A look back: carbon accounting and decarbonization pathways[1]

Carbon accounting in the financial sector has developed rapidly since the Paris Agreement adopted in 2015: financial institutions are obliged to systematically record their financed emissions and align them with global climate targets. Frameworks such as TCFD have created standards for assessment and comparability, while regulatory requirements such as CSRD and EBA guidelines firmly anchor carbon emissions in strategy and risk management.

At the same time, banks use science-based scenarios (IEA, CRREM, NGFS among others) to derive decarbonization pathways for their portfolios. As a result, the focus is increasingly shifting to the question of whether measured emission reductions have actually been achieved through internal measures or are due to external effects – a key challenge for future progress assessment.

Which regulatory frameworks govern GHG progress measurement and GHG management?

Regulatory requirements for GHG progress measurement and management in the financial sector have increased significantly in recent years. Financed GHG emissions are defined as a key parameter for fulfilling various ESG reporting obligations and for integration into ESG risk management.

With the introduction of the CSRD and the associated European Sustainability Reporting Standards (ESRS), financial institutions are obliged to actively set climate targets, define measures to achieve these targets, assess their effectiveness and make adjustments if necessary. Even if the number of financial institutions reporting pursuant to the CSRD is very likely to decrease as a result of the Omnibus initiative, there are still supervisory requirements for the adequate operationalization of ESG risk management.

EBA guidelines and the Minimum Requirements for Risk Management (MaRisk) mandate that institutions carry out regular target/actual analyses in order to evaluate the measures and the progress towards their targets. Transformation plans must be designed dynamically and adapted accordingly if framework conditions change. As interdisciplinary topics, ESG criteria should be formally and transparently integrated into strategy, management, risk framework and governance.

zeb has identified regular monitoring of the progress towards target and actual decarbonization targets as a key component of effective GHG management and transition. Drivers of carbon emission must be precisely identified in order to clearly distinguish genuine transformation effects from other influences. The following chapter explores tried and tested zeb solutions.

How can an approach for a GHG management process look like?

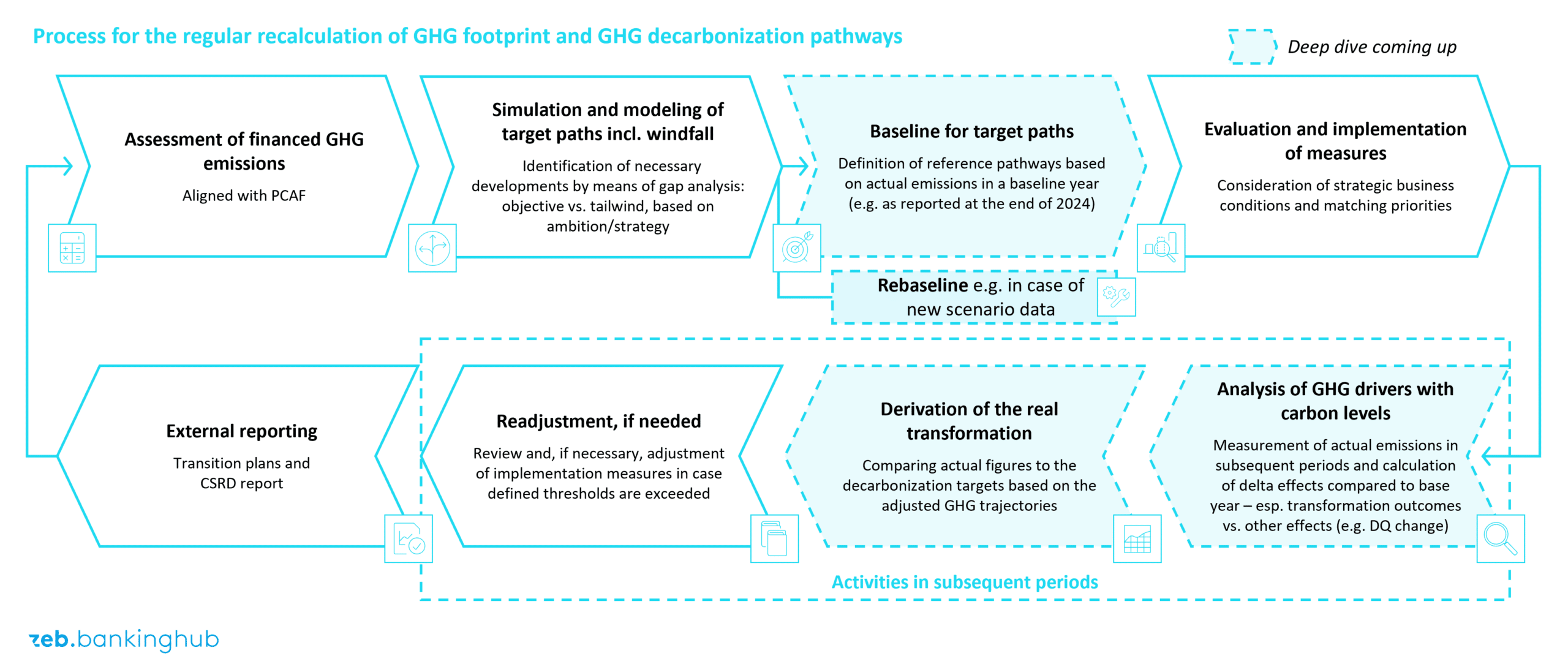

For targeted and regulatory-compliant GHG management, a regularly recurring, clearly structured process is recommended, which typically comprises the steps shown in Figure 1.

This management cycle must be structured in such a way that it enables both continuous progress assessment and flexible adaptation to new findings and framework conditions. The first step is the initial assessment of the financed emissions. Based on this data, quantitative and qualitative analyses are carried out, linking science-based climate paths, regulatory requirements and the institution´s strategic ambition. The result is a clearly defined GHG target trajectory, including an analysis of the gaps between the projected actual pathway and the intended decarbonization pathway.

This establishes a robust baseline that forms the quantitative starting point for all future progress assessment and consistently links current actual emissions with the reference pathways. In practice, this takes place on a fixed date (e.g. at the end of the fiscal year). Using this baseline as a foundation, simulations and measures are developed to concretize the path towards achieving the targets. Our previous series of articles provides a more in-depth look at additional steps.

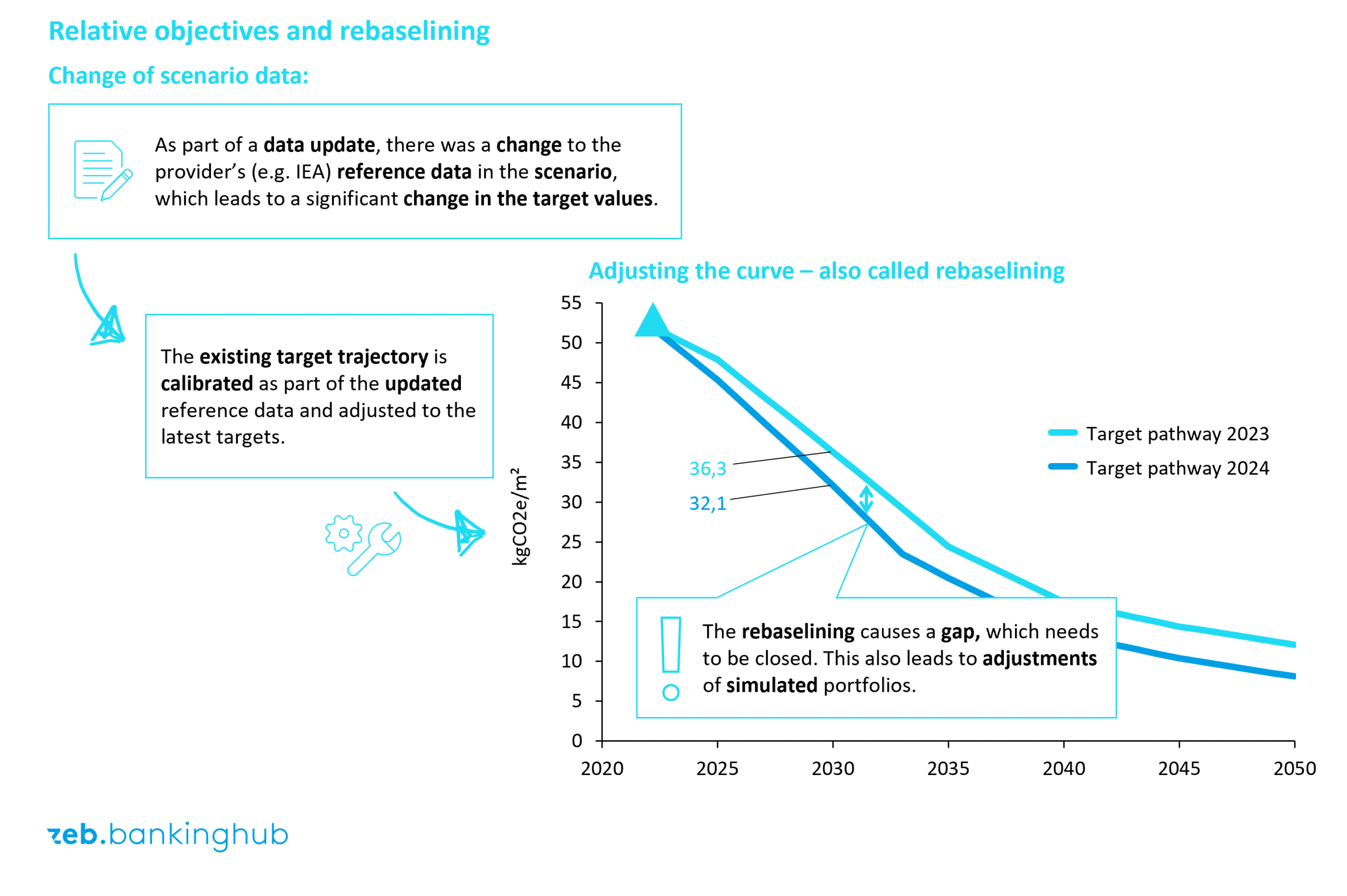

Rebaselining – either event-related or periodic updating of the baseline referenced in target pathways – plays a key role in this process.

What do baseline and rebaselining mean in relation to target pathways?

The baseline, alongside measurement and scenario analysis, forms the jumping-off point for quantitative GHG management. Anchored in a fixed baseline year, it translates external reference pathways (e.g. IEA, CRREM, NGFS) into portfolio-specific emissions targets (see our article “Decarbonization pathways for financial institutions: overcoming challenges with practical solutions” for more information).

First, a representative baseline year is defined and enriched with validated PCAF data (emissions, portfolio balances) to ensure the comparability of future KPIs. Based on this, sector and portfolio-specific reference pathways are evaluated – including CO₂ price assumptions – in order to derive a realistic target range between minimum and stretch targets. The resulting baseline quantifies implications regarding risk, earnings and business model and thus ties in directly with the GHG management logic of the previous chapter.

As soon as new data, methodological adjustments or structural portfolio changes reduce the value of referencing the original baseline, rebaselining becomes necessary (see Figure 2). Historical series of emissions data are scaled retroactively to the updated baseline in order to maintain KPI consistency and avoid misinterpretations in the target/actual comparison. Transparent documentation ensures that the management logic remains transparent and that the data continues to be relevant to decision-making.

How are the GHG drivers analyzed to derive a CO2 level?

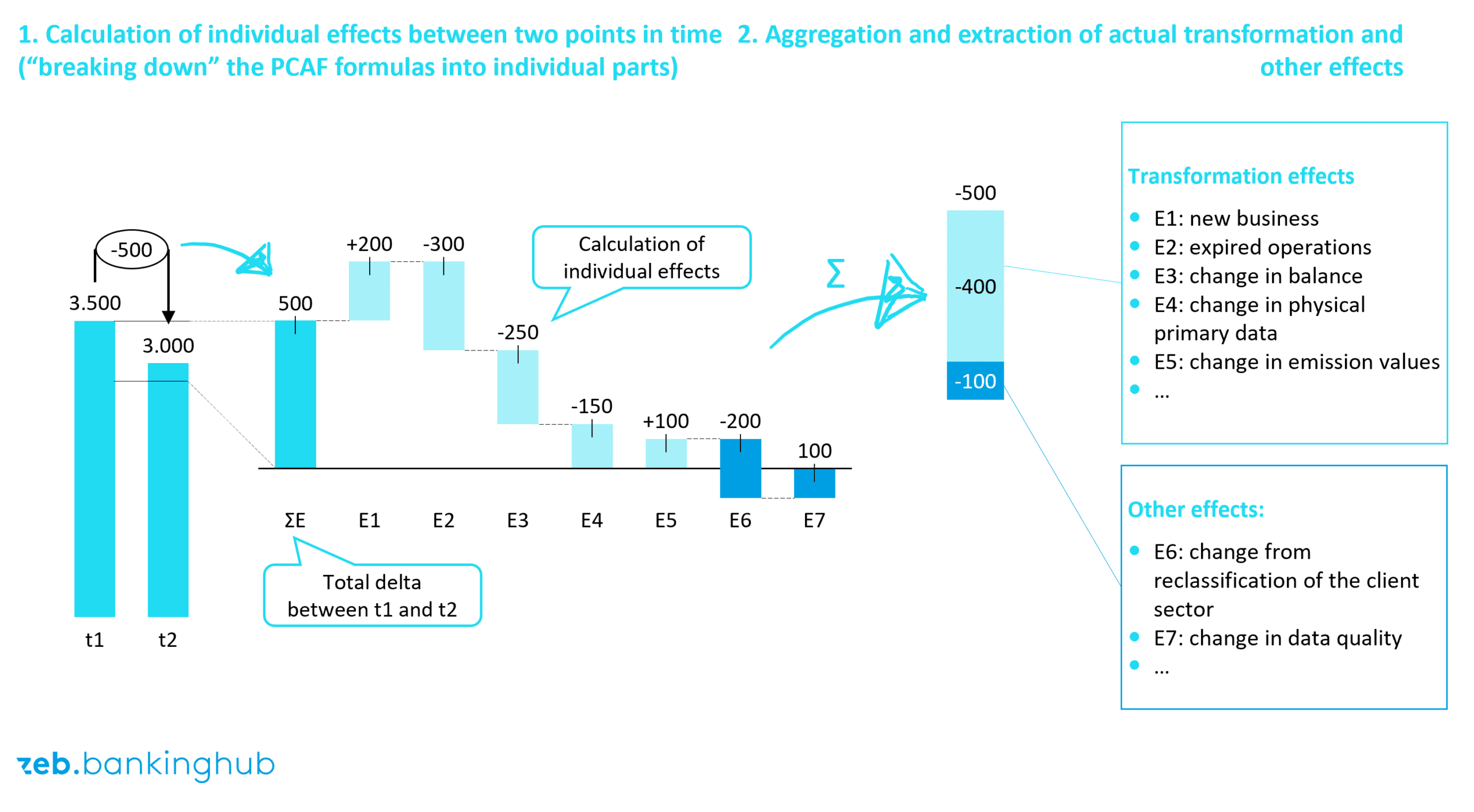

A key component of GHG progress assessment is the detailed analysis of emissions trends between two points in time (usually a comparison of the current reporting date with the baseline date and/or the start of the current year). The CO₂ level serves as a tool to display individual effects transparently and to clearly distinguish actual transformation outcomes from other effects (see Figure 3).

Initially, the differences in financed emissions between two reporting dates are determined. To achieve this, structured alternative calculations are carried out by combining input data determined specifically for both points in time. This procedure enables a precise breakdown of the overall outcome into clearly delineated individual effects. This allows for a differentiated view of individual influences such as changes in the balance, production data and adjustments to emission factors / emissions. A comparison of the individual effects with the overall outcome serves as a control to ensure that all changes can be fully traced and assigned.

Drill-down analyses can be used to examine the identified individual effects in detail at the level of businesses, persons or objects. This creates transparency about the specific causes of changes in emissions.

The isolated individual effects are then aggregated into two categories:

- Transformation effects: genuine changes resulting from management measures taken by the institution, such as strategic new business, portfolio adjustments or changes in emission factors or emissions

- Other effects: external or methodological changes, e.g. balance sheet/market value adjustments or corrections to data quality

This methodical separation enables the CO₂ level to clearly differentiate between the actual reduction in emissions (transformation effects) from other, often immutable changes. Thorough analysis is essential in order to fairly assess progress towards the climate targets and to be able to effectively derive measures for targeted readjustment.

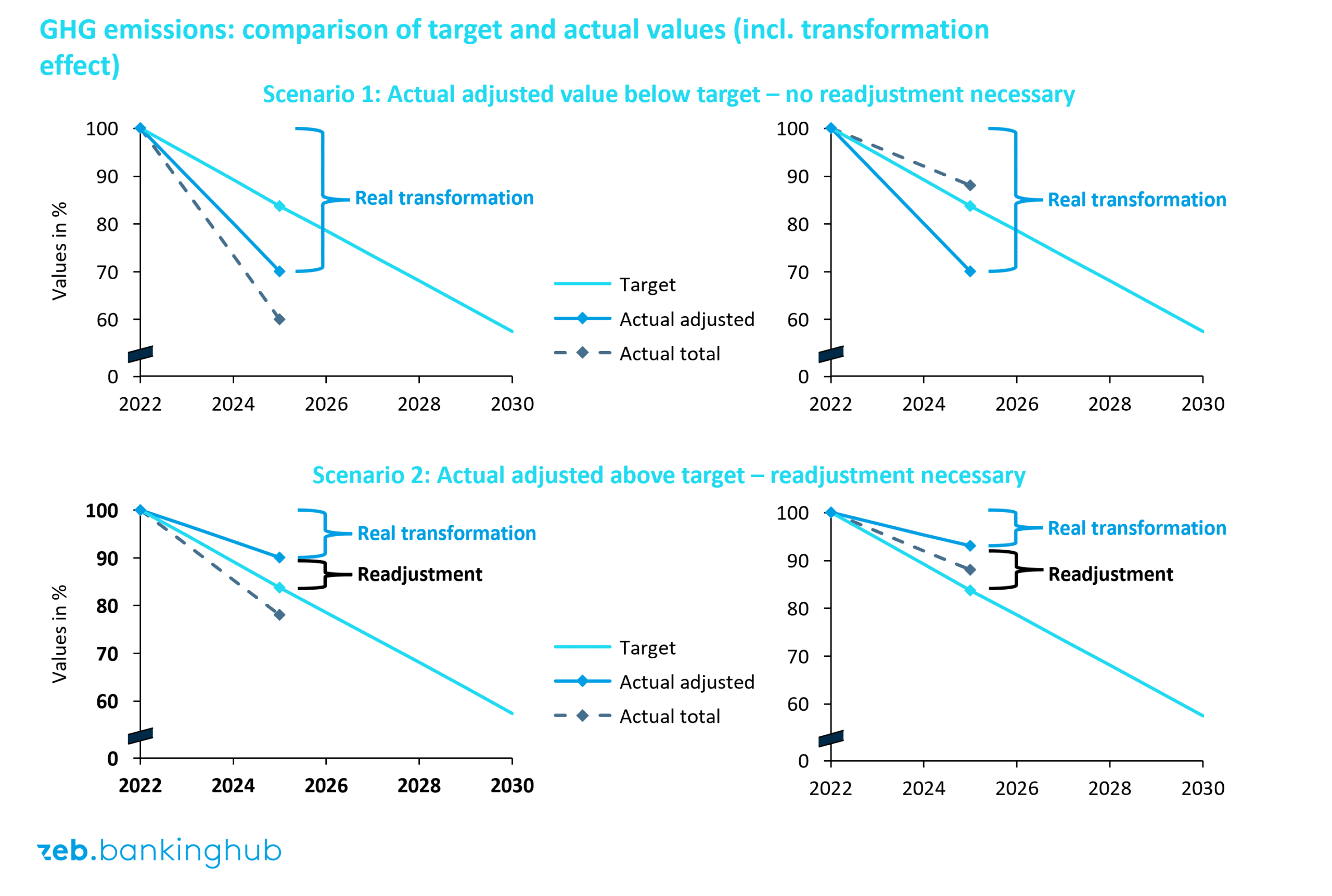

How can real transformation be derived?

For the effective management of decarbonization in the financial sector, it is crucial not only to compare the planned GHG reduction pathway (target) and the measured actual GHG pathway, but also to create an adjusted view of the actual changes regarding financed emissions. This is the only way to differentiate between genuine transformation results and unique or side effects, e.g. changes in data quality or external market influences. This adjustment is crucial in order to be able to arrive at valid conclusions about the effectiveness of implemented measures.

An adjusted target/actual comparison results in one of two possible scenarios (see Figure 4[2]):

- Scenario 1: The adjusted actual trend is below the planned target pathway. This indicates a successful transformation, meaning no additional readjustment is required.

- Scenario 2: The adjusted actual trend is above the planned target pathway. There is a need for readjustment: the measures taken are not sufficient to decarbonize the portfolio. Targeted readjustment (e.g. reexamination, simulation and correction of measures) is necessary in order to return to the target pathway.

Thanks to this differentiated approach, the analysis of the real transformation not only enables a precise evaluation of the previously implemented measures, but also the derivation of correct recommendations for effective management of future emissions development.

What is our conclusion on GHG progress measurement and (re)baselining?

Regulatory requirements, particularly from the CSRD, the ESRS, the EBA guidelines and MaRisk, require institutions to actively integrate the reduction of emissions into their strategic orientation and operational management. A structured process for GHG management has delivered effective results. It includes every step from the initial calculation of the financed GHG emissions to the detailed analysis using CO₂ levels up to the assessment of real transformation effects. Especially the creation of a sound baseline, transparent (re)baselining and the regular detailed analysis and highlighting of genuine transformation effects have proven to be decisive success factors.

zeb offers a holistic approach to establishing effective GHG management based on extensive experience with practical implementations and methodological expertise. It includes both a proven technical methodology for target pathway modeling and for identifying CO₂ drivers as well as software-supported solutions for measuring emissions automatically, simulating scenarios as well as for calculating the CO2 level and rebaselining.