Digitalization is the key driver for changing marketing and sales processes in banks

At the same time, however, the classic channels will not be completely replaced. 61% of all bank product sales preceded by online research are still generated through traditional channels such as branches. Rather, an efficient and seamless interconnection of both worlds—the digital and classic channels—will be decisive for offering customers needs-based advice in the future as well.

An omnichannel strategy as the key pillar of strategy

That the financial industry is making such active efforts to implement an omnichannel strategy is a reflection of this development. Providing customers with the opportunity to “travel” on their preferred channel—deviate from it if necessary and return at a later point in time—is the target image to which financial institutions are moving and must move.

The flexible use of contact points along digital and classic interfaces leads to a rapid accumulation of valuable information about customer behavior and needs. Banks must use this information systematically to identify customer needs at an early stage and address them individually. At present, however, the majority of banks fail to adequately tap the potentials offered by the omnichannel strategy.

Other sectors, the most prominent example being the retail sector, are leading the way. Consistent customer information and the ability to conclude contracts on all channels lead to higher market penetration and, by making products easily accessible, move them closer to everyday customer life.

Systematic integration of classic and digital marketing and sales processes as the basis for a successful omnichannel strategy

The consistent implementation of digital marketing and sales processes is necessary to monetize omnichannel models. Valuable customer contacts that signal interest in certain banking products and services online (so-called “leads”) must be systematically transformed into potential customers, regardless of their choice of the trade channel (classic or online).

According to the results of a recent zeb study, only a quarter of the institutions pursue a targeted online marketing strategy. Most banks are limited to their own corporate website without systematically processing these leads. External sources—including social media such as Facebook—are hardly being used for marketing measures. Only 5% of the banks surveyed carry out personalized marketing.

Therefore, implementing the strategy not only requires banks to integrate classic and digital channels, but also to expand existing contact points along the customer journey.

Challenges for the marketing and sales process in banks

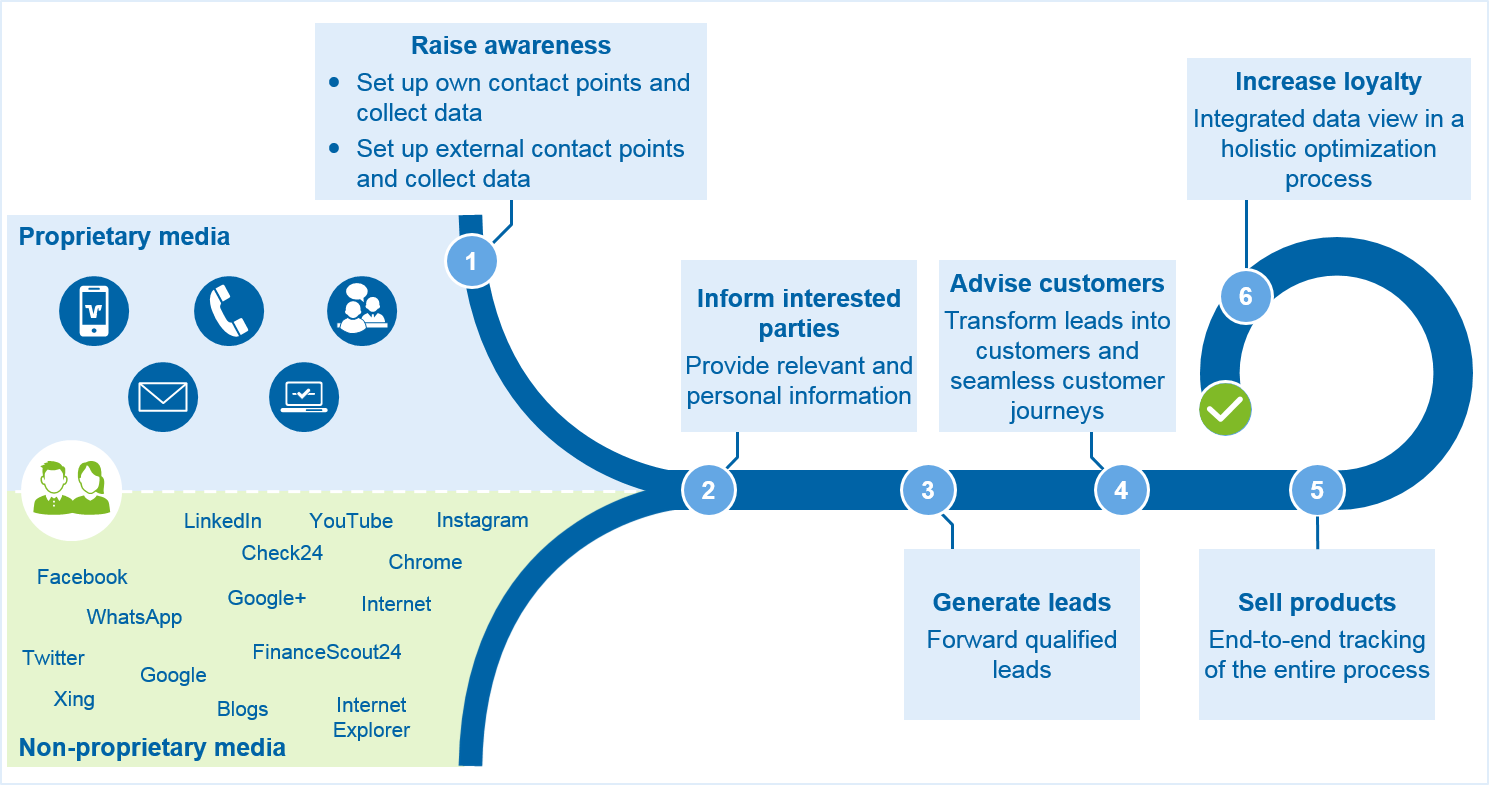

The customers’ changed channel and media usage behavior leads to various challenges for the marketing and sales process in banks. In-house (“proprietary”) and external (“non-proprietary”) media form the new “entry point” to the funnel, in which the the boundaries between marketing and sales are blurred. Despite increasing data diversity and the diversity of customer types, banks must systematically establish a presence in the digital world and create sustainable and recurring contact points with potential customers.

Figure 1: Overview of the challenges for banks throughout the marketing and sales process

Figure 1: Overview of the challenges for banks throughout the marketing and sales processOnce 1) entry into the funnel has been achieved, the bank should 2) provide targeted information and 3) offer tailored solutions as well as 4) advice in the most suitable sales channel. 5) The sale of products and services must solve problems and fulfill desires. Only then, in combination with value-creating additional products and services, can banks 6) sustainably ensure customer satisfaction, loyalty and referral rates.

Targeted digital marketing and sales must assume the task of guiding the customer through the financial institution’s world of products and services on all channels of their customer journey—from information to conclusion. The right information at the right time via the right sales channel—this is the key to growth and success in the omnichannel model.

Levers of modern, digital marketing and sales management

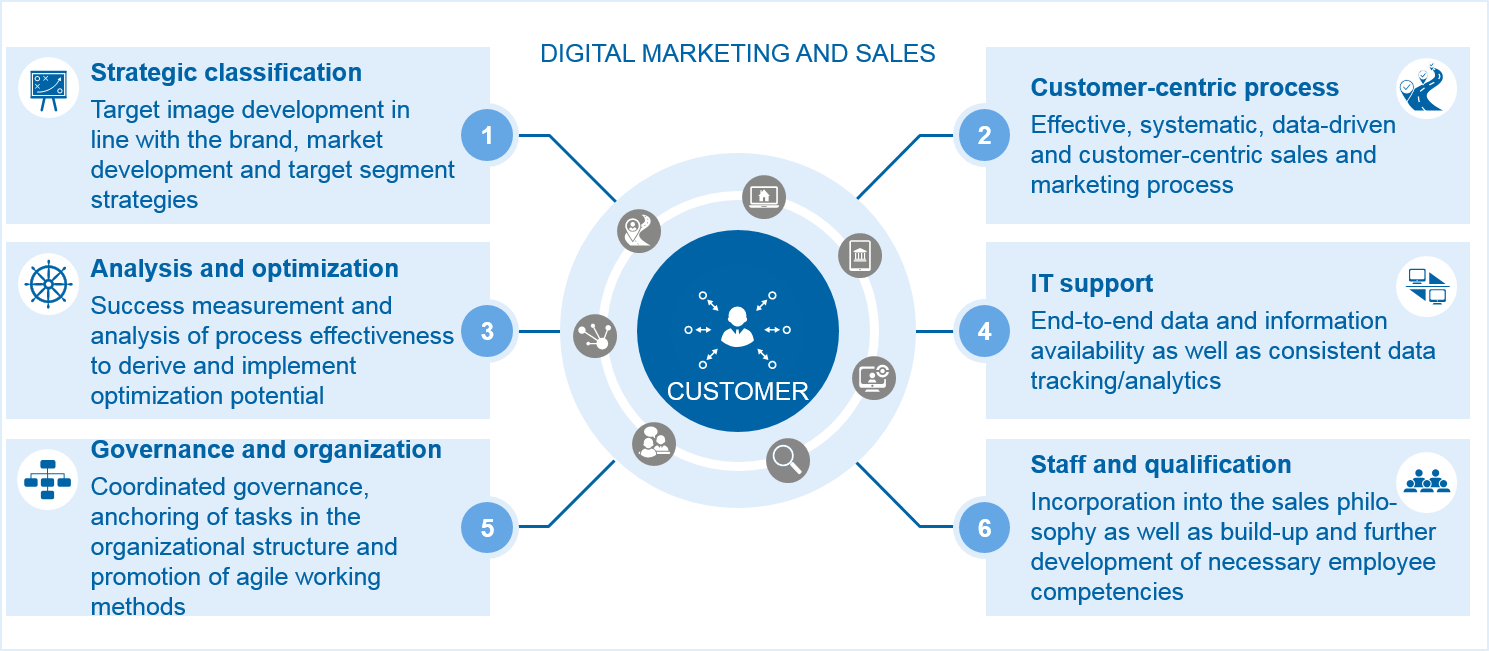

In order to ensure successful digital marketing and sales, the institution needs to design six elements:

- Within the framework of a strategic classification, the target image for digital marketing and sales is developed in line with the brand, market development and target segment strategies

- A customer-centric and integrated process is the basic prerequisite for successful implementation

- Analysis and optimization along a defined process ensure the continuous derivation and implementation of optimization potentials

- End-to-end data availability and systematic data tracking via corresponding tracking tools are the focus of IT support for digital marketing and sales

- Governance and organization support through targeted anchoring of tasks, overarching cooperation formats and promotion of agile working methods

- A digital “sales philosophy” and the necessary competencies are sustainably developed and maintained within the framework of staff and qualification

Figure 2: Elements for digital marketing and sales

Figure 2: Elements for digital marketing and salesContinuous analysis and a systematic optimization process to ensure successful implementation

In order to successfully implement digital marketing and sales, it is crucial to systematically evaluate the data collected along the customer journey, identify potential for improvement and initiate continuous optimization. By analyzing customer flows on the website, it is possible, for example, to identify improvement potential in its structure, layout and content and significantly increase conversion rates even through minor adjustments. Banks should carry out their analysis and control activities via a user-friendly and standardized “analysis dashboard” in which all available information is consolidated into simple and meaningful evaluations.

Conclusion on digital marketing and sales in banking

The consistent development of digital marketing and sales and the implementation of a systematic analysis and optimization process lead to a large-scale activation of digital contacts. Systematically interlinking classic and digital channels improves the use of contact opportunities, significantly increases sales success and sustainably supports the monetization of omnichannel models. The banks have started to catch up, but much remains to be done.

[1] GfK-Studie, commissioned by Google and Postbank (2017): Customer Journey Banking

One response to “Digital marketing and sales as growth drivers”

Ravi Gill

Digital marketing is the best technique for small businesses.