenario can only be valued using Type 2 or 3 methods, this uncertainty must be taken into account in the downturn LGD via an additional MoC. It generally holds that the lower the priority of an approach, the stronger the requirements regarding MoC.

The GL’s detailed requirements create complexity—essential challenges have to be mastered

While the RTS has been considerably simplified compared to its first consultation, the guidelines still contain complex detailed requirements and scope for interpretation. Challenges arise from the following aspects, among others:

- The concrete mathematical derivation of the downturn LGD remains an open question, although the analytic approaches, as described above, are clearly outlined. In addition, the design of an add-on (multiplicative, additive, caps, floors, etc.) remains unclear if a different way than a calibration target is applied. The guidelines merely stipulate that the downturn adjustment should not change the assignment of exposures to facility grades or pools.

- In order to reduce the cyclicality of the models, the amount of the downturn effect should be chosen sensitive to the current economic cycle. For example, a smaller add-on could be taken into account in acute downturns. However, the methodological derivation of such an economic dependence in the models remains unclear.

- In order to take into account the downturn effects of LGD components, institutions must develop methods by means of which the effects of the individual components can be aggregated into a downturn LGD. This is a difficult undertaking given the dependencies of the individual components. The two principles presented by EBA for this aggregation provide only little guidance.

- EBA requires the calculation of a reference value for the downturn LGD to check the plausibility of the institution’s results. Therefore, it is advisable to provide appropriate reconciliations from the reference value to the actual downturn LGD in preparation for audits.

- According to the Guidelines, the downturn periods that can only be quantified using Type 3 methods are negligible if there are other downturn periods that can be quantified with the institution’s own or estimated history (Type 1 or Type 2 approaches). The estimation uncertainty due to non-considering the Type 3 periods is to be taken into account via a MoC. How this MoC can be calculated without a data basis remains unclear.

At the level of the individual quantification approaches, uncertainty and practical challenges remain, too:

- In the extrapolation approach, LGDs or model components should be estimated by several economic factors. However, since economic factors are often strongly correlated this will lead to multicollinear models, i.e. overfitting. On the other hand, a reduced model would suffer from a lack of explanatory content.

- When applying the haircut approach, it should be noted that usually only a few or only one single component of the LGD model directly depends on macroeconomic factors. However, since a downturn can affect all model components, the haircut approach will have to be applied on a regular basis in combination with the extrapolation approach, thus providing little relief in terms of methodology and data.

- In the case of Type 3 approaches, the flatrate floor of 15% for certain asset classes, in which overcollateralization can typically be observed, may simply be too conservative and lead to risk-insensitive management.

- Type 2 approaches are probably the most challenging alternative with regard to the complexity of the methods. At the same time, the relevance of the Type 2 approaches is high, especially at the start of their application in 2022 due to the mostly short loss data histories in the institutions. The challenge in this respect is that various macroeconomic factors, e.g. the unemployment rate, will show their worst realization outside quality-assured internal loss histories within the required 20-year history.

Assessment and outlook

In the course of the two years since the first consultation, EBA has proceeded to reform the requirements for deriving the downturn LGD and to take into account the availability of data in the institutions as well as the complexity of the calculations, at least partially. All in all, downturn estimation as a “discipline” in parameter estimation is more and more focused on.

The final requirements show only moderate improvements compared to the second consultation. Although some problem areas were addressed (e.g. LGD in-default and LGD component aggregation), a number of severe challenges remain in the final version. Overall, it is to be noted that the requirements imply an enormous need for action for most institutions. Considering the immense amount of analyses required for the downturn parameter estimation, the implementation of the requirements—despite the postponement until 2022—remains an ambitious goal. This is aggravated by the necessity to implement the highly detailed provisions of the guideline for PD/LGD estimates in parallel. The institutions should therefore begin preparations and implementation as soon as possible if they have not already done so.

zeb already supports customer projects, among other things, in the conceptual design of methods, in the collection and consolidation of relevant loss and macroeconomic time series and in forecasting the RWA impact on the basis of currently available data.