Why are legacy control mechanisms being outpaced by fraud in a real-time payment world?

Banks still monitor fraud using traditional rule-based systems, fixed thresholds, manual alert reviews and investigations that happen after transactions are completed. This approach was built for a slower payment world, where transfers could be checked or stopped before settlement. While attacks now happen in seconds and often at scale, many detection processes still take hours or even days. Fraud teams investigate alerts one by one, often after the payment has already been cleared. This creates a structural imbalance: automation on the attack side; manual intervention on the defense side.

Fraud patterns also differ by payment rail: cards and card-not-present (CNP), A2A and instant payments as well as wallets or P2P each show their own typologies and latency requirements. This increases the pressure for rail-specific control mechanisms. Modern defense systems therefore need E2E AI: supervised models for known fraud patterns, anomaly detection for emerging behavior and graph analytics to detect coordinated networks. At the same time, attackers leverage deepfakes and synthetic identities, raising the bar for real-time, in-flow decisioning.

Figure 1: Fraud prevention gap

Figure 1: Fraud prevention gapThis gap has created a structural imbalance between attackers and defenders. Fraudsters operate with automation, scale, and AI using deepfakes, synthetic identities, and large-scale social engineering to bypass controls. Meanwhile, the defense side remains reactive and manual. This systemic gap exposes the payment infrastructure to significant risk.

How can AI be used to prevent fraudulent activities powered by AI?

The transition to real-time, AI-enabled fraud has made it clear that each fraud scenario requires its own defense strategy. While PSD3 and the Payment Services Regulation (PSR) strengthen the overall framework for security, liability and data access, they were designed around traditional risk models and therefore do not yet fully align with AI-driven prevention methods. As a result, institutions must deploy targeted measures and specialized analytics to close this gap and ensure that their controls remain effective across all fraud types.

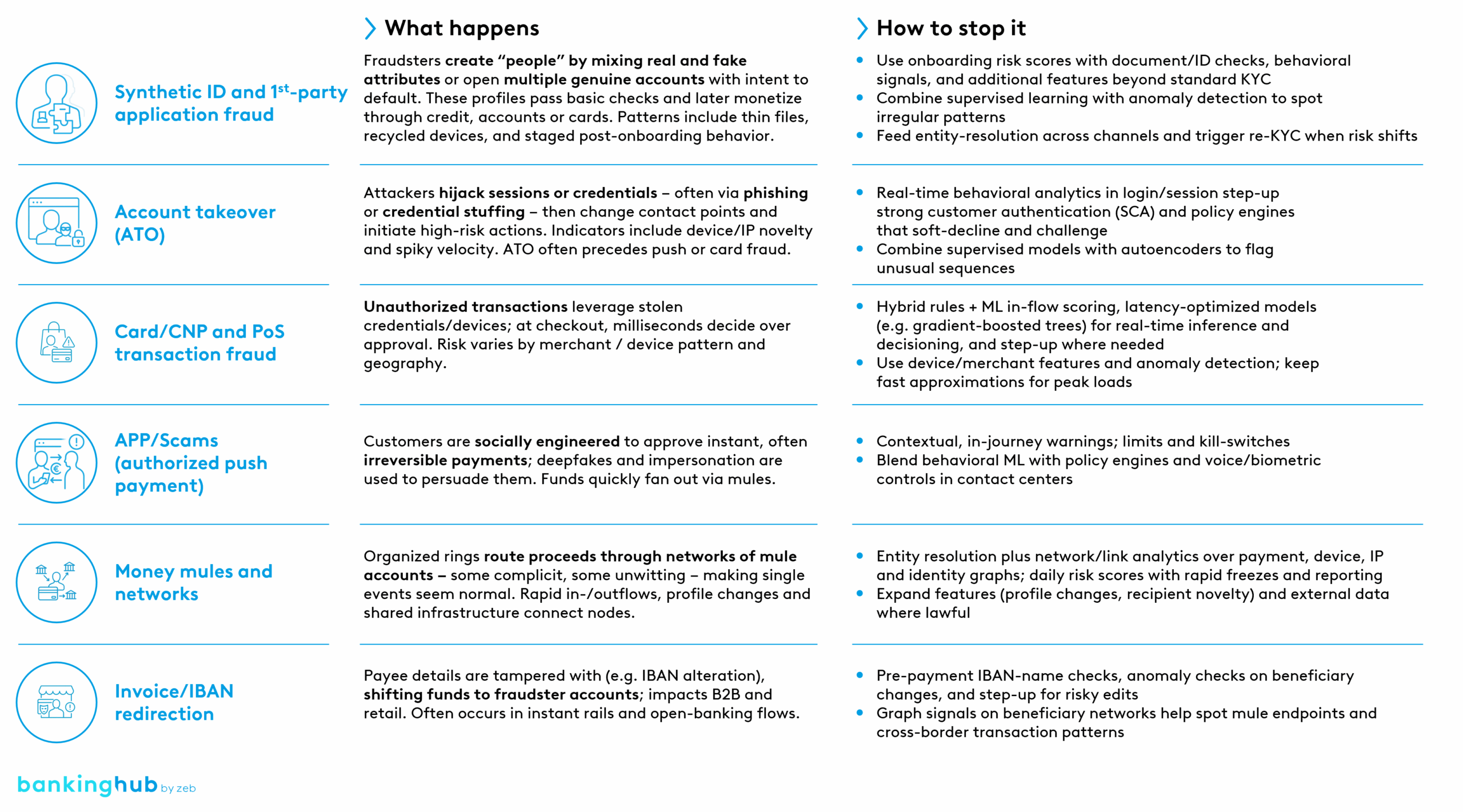

The following table illustrates how typical fraud scenarios unfold in practice and which AI-supported countermeasures are required to contain them:

Figure 2: Catalog of fraud types and matching countermeasures

Figure 2: Catalog of fraud types and matching countermeasures