zeb.Private Banking Pricing Pulse Check

A look at the business figures of many providers of Private Banking services reveals a fairly uniform trend over the past few years: at best, constant revenues combined with significantly increasing volumes, substantially lower margins, high regulatory expenditure and profits that are characterized by positive one-off items. If there is no noticeable increase in profitability in the medium term and the current market environment continues, companies will have to ask themselves how sensible it is to keep operating.

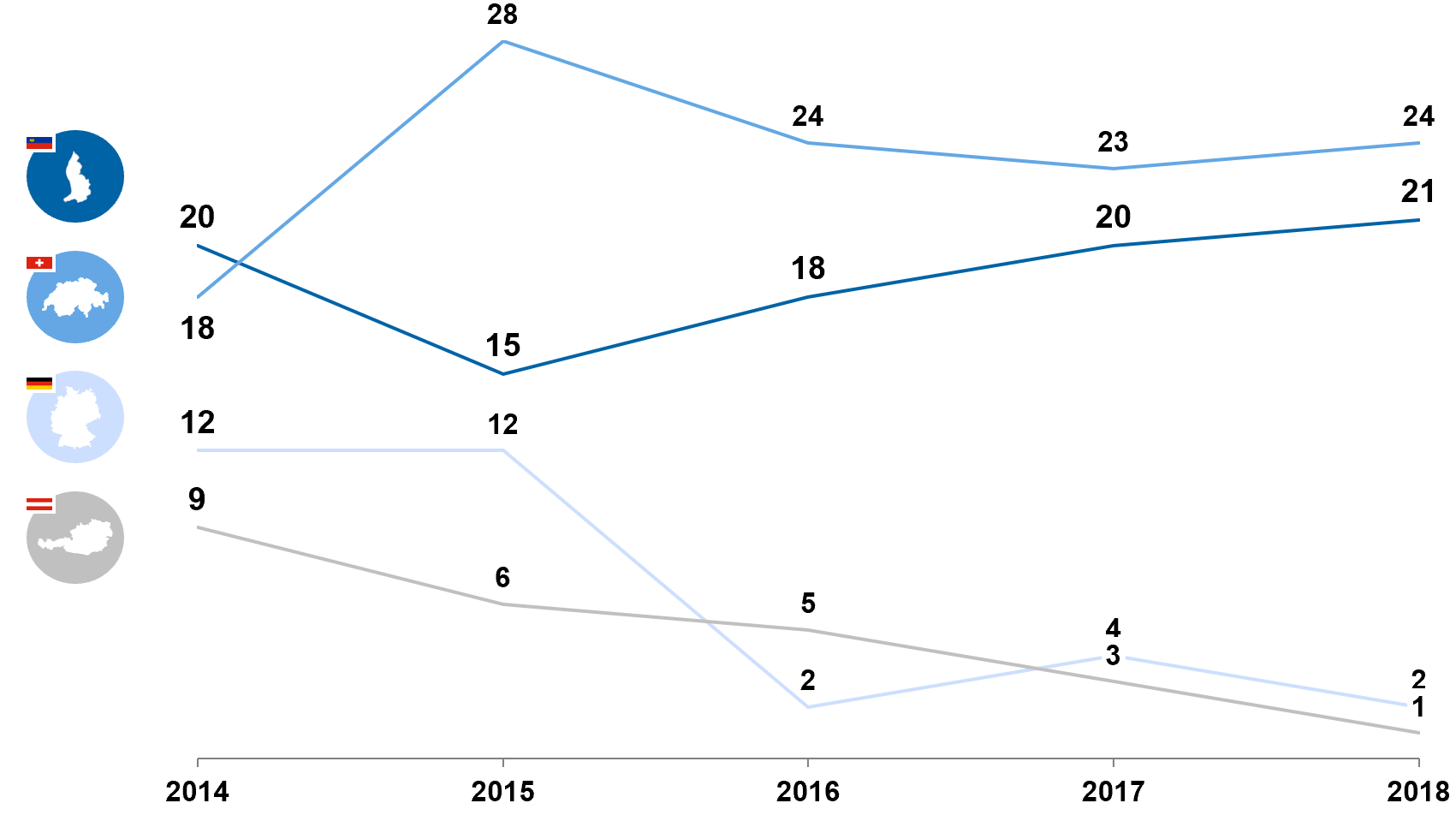

Figure 1: Comparison of operating profit margins of Private Banking providers 2014–2018 (German-speaking countries plus Liechtenstein; source: annual financial statements of the banks included in the zeb.Private Banking Studies Germany 2018 and Austria 2018)

Figure 1: Comparison of operating profit margins of Private Banking providers 2014–2018 (German-speaking countries plus Liechtenstein; source: annual financial statements of the banks included in the zeb.Private Banking Studies Germany 2018 and Austria 2018)Clients show a high willingness to pay as long as providers deliver high performance

At the same time, when asked directly in the context of anonymous interviews, Private Banking clients are indicating a high willingness to pay for high-quality, personalized services and the resulting time savings. They see the price as part of the total client care package.

If, for instance, a bank has a good, integrated package of offers and services, then a well-designed and service-oriented pricing framework provides a considerable lever for realizing earnings potentials. In addition, this can often be implemented quickly and at low investment cost within the existing organization.

Would you like a benchmarking of your pricing framework in Private Banking? You can still take part in our survey here and receive your individual copy of our study.

Participate in the pricing survey

In light of the relevance of pricing right now, zeb surveyed executives and pricing specialists at European institutions on the way they currently deal with the topic of pricing and compiled the findings in the “zeb.Private Banking Pricing Pulse Check”.

Overview of key findings

Based on the five dimensions defined in the zeb.pricing framework, the following insights can be derived:

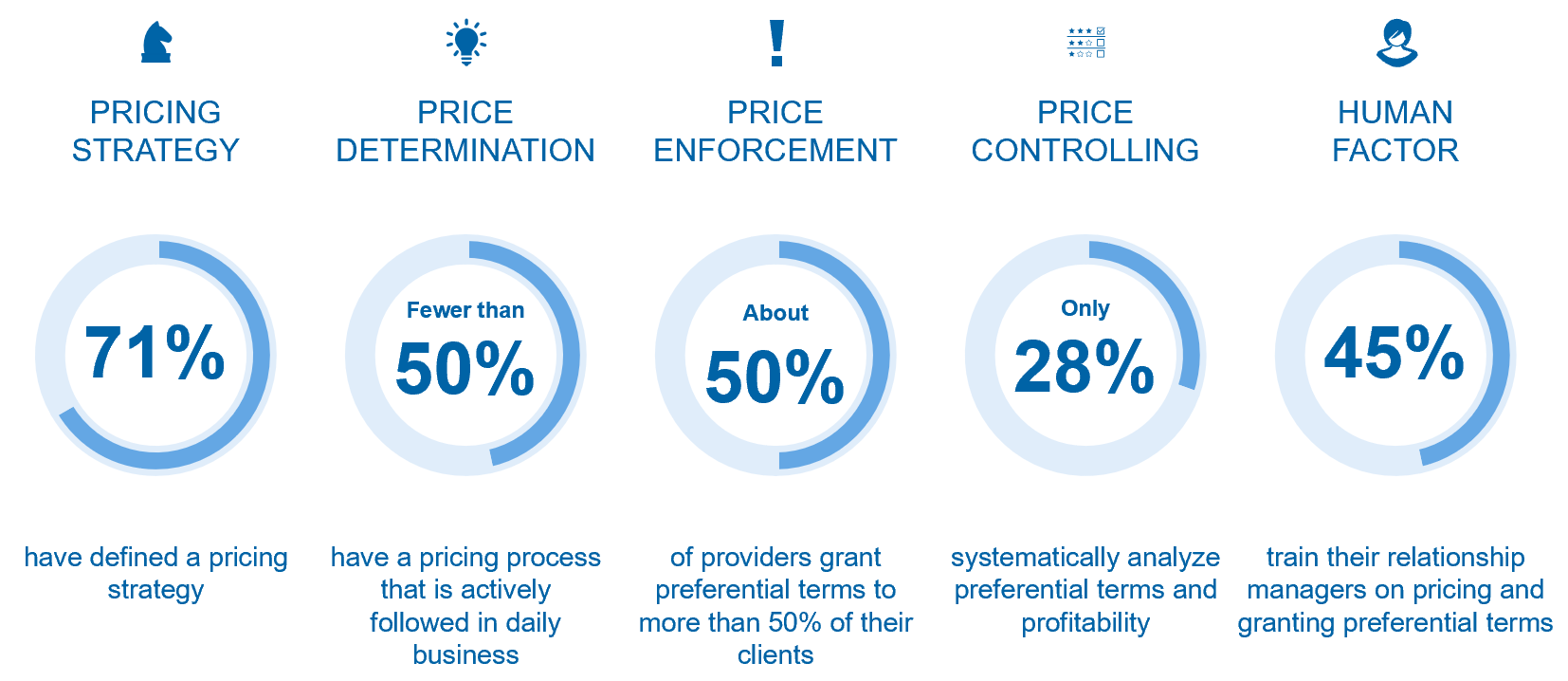

- Pricing strategy: Most banks have a defined pricing strategy, but fail to implement specific measures.

- Price determination: At half of the banks, prices are determined without any clear processes and without systematic consideration of competitors and clients’ willingness to pay.

- Price enforcement: There is a large proportion of preferential terms with mostly clearly defined granting processes—however, existing preferential terms are hardly ever analyzed and adjusted.

- Price controlling: Professional and systematic monitoring of client profitability and corresponding steering of relationship managers (RMs) are rare.

- Human factor: Regarding pricing, relationship managers are often not properly prepared and supported in their daily business through coaching and tools.

Figure 2: Key results of the study at a glance

Figure 2: Key results of the study at a glancePricing in Private Banking: need for action recognized, professionalization pending

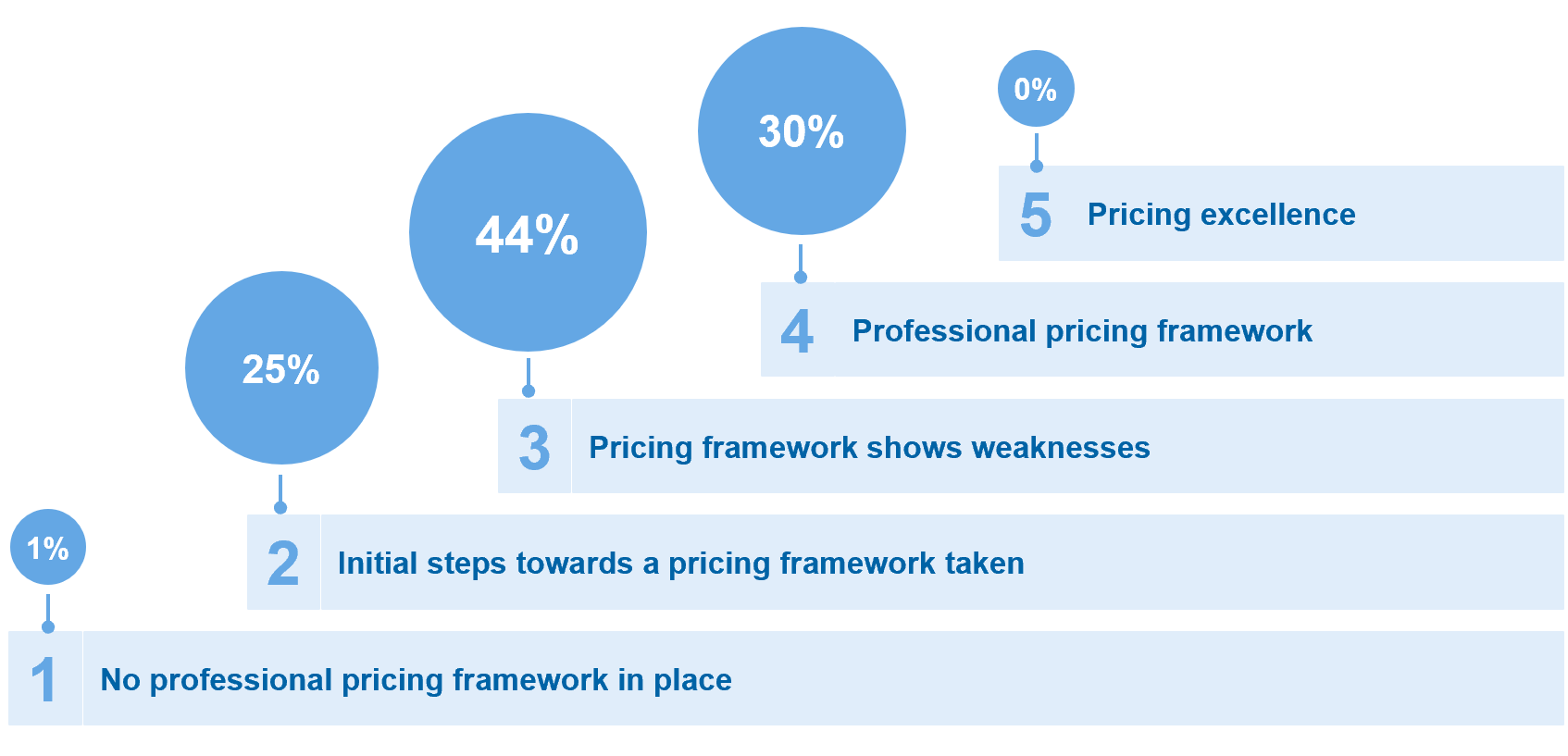

Our study shows that the participating institutions are looking at the topic, but sometimes without defining the relevant guidelines of the pricing framework and ensuring their implementation. As a result, the average maturity level across all dimensions is only in the medium range (maturity level 3 on a scale of 1 to 5), and in most institutions the existing framework shows distinct weaknesses.

Figure 3: Pricing maturity of the participating institutions (as a percentage of the total sample)

Figure 3: Pricing maturity of the participating institutions (as a percentage of the total sample)Surprisingly large weaknesses are apparent particularly in the transparency of terms and profitability as well as in managing relationship managers. Many banks lack a complete view of each client’s willingness to pay as well as the prices actually paid and their effect on the profitability of the client relationship.

Only a few institutions carry out regular analyses and adjustments of preferential terms due to the lack of transparency regarding their existence and effects. In addition, relationship managers are often insufficiently trained for their price negotiations and not given appropriate sales incentives.

In most cases, the RMs are managed by means of variable remuneration models which are limited exclusively to new business. In terms of pricing and profitability, what counts most for the relationship managers is therefore “How much do I sell” rather than “At what price do I sell”.

The lack of consideration of willingness to pay and the inadequate management of profitability and relationship managers ultimately lead to inadequate prices that cannot make a sufficient profit contribution.

At the same time, Private Banking providers put a lot of effort into acquiring new clients and generating net new money. This combination means that providers initially engage in a fierce battle for clients’ new money in order to increase their assets under management, and that in the end they lose out on profits due to weak pricing.

German banks lagging behind in European comparison—large banks at an advantage

In terms of regional performance, German banks are lagging behind their European peers. By contrast, especially institutions from the traditional offshore locations Switzerland, Luxembourg and Liechtenstein are doing much better. At the level of institution types, large/universal banks are clearly in the lead over private and regional banks. Regional banks, in particular, are still showing significant potential for improvement in the pricing of their Private Banking business.

Figure 4: Results by region and type of institution (average values)

Figure 4: Results by region and type of institution (average values)Levers for targeted improvement—managing profitability and the human factor

The results show that there is still considerable potential for professionalization in the area of pricing. The implementation of targeted measures for improvement is expected to have a high impact on returns.

Based on the findings of our study, we derive two main measures that could lead to a significant improvement in profitability in Private Banking in the short term:

1) Monitoring of client profitability and adjustment of existing terms

Realized margins can only be improved if the banks have clarity about the level of prices paid by clients after deducting discounts. Such transparency can be created, for example, by establishing a sales and pricing tool for relationship managers.

In particular, by comparing clients with similar profiles (e.g. in terms of assets, mandate type or transaction behavior), internal benchmarking can be systematically established. A dashboard visualization of overall client profitability can thus support the relationship managers in price adjustments and trigger a regular, holistic review of terms granted.

As at least a small proportion of clients are not profitable in most banks, such a dashboard allows further transparency to be created in order to address these clients specifically (e.g. through systematic repricing, the introduction of minimum fees or migration to a more suitable service offering). This could also reveal, among other things, that the current product range and pricing models do not meet client needs.

2) Negotiation coaching and incentive-based steering

The relationship manager remains the biggest driver in price enforcement. Experience shows that preferential terms can vary greatly among RMs in the same bank.

It is therefore important to manage the RMs through an incentive-based variable remuneration system, which should take the following three aspects into account: a) the growth dynamics (e.g. in the form of net new money inflow), b) the quality of growth (e.g. via the prices enforced) and finally c) client satisfaction.

In addition, targeted price coaching can lead to a noticeable change in behavior and thus to a measurable improvement in price enforcement. A successful empowerment concept is characterized by the fact that it not only leads to a better understanding of the products and prices on the part of the relationship manager, but also to the consideration of the profitability aspect in the client relationship being permanently internalized.

Ideally, price becomes a secondary factor due to the high-quality, individual client support and the resulting time savings for the client.

Conclusion—Private Banking Pricing Study

Our Pulse Check shows that although many institutions have defined processes relevant to pricing, these processes are often only used to a limited extent in daily operations. The margin improvements institutions hope to achieve through price adjustments can only be realized if the framework is also systematically improved at the same time.

Targeted measures such as quick-win actions in relation to pricing, sales tools or coaching, enable comparatively rapid improvements, which, according to our project experience, immediately translate into increased profitability.

Further information about the Private Banking Pricing Pulse Check can be found here.