What modeling approaches exist?

How can traditional models be applied?

Various approaches for the valuation of interest rate derivatives exist, such as closed analytical models, numerical methods, finite difference methods and data-based approaches. The Hull-White model developed in the 1990s is frequently used in the financial industry. The advantages of the model are its efficiency, transparency and its ability to account for mean reversion, i.e. the tendency of short-term interest rates to revert to a long-term mean.

However, the Hull-White model also has some weaknesses: It is a single-factor model, which means that complex market dynamics cannot be fully captured. Furthermore, it is based on the assumption of a normal distribution of market interest rates, which means that extreme events are underestimated, and structural changes (e.g. negative interest rates) can only be taken into account to a limited extent. Numerical methods such as Monte Carlo simulations are the better alternative, especially for exotic derivatives or in times of high volatility. Ultimately, however, these models also reach their limits, as they are significantly more time-consuming and computationally intensive.

What options are there for using AI?

A promising alternative approach is the use of AI, in particular ML. Essentially, these terms refer to technologies that enable computing systems to learn from data and recognize patterns without being explicitly programmed for this purpose. While AI generally aims to replicate human intelligence, ML focuses on the development of algorithms that can create and improve models themselves to solve a complex problem or make a prediction.

Algorithms based on deep learning (DL) can offer advantages for the pricing of complex products. DL is a subfield of machine learning that is based on artificial neural networks and was specifically designed to process large and complex datasets. The DL architecture is based on multi-layered networks (so-called deep neural networks) that recognize abstract dependencies, enabling the analysis of complex patterns. This article provides a comprehensive explanation of how neural networks work.

What are hybrid models?

One of the most frequently criticized weaknesses of neural networks is their lack of explainability (“black-box nature”), as the decision-making processes within the architecture are difficult to understand. This is of great importance in strictly regulated industries such as finance, where model transparency is absolutely essential. One possible solution is a hybrid model that combines traditional methods and DL. For example, an established mathematical model like the Hull-White model can be enhanced with machine learning to dynamically adapt to market data while remaining interpretable. This can be achieved, for example, by training an algorithm to derive model parameters using a so-called deep calibration approach.

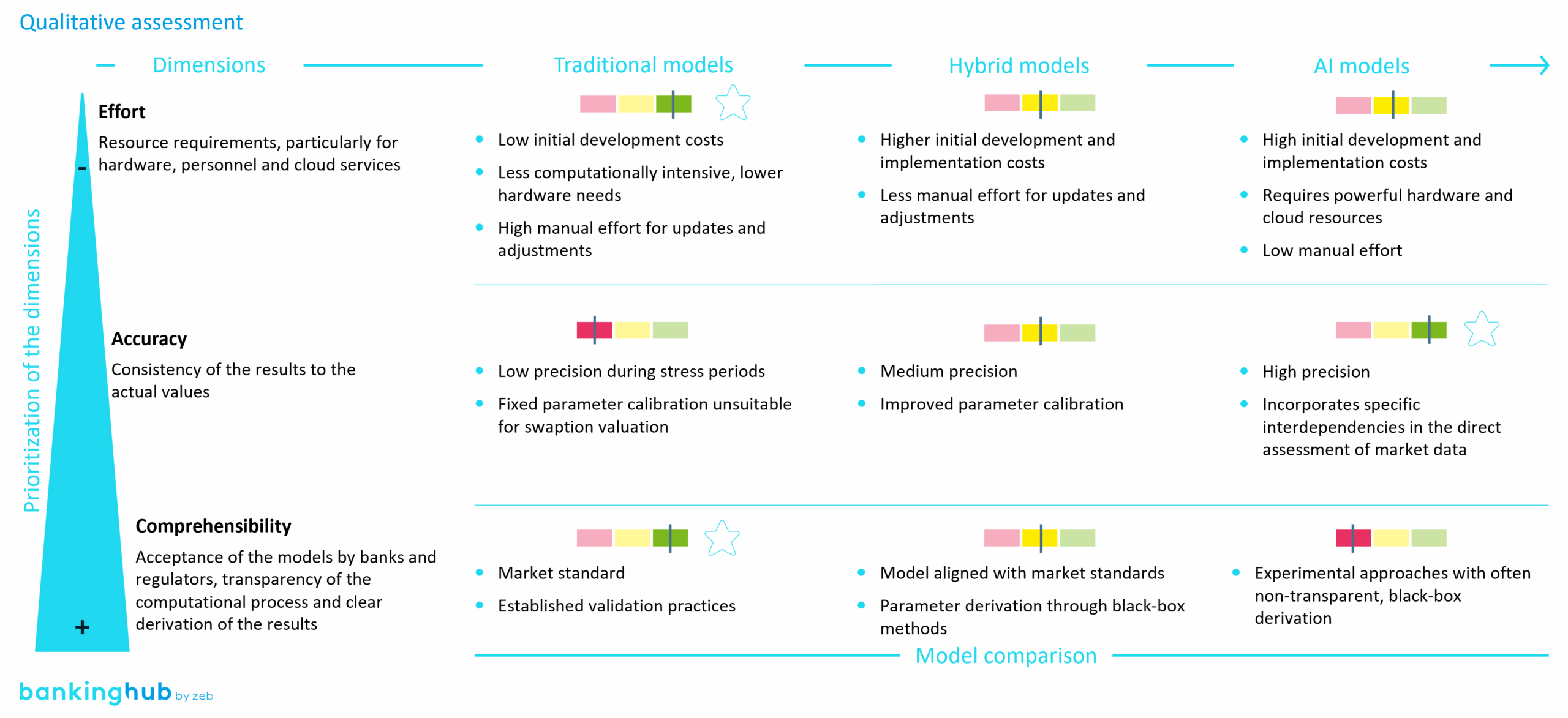

The following figure offers a summary of the qualitative assessment of the various approaches.

Figure 1: Qualitative assessment of the model approaches

Figure 1: Qualitative assessment of the model approachesHybrid models therefore combine the best of traditional approaches and modern AI. Their main advantage lies in improved regulatory acceptance, as they preserve the structure of closed-form analytical models. In addition, hybrid models offer greater adaptability to short-term changes in market conditions, as they can be continuously recalibrated.

Hybrid models are particularly effective in the presence of structural changes, i.e. sudden regime shifts in the data, since they can retain historical knowledge while flexibly integrating new patterns. Machine learning also contributes to time savings, especially through the automated calculation of input factors that feed into the traditional model. On the downside, training AI components can be costly, particularly when dealing with complex data structures. Last but not least, developing hybrid models requires deep expertise in both financial mathematics and computer engineering, which makes their implementation more demanding.

Test calculation: how can the modeling be carried out?

To evaluate the performance of different modeling approaches for estimating market prices, extensive test calculations were conducted for payer swaptions on the 12-month Euribor during a stress period – the COVID-19 pandemic. Forecast accuracy served as the key metric to assess how closely the model-based price estimates aligned with actual market prices. The results are illustrated in the following figure.

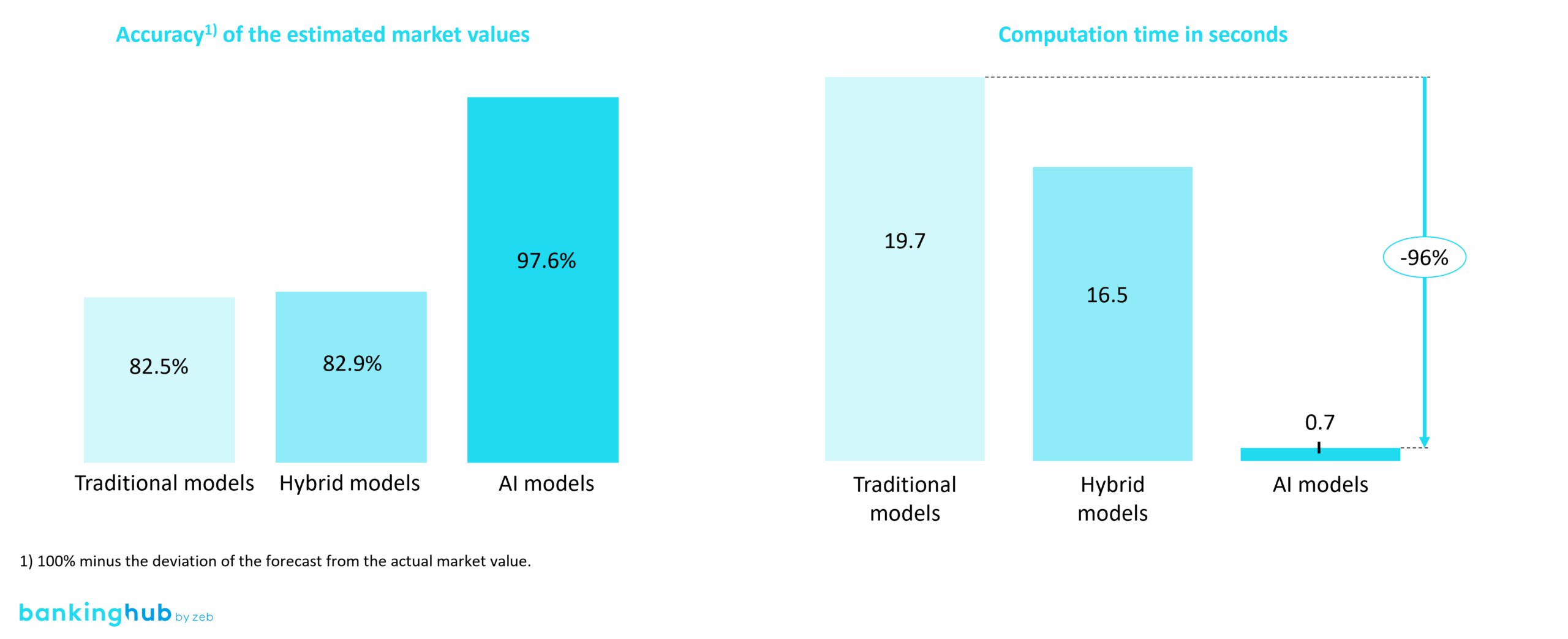

Figure 2: Results of the test calculation

Figure 2: Results of the test calculationThe traditional approach, a Hull-White model, shows solid but limited precision. While market prices can generally be estimated reliably (with an accuracy of 82.5%), the model reaches its limits during the stress period under consideration. A significant limitation results from the use of a fixed model parameter combination (α as the speed of mean reversion and σ as the volatility of the short-term interest rate), which means that the model cannot adequately reflect all market conditions.

An alternative hybrid approach combines the traditional model with deep calibration methods using neural networks. This leads to slightly improved modeling, although the accuracy is only marginally higher than that of the traditional model (82.9%).

The purely AI-based method, which uses a neural network with 100 neurons, proves to be significantly more powerful. It achieves an accuracy of 97.6% and allows flexible adaptation to different market conditions without producing systematic errors for specific maturity combinations. This approach offers a robust estimate of market prices and minimizes distortions, particularly in stress periods, although slight tendencies toward overfitting can be observed. Overall, the AI method proves to be the most effective approach, as it combines high precision with strong adaptability.

Is the AI model a viable option?

In summary, the test calculation shows that the pure AI model achieves the fastest and most accurate pricing results even in stress periods. However, the applicability and acceptance of the method are limited due to its black box properties. Nevertheless, applications outside highly regulated areas and parallel operation alongside a traditional model are feasible options.

For activities that are subject to high regulatory requirements, the hybrid model is a useful addition, as time savings can be achieved and experience with machine learning can be gained while continuing to use established, regulatory-compliant models.