Initial situation: internal segment accounting

Internal segment accounting provides the necessary transparency on value creation within the strategic business segments. In an environment of tight margins, declining operating profit and thus also limited retention opportunities, this is an increasingly important competitive factor. As a consequence, transparency regarding the income, expense and risk situation in the strategic business segments forms the basis for identifying levers to improve the risk/return positions.

As a rule, business segments are separately controllable, market-oriented business activities, to which expenses and income as well as capital commitment can be allocated on a cause-related basis, and which bear their own profit responsibility (e.g., retail customers, corporate customers, private banking, etc.).

According to zeb’s project experience, the setup of internal segment accounting varies considerably: while some institutions have a mature, data-based calculation approach for their strategic business segments up to assigned segments and products, other institutions struggle with issues relating to data availability or data quality as well as the choice of the right methodology.

In this context, four developments play an important role for the future of internal segment accounting in regional banks:

- Internal segment accounting as part of the measures to counter an increasing equity squeeze: Growing capital requirements, resulting from increasing credit volumes linked with rising risk-weighted assets (RWAs), tend to lead to declining capital ratios. The transparency created by internal segment accounting with regard to the RWA profitability of the business segments contributes to efficient capital management by enabling comparisons between them or by scrutinizing them individually.

- Internal segment accounting as a tool to quantify the ESG megatrend: In addition to “classic” risk-return aspects, sustainability or ESG criteria are gaining in importance. Internal segment accounting should be used to successively include ESG characteristics in business segment comparisons so as to meet the growing demands of the public, legislators, regulators, employees and customers in the environmental, social and governance areas.

- Internal segment accounting to determine the value contribution of alternative investments: As a consequence of the low interest rate environment, regional banks increasingly include alternative investments in their proprietary portfolio. Internal segment accounting provides a holistic view of their profit contribution as well as capital and risk retention.

- Internal segment accounting to implement the new risk-bearing capacity requirements: As of 2023, reporting of the economic perspective of risk-bearing capacity will become mandatory. In this context, internal segment accounting supports the implementation of the management impulses derived from the RBC also in the individual business segments.

Four hypotheses on the future of internal segment accounting can be derived from these developments:

Hypothesis 1: When measuring the performance of business segments, particular attention should be paid to RWA profitability. Banks should therefore make it their primary objective to recognize the regulatory capital costs for each business segment.

In the context of the normative perspective of risk-bearing capacity, RWAs and the equity tied up therein are increasingly becoming a management-relevant bottleneck in regional banks. This is largely due to the high credit growth, the persistent pressure on earnings and the RWA-relevant changes resulting from CRR II as well as the foreseeable changes arising from the CRR III draft.

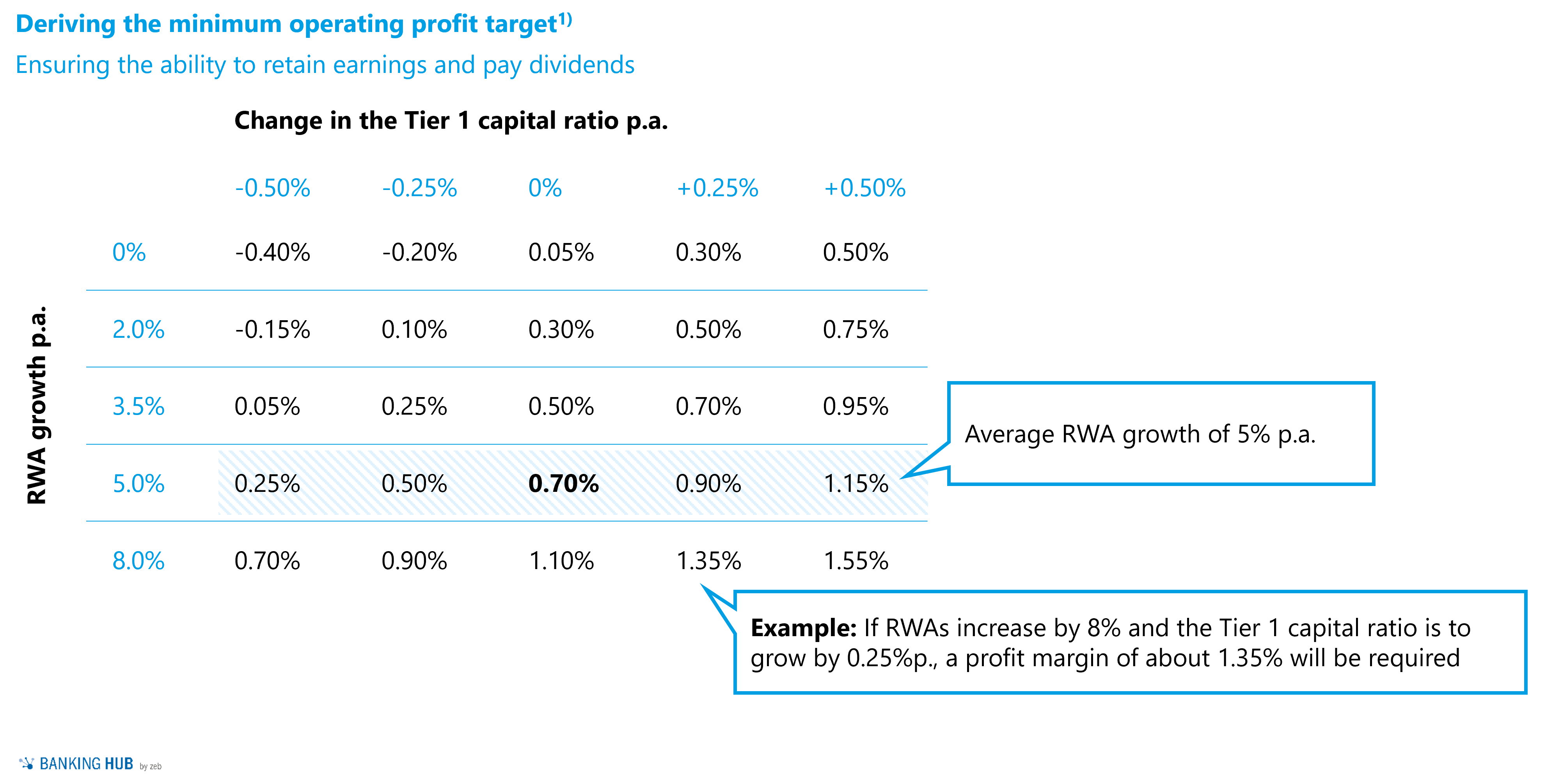

As part of the zeb.regional banking study 2021, we analyzed the pre-tax operating profit (as a percentage of the average balance sheet total) that an institution would have to generate in order to achieve the ambitious level with regard to the core capital ratio under an assumed annual RWA growth. As a result, an institution with annual RWA growth of 5% and the ambition level of maintaining a constant core capital ratio would have to generate an operating profit before taxes of at least 0.70% of their BST (see figure 1).

Figure 1: Estimated market development for digital assets in Europe and Germany

Figure 1: Estimated market development for digital assets in Europe and GermanyThis example illustrates the strategic business segments’ need for efficient RWA allocation and management in order to ensure that RWA growth “pays off” against the backdrop of the Tier 1 capital ratio ambition level. In particular, the following questions may provide guidance in allocating RWAs:

- What minimum result must the individual business segments generate, given the allocated RWA budgets, in order to ensure that the overall bank targets are met?

- Which business segments show high potential from an RWA-adjusted perspective and should be further “promoted” in the course of future allocations?

From a business perspective, strategic business segments with high potential should also be assigned appropriate RWA budgets. This allows these business segments to grow and tap the existing market potential. In addition, regulatory capital costs should be recognized at business segment level and subsequently reviewed in the business internal segment accounting.

Hypothesis 2: In the short to medium term, institutions should strive to determine an average ESG score for each business segment and identify the industries or exposures within the business segments that are particularly affected by sustainability risks. These findings can then serve as a basis for future elements of risk management – and thus also benefit the expected regulatory requirements.

The sustainability topic has become a “megatrend” in recent years and has led to a shift of social mindset. The BaFin Guidance notice on “Dealing with Sustainability Risks” published by the regulator in December 2019 already provides a framework for orientation.

The LSI survey conducted by Deutsche Bundesbank and BaFin in February/March 2022 comprehensively inquired about the current implementation status as well as the concrete implementation plans for integrating sustainability criteria into the business organization or sustainability risks into risk management. The answers had to be supported by corresponding documentation within the institutions.

The recently published recommendations of the EU expert group on the social taxonomy also show that the “ESG megatrend” will advance at a rapid pace in the future and is expected to have an impact on regional banks’ business operations.

With regard to internal segment accounting, the first relevant exercise institutions need to undertake is to identify the exposures particularly affected by sustainability risks within the loan portfolio in general or within the business segments in particular. An increasing number of institutions calculate a standardized ESG score for their strategic business segments in order to provide initial transparency regarding the general impact level.

In the regional banking sector, some group service providers have already created corresponding scoring solutions for the environmental (E), social (S) and governance (G) dimensions across the board, which will be further developed in the future, thereby keeping in line with the data and methods available on the market and the legal or regulatory requirements.

In the short to medium term, regional banks will be required to provide an overview of particularly affected exposures at both overall bank level and business segment level and to report an average ESG score.

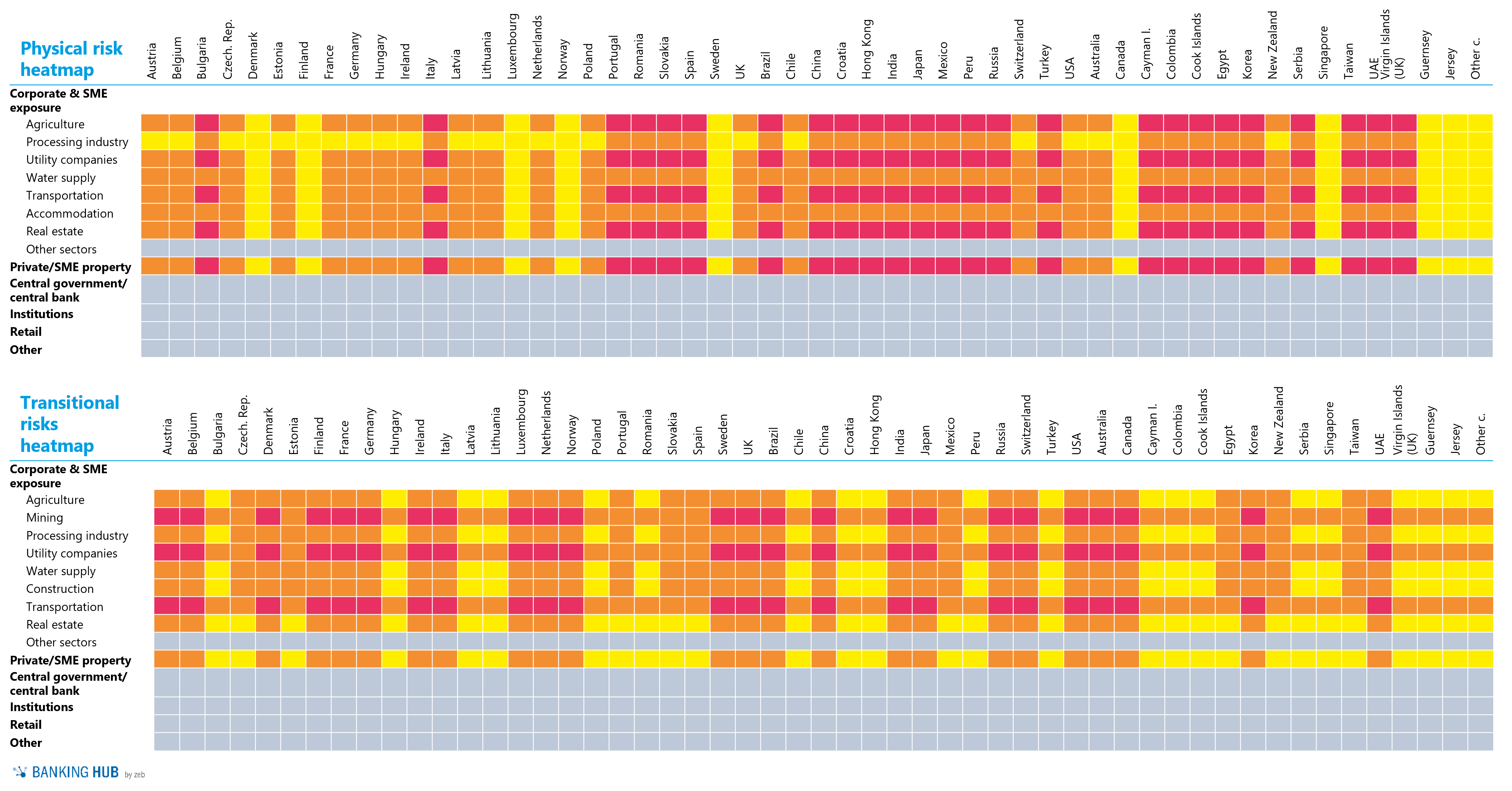

Figure 2 below shows an exemplary heat map of an ESG scoring, which differentiates between industry and country exposures. While “green scores” testify to the rather low physical or transitional risks of an industry, “yellow scores” and “red scores” indicate medium or high physical and transitional risks in the respective industry.

Figure 2: ESG scoring – exemplary heatmap on industry level

Figure 2: ESG scoring – exemplary heatmap on industry levelHypothesis 3: The rising demand for alternative sources of income or investments increases the importance of transparent internal segment accounting, thus putting “supposedly attractive business segments” to the test.

Alternative investments are those outside the category of traditional banking products. In recent years, alternative asset classes, such as real estate, ETFs, project finance (including wind farms) and private equity, have enjoyed growing popularity at regional banks as well. Institutions often see alternative assets as a valuable instrument for portfolio diversification and increasing income. The bank’s individual risk profile must, however, also be taken into account in the decision-making process (“Does the alternative investment fit in with the bank’s overall portfolio from a business strategy and risk-return perspective?“)

According to a study carried out by CFin (“Research Center for Financial Services” at Steinbeis University), just about half of all regional banks participating in the study see positive effects on the potential returns in their proprietary portfolio. Only 2 percent of the institutions surveyed said they expected negative effects on returns. Consequently, we can expect a significant increase in the portfolio share of so-called “alternatives”.[1]

Modern internal segment accounting can act as an objective instrument with which the (supposedly attractive) alternative investments can also generate an appropriate return from a risk-adjusted point of view (Return on Risk-Adjusted Capital – “RORAC”) or from a regulatory point of view (Return on Regulatory Capital – “RoReg”) and to what extent the bank’s portfolio structure is meaningfully complemented by these “alternatives”.

Under the revised Standardized Approach to Credit Risk (SACR) as part of CRR III, for example, equity investments are expected to have a new “regular” risk weight of 250% (previously: “regular” risk weight of 100%). If an institution therefore participates in a special purpose vehicle (SPV) in the course of a wind farm project financing, this alternative investment could prove worthwhile from a return perspective, but generate high regulatory capital requirements and thus become unattractive from a risk-return perspective (see also our BankingHub article on the Basel IV impact on a bank’s proprietary portfolio (currently in German only).

Hypothesis 4: Present-value impulses for new business are (once again) gaining in importance and can adequately supplement internal segment accounting.

Cross-institutional economic KPIs are gaining in importance, especially against the backdrop of the mandatory preparation of economic RBCs based on the RBC guidelines, by the beginning of 2023 at the latest[2]. In order to provide a complete view, internal segment accounting should not only refer to periodic or normative figures, but also include present-value impulses. The development of assets and also of risks could thus be reported for each business segment. On the one hand, this procedure enables an assessment of whether there is a long-term increase in assets for each business segment and to ensure that hidden reserves are not being “eaten up“; on the other hand, it would allow an integrated asset/risk view and a comparison with external market indices in the sense of risk-adjusted management.

Management impulses and conclusion

The current area of conflict between earnings and cost pressures and the increasing equity bottleneck requires regional banks to have a transparent view of the earnings and risk contributions of their business segments. Internal segment accounting can provide insights into which (growth) strategies for the business segments are target-oriented and create value in the long term against the backdrop of potential-oriented sales, regulatory developments (including the draft CRR III, ESG) and the persistently low level of interest rates.

Market developments thus provide a variety of reasons for further developing internal segment accounting to keep a finger on the pulse.