While the importance of digital services has been rising steadily over the past years in a number of areas, the ubiquity of the internet via mobile devices became a reality with the present COVID-19 crisis. In the wake of such dramatic changes, banks have adjusted to this new normal too. As a consequence, mobile banking applications have gradually moved from niche to mass-market, becoming a fuel to improved bank performance.

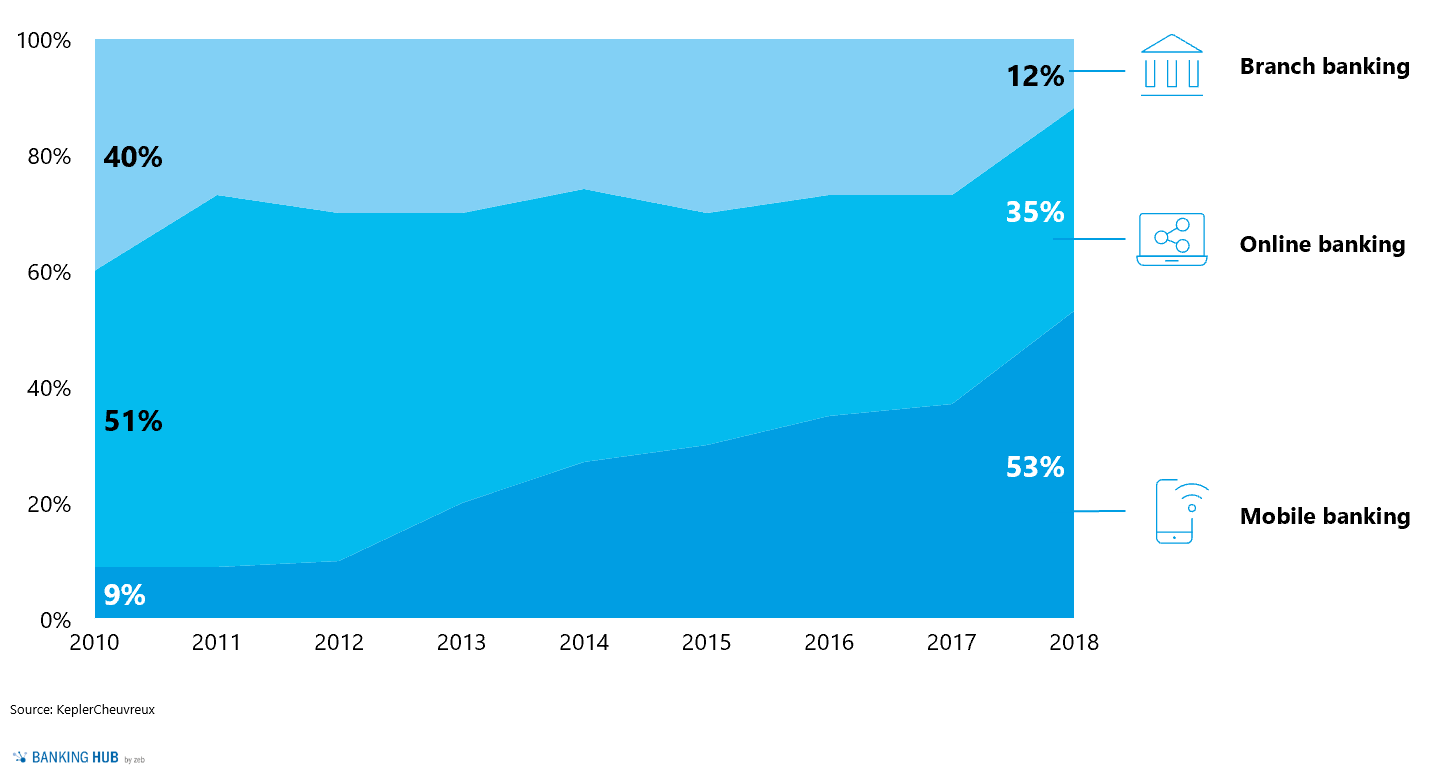

In fact, the lockdowns related to the COVID-19 crisis caused more than half of global shoppers to use digital payment tools more frequently than before the pandemic started. However, even prior to the crisis, proportions of digital and face-to-face interactions in banking had reversed on a global scale (see figure 1).

While four out of ten people would visit an advisor at their local branch ten years ago, five out of ten customers now use a mobile banking application, with only one still coming into the branch. In light of these developments, zeb has accelerated its efforts and conducted the most in-depth study available on the market on mobile banking across several European countries.

Figure 1: Global evolution of the customer-bank interaction by channel

Figure 1: Global evolution of the customer-bank interaction by channelIn Luxembourg, more than a third of the residents used their smartphones regularly to check their account balance in 2018, which represents a 20% year-on-year increase. The shift toward digital tools is remarkable and presents a real challenge for traditional retail banks. At the same time, it also reflects the consumers’ wish for further enhanced and more comprehensive mobile banking offerings.

The article on mobile banking in Luxembourg at a glance:

Assessing mobile banking applications in the Greater Luxembourg area

As part of an international study on the current performance of retail banking in the digital field, zeb assessed the situation of the main retail banks in the Luxembourg market from the customers’ point of view. As Luxembourg is a very diverse market, with several relevant players located outside of the borders, we analyzed the mobile banking offerings of 6 local banks as well as 3 banks from the Greater Region and benchmarked them with international best practices mainly from Neobanks de facto threatening local markets across Europe as well.

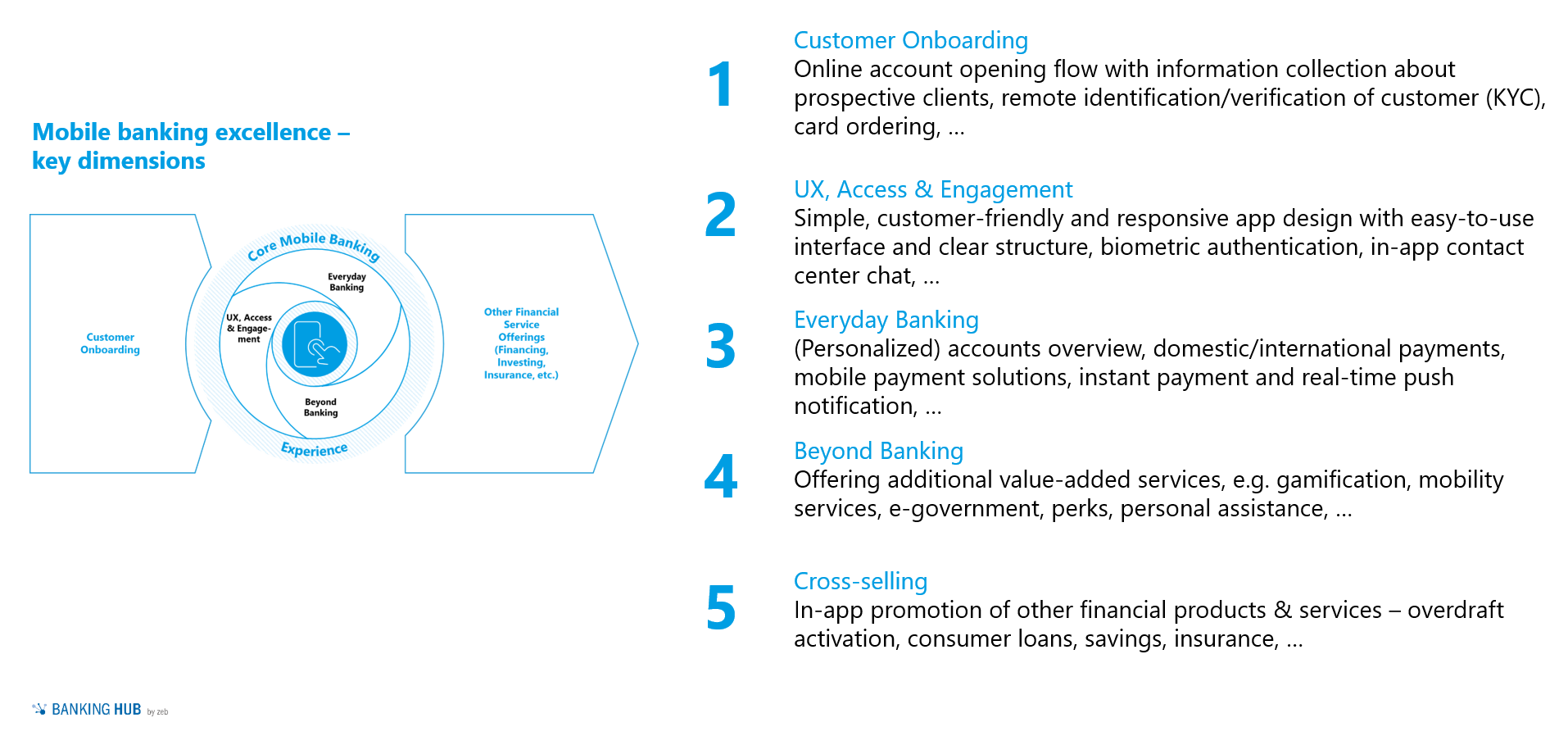

Figure 2: Mobile banking assessment framework

Figure 2: Mobile banking assessment frameworkThe basis for our comparative analysis was a set of more than 100 criteria, each of them addressing a specific aspect of the mobile banking system.

We specified these criteria within 5 general categories:

- Customer Onboarding: Here, we mainly examined the account opening process as well as the information required by the bank to verify a customer’s identity (KYC), but also included personalized greetings for first-time access and potential in-app tutorials.

- UX, Access & Engagement: In this category, we tested the accessibility and consistency of the platform, its communication tools, the user interface of the application, and the possibility to personalize the application. Moreover, we analyzed the log-in process and its security components.

- Everyday Banking: Here, we assessed the different options for daily banking operations, management of multibank systems, and the availability and viability of various payment options.

- Beyond Banking: We looked at the availability of additional services such as loyalty programs, special offers or mobility services. These included, among others, discounts on other non-banking-related products, concierge services, donations and integration with service providers.

- Cross-Selling: This category considers other banking products, such as insurance, loans and investment products, that were offered to the customer through the mobile application.

We used these five categories – comprising a total of 115 criteria – to grade the banks’ mobile banking solutions on a scale from 1 (not available) to 5 (outstanding) for each criterion. Thus, our study enabled us to not only assess the overall performance of each bank but also to precisely analyze the apps along the five main categories and detect relevant room for improvement. This makes our study the most comprehensive and in-depth study in the market.

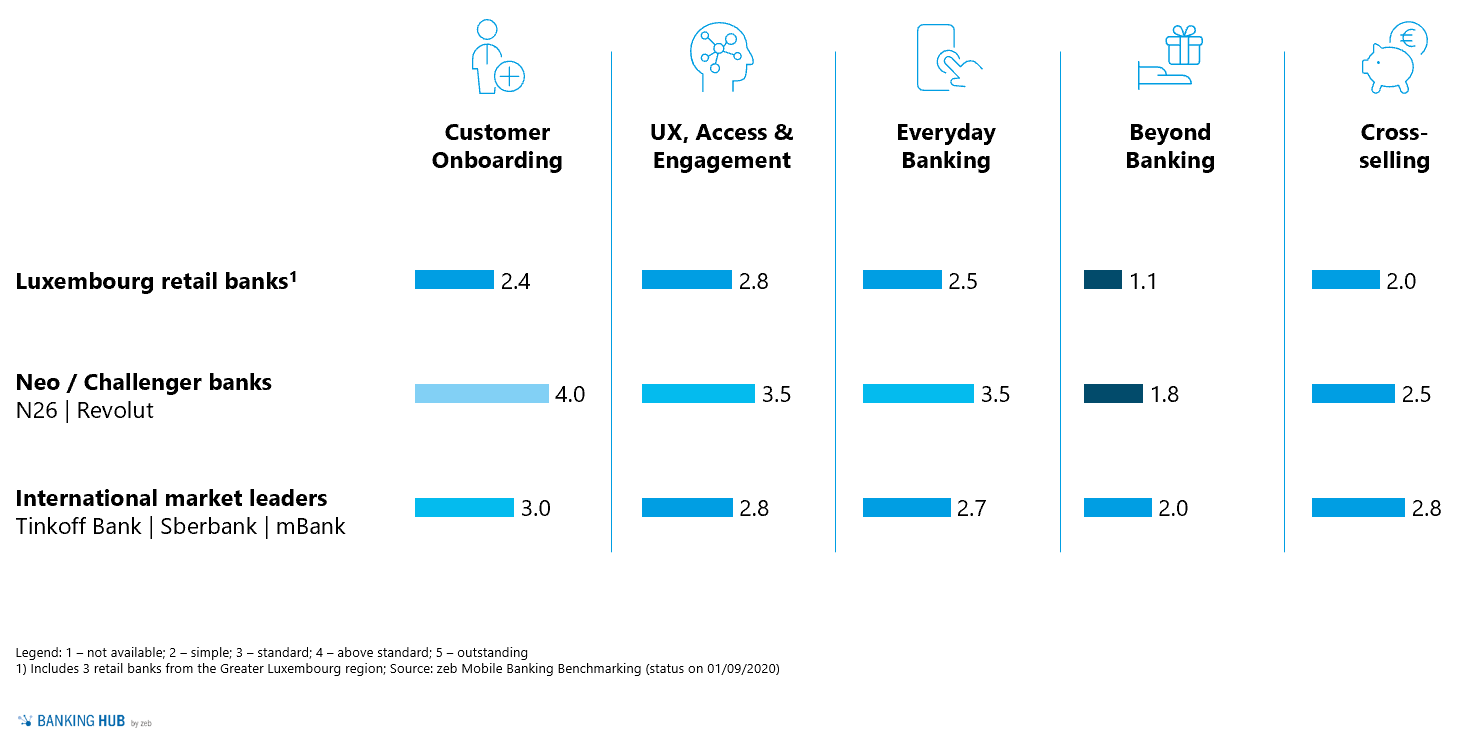

A broad overview of the banks’ performance

The overall performance of the banks we tested turned out to be average considering what one would expect from a dynamic financial place such as Luxembourg. Comparing the average aggregated results of the Greater Luxembourg banks with European Neobanks and international market leaders reveals significant room for improvement particularly in the areas of customer onboarding, beyond banking and cross-selling.

Figure 3: Luxembourg mobile banking benchmarking

Figure 3: Luxembourg mobile banking benchmarkingIn the following, we will narrow down the analysis by looking at each of the five main categories separately in order to better understand the strengths and weaknesses of the Luxembourg banking market.

Strengths and weaknesses of mobile banking in Luxembourg

Customer Onboarding

As laid out above, banks in Luxembourg still suffer from significant weaknesses in their digital interaction with customers. Unfortunately, customers are confronted with this right from the start. Out of the 9 assessed institutions, only one provided customers with a fully mobile end-to-end onboarding process, while another displayed a hybrid mobile version of the application (i.e. website integrated into the app).

Moreover, while most banks enable customers to register online through their website, a significant number of institutions subsequently require them to send paper files by postal mail, which leads to significant delays. While most banks indicate an average time between 5 and 20 minutes to go through the account opening process, this only takes into consideration the “request” part of the process and excludes the bank’s examination of requested documents. On average, 14 working days go by between initial registration and the full usage of the account including the mobile banking. Still, this figure hides strong disparities, as we encountered total onboarding times from a few days up to a total month.

In comparison with international best practices and fierce competition from Neobanks, our analysis reveals a key weakness of Luxembourg banks to be tackled with high priority, particularly in the context of an expansion of the target customer base to the Luxembourg Greater Region and a market dominated by immigration.

Although it is evident that there is huge room for improvement, there are also some bright spots. One of them is the fully mobile client-ID verification. In this field, new technologies have indeed been strongly integrated in order to perform secure, and most importantly, fast KYC checks.

UX, Access & Engagement

While the banks’ performance in the first category was mostly underwhelming, the overall accessibility of mobile applications and their architecture – assessed in this category – show much more pleasing results. As a whole, the mobile banking applications present clear visuals, with intuitive interfaces. This helps to make the banking apps accessible for all types of users and allows the users to comfortably navigate through the application.

However, improvements are still necessary – in particular regarding the overview of transfer processes which are more often than not fragmented and confusing. A clear step-by-step guide with a lucid summary of all relevant information is rare. In addition, the communication between bank and customer – be it through FAQs, hotlines or in-built chat options – leaves much to be desired.

Everyday Banking

Concerning the core competence of retail banks, the provision of everyday banking services, zeb identified an overall satisfying performance on the part of the banks that were looked at.

While the majority of banks have a comprehensive account overview and management, they struggle to provide in-house solutions for instant payments, scan-to-pay or NFC payments. Yet, basically all banks make up for the lack of these features by integrating Apple Pay and Digicash, an innovative Luxembourg payment solution. Regarding multi-bank account aggregation, a feature that is becoming increasingly popular in the wake of PSD2, the results are mixed: most banks fail to offer multi-banking at all, while some stand out with very sophisticated solutions.

Moreover, zeb found striking differences between the 9 banks in the management and handling of account-related debit or credit cards. Around half of the banks’ mobile apps include easy and intuitive card overview and card management pages, whereas the other half are still lagging behind in this area.

Beyond Banking

In this category, we focused on features like loyalty schemes, special offers, mobility services and e-government (i.e. digital signature, possibility to apply for government support or availability of an e-card storage). The results were sobering. Most of the above-mentioned features were not available at any bank, while other features – largely in the area of e-government – are only provided through a shared digital identity provider, LuxTrust. However, we discovered some rather handy in-app services such as the possibility to pay via smartphone at the gas station without having to go to the checkout or the option to make use of concierge services via the selected credit card.

Still, it appears that the Luxembourg banks have yet to develop viable beyond banking offerings. This should not distract from the fact that the financial services sector as a whole steadily moves towards a future in which ecosystems and beyond banking offerings will play a key role. Therefore, zeb views it as vital that the banks embrace the challenge and work on sound offerings for their customers.

Cross-Selling

Similar to the performance in the previous category, the financial institutions do not impress in the cross-selling category either. The overall scores are slightly better, but many banks fail to tap into the potential of cross-selling. While some banks do offer simple cross-selling opportunities for savings, loan and investment products, almost all of them overlook the insurance business.

Thus, the potential for improvement is huge. Personalized pre-approved credit lines, individualized advertisements for investment products or in-app insurance application and management – to name a few – are still a long way off. When implemented appropriately, they do offer enormous cross-selling potential. Key for all of this, naturally, is a profound and comprehensive understanding of the customer which many banks have not yet been able to gain despite initial efforts in the area of data analytics (e.g. by not introducing multi-banking functionalities, see ‘everyday banking’).

Mobile banking study wrap-up

The results of our study were feeble yet not discouraging. All mobile banking apps we assessed had good features, but none managed to convince across the board. In fact, looking at the average scores across all five categories, only two out of the nine banks achieved an average score of 3.0 or more – our grade for market standard and not truly innovative applications. Given the increasing importance of mobile banking for customers, the banks should take these results as a boost to their motivation.

The strategy should be clear: elevate the standard mobile banking services, which were at least decent from all banks, to a new, more innovative level and – at the same time – substantially integrate modern features in the fields of customer onboarding, beyond banking and cross-selling. Particular emphasis should be put on onboarding as it risks initiating a business relationship with a negative connotation accordingly to the mantra “you never get a second chance to make a first impression”.

This becomes all the more important against the backdrop of a financial industry that slowly but steadily moves towards a platformized and customer-centric service offering. With 97% of millennials using mobile banking, banks have to provide sound mobile banking offerings in order to be successful in the future. For our sample, this should serve as a small signal of affirmation. Most are taking the right path. But from now on, they should take the highway – and never look back.