Robo what?

The term “robo advisor” has come to be defined as a “digital and fully automated asset manager” over the past few years. This description, however, goes rather too far, as a robo advisor in itself is simply a web- and/or app-based customer interface for determining the appropriate risk profile for an investor. It merely digitalizes the WpHG[1] classification and the MiFID II suitability and appropriateness assessment carried out by the client advisor in a traditional advisory meeting. A differentiation between robo advisors only takes place in the subsequent process of actual asset management where the risk profile is translated into a strategic asset allocation and implemented by selecting specific investment products.

Internationally, robo advisors manage approximately EUR 480 bn in assets under management (AUM), which corresponds to about half of the German market for mutual funds. With about EUR 110 bn, Vanguard Personal Advisor Services is the largest provider worldwide and has a global market share of around 20%. The top 5 robo advisors manage about EUR 170 bn, which corresponds to a market share of roughly 40%. The sector is estimated to grow to more than EUR 2,300 bn in AUM over the next five years.

With a volume of about EUR 14 bn in AUM, the European market is relatively small and roughly equals the size of the third-largest robo advisor in the world, Betterment. In Europe, the United Kingdom is the largest market with AUM of EUR 5.5 bn, followed by Germany with AUM of about EUR 3.9 bn. In terms of population size, the Luxembourg market corresponds to less than one hundredth of the German investment market and is thus a niche market for robo advisory as a private client product.

Four robo advisors in Luxembourg market

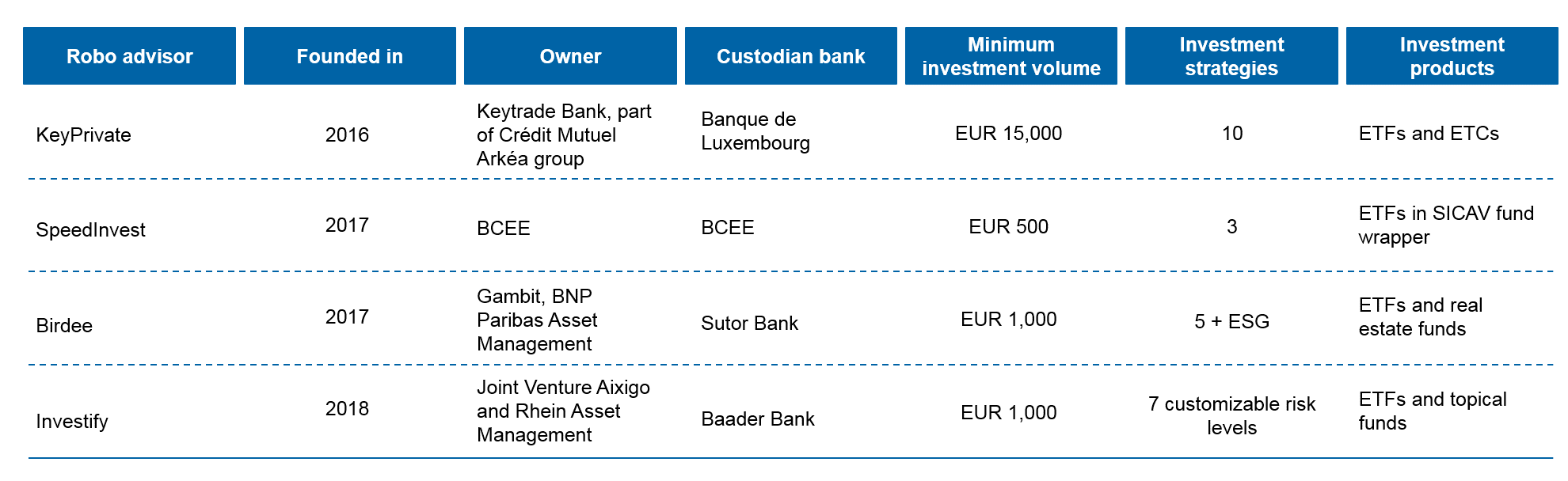

Currently, the four robo advisors KeyPrivate, Birdee, SpeedInvest and Investify operate in the Luxembourg market.

In 2016, Keytrade Bank launched the first B2C robo advisor KeyPrivate to supplement its online brokerage offering. Keytrade Bank is part of the French Crédit Mutuel Arkéa group and a subsidiary of Arkéa Direct Bank. To carry out its portfolio management following robo advice, it uses the Birdee middleware supplied by Belgian fintech company Gambit Financial Solutions, founded in 2007.

In 2017, Gambit Financial Solutions entered the Luxembourg B2C market with its proprietary robo advice offering Birdee. Gambit Financial Solutions is now part of the French BNP Paribas Asset Management.

Also in 2017, Banque et Caisse d’Epargne de l’Etat (BCEE) was the first retail bank with Luxembourg roots to launch a robo advisor, called SpeedInvest. BCEE is Luxembourg’s fully state-owned savings bank.

Since 2018, Investify has also been present in the market. This robo advisor has already been operating in Germany since 2015 and is a subsidiary of German fintech company Axigo, which—similar to Gambit Financial Solutions—also positions its software modules in the B2B business.

Investment strategies and rebalancing

A look at the four robo advisors’ investment approaches reveals the classic concept of simple strategies, usually carried out using ETFs. The asset management offerings differ regarding their strategic allocations in the number of risk profiles (three to ten), the number of ETFs and investment funds used as well as customizability on the part of the client. All providers classify their strategic asset allocation as active with up to daily rebalancing.

SpeedInvest, the Luxembourg savings bank’s robo advisor, positions itself as a basic provider with only three strategies (cautious, balanced and dynamic). Depending on their investment horizon, financial strength and risk appetite, investors are offered a strategic allocation of 80% shares and 20% bonds in the “dynamic” strategy, 50% shares and 50% bonds in the “balanced” strategy or 20% shares and 80% bonds in the “cautious” strategy. The selected asset allocation is put into place using ETFs within a SICAV fund which is posted to the client’s securities account.

Birdee offers its clients five strategic allocations (defensive, stable, moderate, protector, dynamic) with a similar structure of bond and equity ETFs and additionally allocates real estate funds in the more risky strategies. On top of that, ESG concepts are offered. In contrast to SpeedInvest, the selected strategy is not carried out by investing into a SICAV fund wrapper, but—as with all other providers—the ETFs and funds are traded directly on the client account.

With KeyPrivate, the investor is allocated to one of ten risk profiles which differ in their weightings of shares, bonds, commodities and cash. For investments into shares, five ETFs (eurozone shares, US shares, Japanese shares, emerging market shares and APAC shares (excl. Japan)) are used. For investments into bonds, there are also five ETFs (inflation-linked, emerging market bonds, high-yield bonds, corporate bonds and eurozone sovereign bonds). For investing into commodities, ETCs referencing gold and precious metals are available. KeyPrivate uses the Birdee technology, which means that both providers are based on a Black-Litterman portfolio optimization algorithm, supplemented by the respective opinion of their investment experts, for determining the strategic asset allocation.

At Investify, clients are allocated to seven risk classes based on a proprietary scoring. The ETFs and theme funds are also allocated to seven risk classes, depending on their historic volatility. Investments are allocated to clients based on a linear risk allocation in which the individual risk score is represented by capital-weighted investments in different, individual ways. A client portfolio always consists of the basic investment and the theme investment options selected by the client, so that on average about 21 products are allocated to a client account. Investify thus positions itself as a robo advisor with maximum customizability and therefore tends to address more experienced investors who wish get personally involved.

Performance and transparency

In contrast to funds business, where product quality can be measured transparently by means of the fund price, the asset management performance of robo advisors is nontransparent, as the strategies are carried out within the individual client accounts and performance is not published in a certified manner.

In order to offset this weakness and bring transparency to the German market, brokervergleich.de shows a real-life test, where the website operators have opened live accounts, usually with balanced risk profiles, with all German providers to obtain performance data for online publication. However, brokervergleich.de only offers performance data for Investify, which is also available on the German market. KeyPrivate publishes quarterly reports on its website which document the performance of the ten investment strategies offered. For SpeedInvest and Birdee, no data is made publicly available.

Minimum investment

The required minimum investment volume is another factor in which providers differ significantly. While SpeedInvest (EUR 500) and both Birdee and Investify (EUR 1,000) have defined low entry volumes in their business models, KeyPrivate only addresses clients with an entry volume of at least EUR 15,000.

Figure 1: Luxembourg robo advisors: overview of all B2C providers

Figure 1: Luxembourg robo advisors: overview of all B2C providersManagement fee and costs of funds

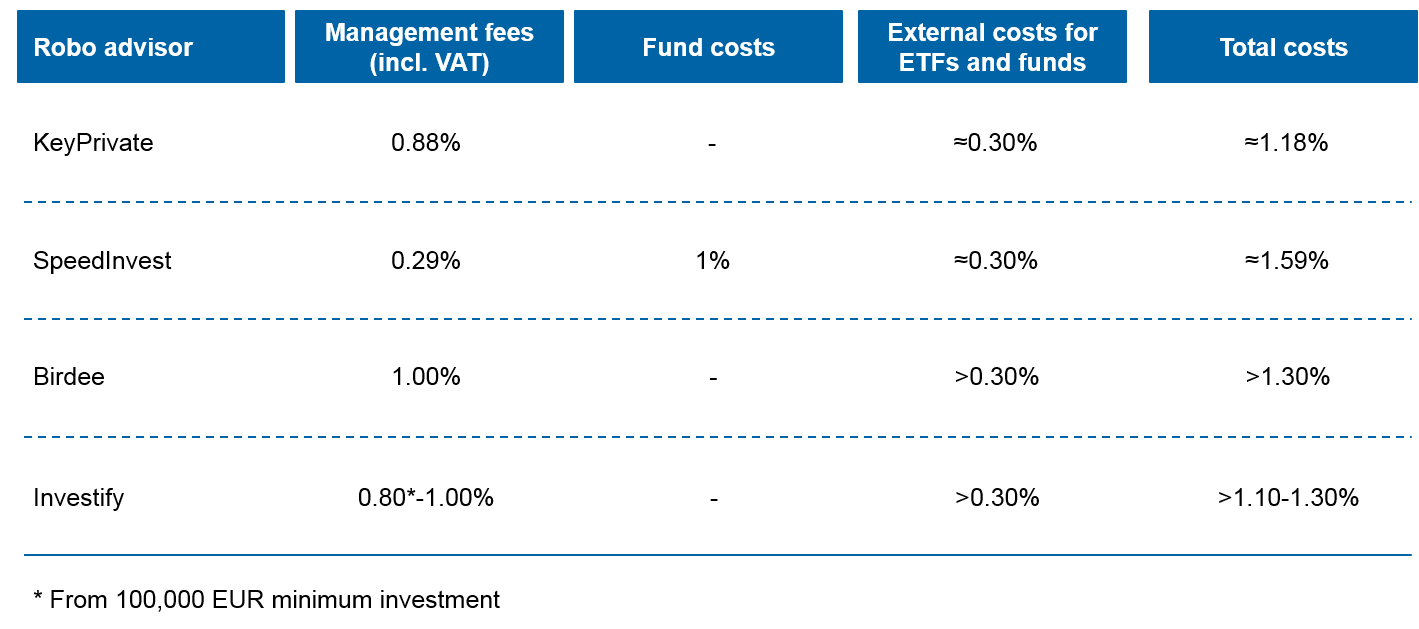

A look at the cost structure of robo advisors reveals few differences. Providers ask for a management fee between 0.25% p.a. and 1% p.a. There are no additional costs for the securities account on which the investment strategy is executed and neither are there any additional transaction costs in case of a portfolio restructuring, e.g. as part of rebalancing or due to inflows or outflows.

Since all providers mainly use ETFs based on shares and bonds to implement their strategies, fund costs are at least around 0.30% p.a. Due to the use of investment funds, Birdee and Investify charge more, depending on allocation and individual setup.

The cost structure at SpeedInvest stands out. It only charges 0.25% p.a. (excl. VAT) in management fees, but there are additional fund costs of 1% p.a. for the SICAV. Since the SICAV is a fund wrapper around the acutal ETFs investments, it can be assumed that the client has to pay a minimum of around 0.30% p.a. additionally for the ETFs and thus faces similar fees as charged by the other robo advisors.

KeyPrivate actually appears to be the cheapest provider due to its low management and fund costs. A precise analysis, however, would only be possible in real-life operation with actual money involved.

Figure 2: What providers charge: fee structure

Figure 2: What providers charge: fee structureConclusion—small, but sweet

The market potential for robo advisors in Luxembourg is limited compared to other European countries. Nevertheless, four providers have created an adequate offering that allows novices easy investing by means of three basic strategies and gives experienced investors the chance to customize their solutions. Actual diffusion into the mass market is only to be expected once robo advice has become part of the standard offering of every bank.

[1] WpHG = German Securities Trading Act

For reference

Robo-Advisor Pros (2019): Robo-advisors With the Most Assets Under Management – 2019

Keytrade Bank Luxembourg (2017): KeyPrivate – The first Robo-Advisor in Luxembourg

Keytrade Bank Luxembourg (2017): Special terms and conditions discretionary portfolio management service

Keytrade Bank Luxembourg (2015): Keytrade Bank relies on Birdee for its online solution for discretionary asset management

Banque et Caisse d’Epargne de l’Etat, Luxembourg (BCEE) (2019): A unique way to invest

Birdee (2019): How do you select the ETFs?

investify (2018): Strategie und Anlageprozess

aixigo AG (2019): aixigo AG – Wer wir sind

investify (2019): So funktioniert’s

Glossary

ETF: An exchange-traded fund (ETF) is an investment fund traded on stock exchanges. It is typically not bought and sold via the issuing investment firm, but via the stock exchange in the secondary market. Most exchange-traded funds are passively managed index funds. For further details, see: wikipedia (2019): Exchange-traded fund

SICAV is the acronym of the French term “société d’investissement à capital variable” or the Italian term “società di investimento a capitale variabile” and refers to an investment company with variable capital, based on French, Belgian, Luxembourg, Swiss, Maltese, Spanish or Italian law. For further details, see: wikipedia (2019): SICAV

ESG is an acronym for “Environmental, Social, and Governance”. The term is used internationally in companies and financial services to express if and how corporate decisions and leadership as well as company analyses of financial services providers take ecological and social aspects as well as governance into account. For further details, see: investopedia (2019): Environmental, Social, and Governance (ESG)

2 responses to “Robo Advisors in Luxembourg”

Ken Van Eesbeek

Very clear overview of the market.

However small remark on the management fees: some are VAT included, others excluded.

E.g. Keyprivate is 0.75% ex VAT, Birdee is 1% incl VAT.

Joël Theisen

Dear Mr Van Eesbeek,

thank you for your comment on the VAT.

We adapted Figure 2 accordingly.

Kind regards,

Joël Theisen