What does the current market and competitive environment for banks look like?

Market environment

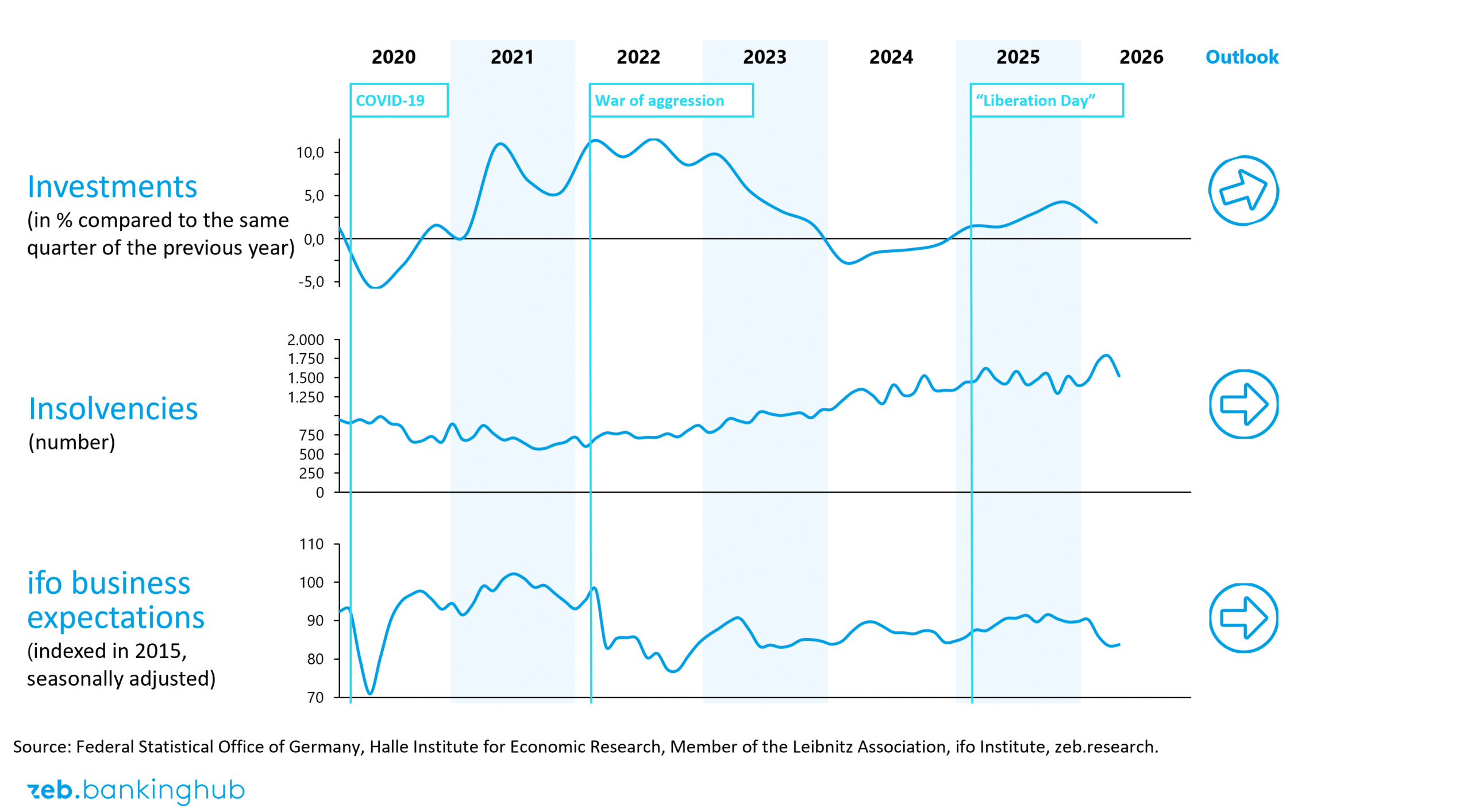

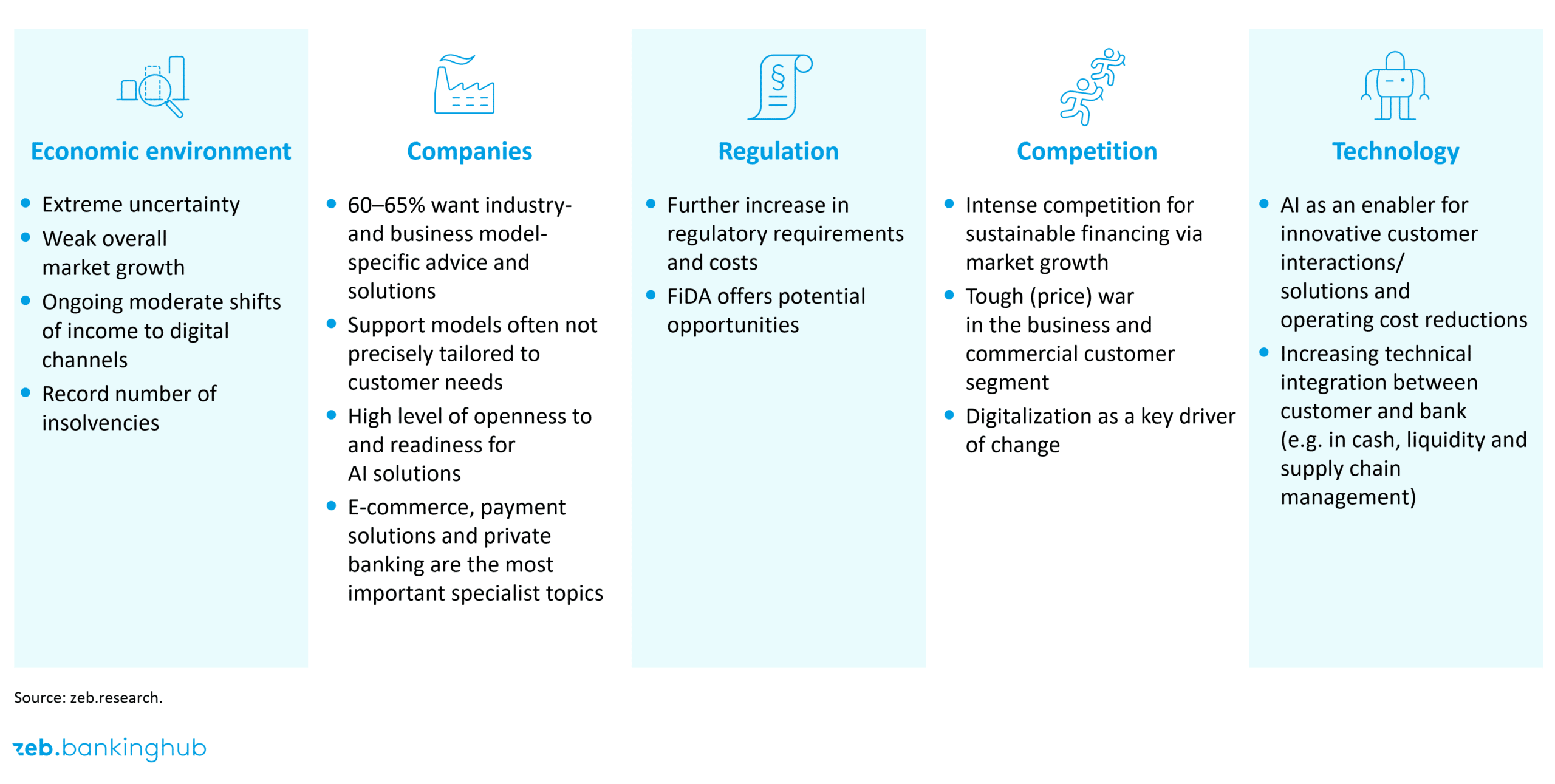

The German economy is experiencing a severe crisis; never before in the history of the Federal Republic has a recession lasted as long as the current one. In addition to structural problems such as the shortage of skilled workers and excessive bureaucracy, companies are struggling with a high level of uncertainty as to the prevailing economic policy, which is further weakening the export-oriented economy.

As a result, the situation for businesses is extremely difficult: hardly any investment growth, but insolvency figures at record levels. Banks are reacting to the corresponding increase in non-performing loans by being much more cautious in their lending. Small and medium-sized enterprises in particular are feeling the effects: more than a third of them have rated bank lending as restrictive.

Competitive environment

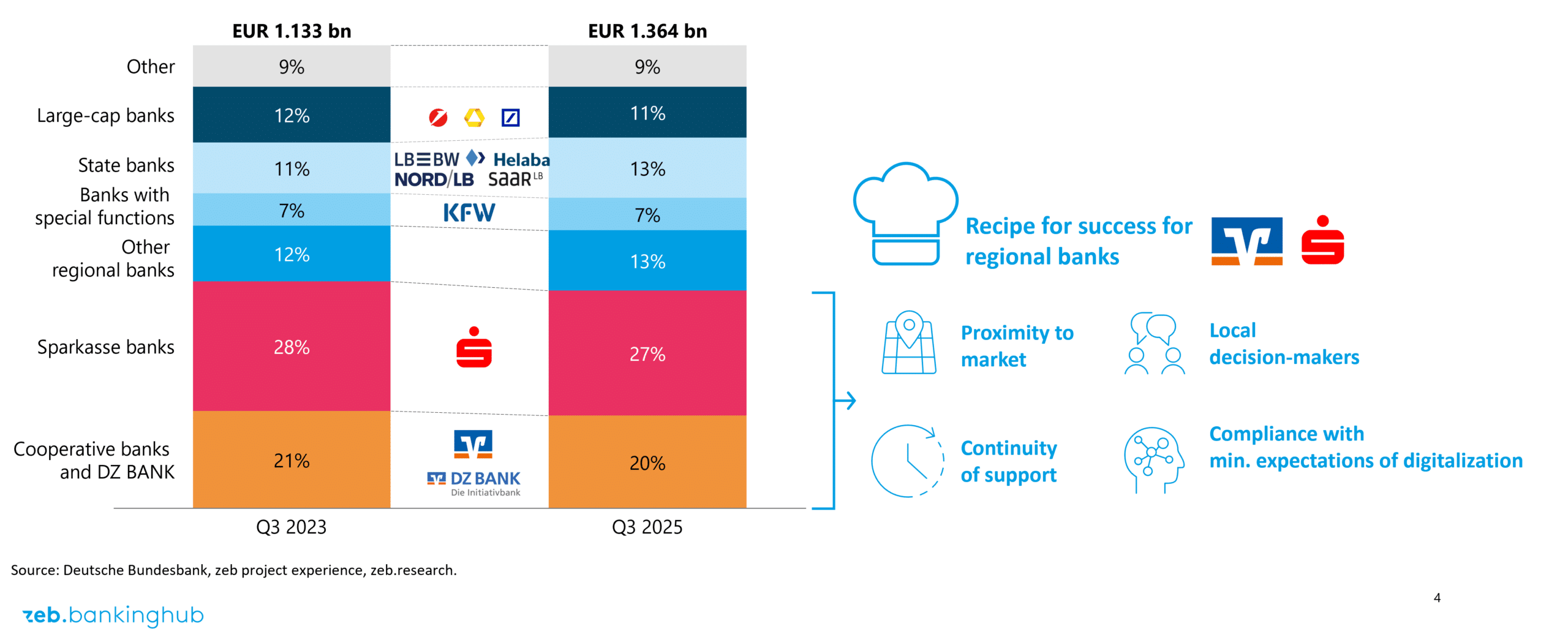

Banks’ income potential is also expected to grow only moderately in the coming years. The zeb.CC wallet model forecasts income potential of EUR 61 billion for 2030 with annual growth of around 2.1%. In this market that lacks any noticeable growth momentum, competition between banks is intensifying – the regional banks of the two network organizations (Savings Banks Finance Group and Cooperative Financial Network) have been able to hold their own in the market in the past thanks to their proximity to the market, continuity of support and local decision-makers.

However, banks need to catch up on a huge backlog when it comes to meeting minimum digital standards, which will increase ever more rapidly as the importance of artificial intelligence grows. In the lower corporate banking segments in particular, more and more digital players are entering the market, continuously taking market share from the established banks, albeit on a rather small scale.

A particularly fierce battle for market share is also emerging in the sustainable financing segment. While the share of sustainable financing in new business will be around 9% in 2027, financial institutions have set targets that go well beyond the forecast market growth (savings banks, for example, are aiming for a 20% share of green financing in new business, while cooperative banks are striving for 19.6%).

What do corporate customers expect and what do (or should) banks provide?

Against this backdrop, we surveyed 400 companies of all sizes and industries in Germany as well as 82 regional banks in order to compare the expectations of corporate customers with the regional banks’ offers and assessments. In this section, we present a selection of the key findings from our survey.

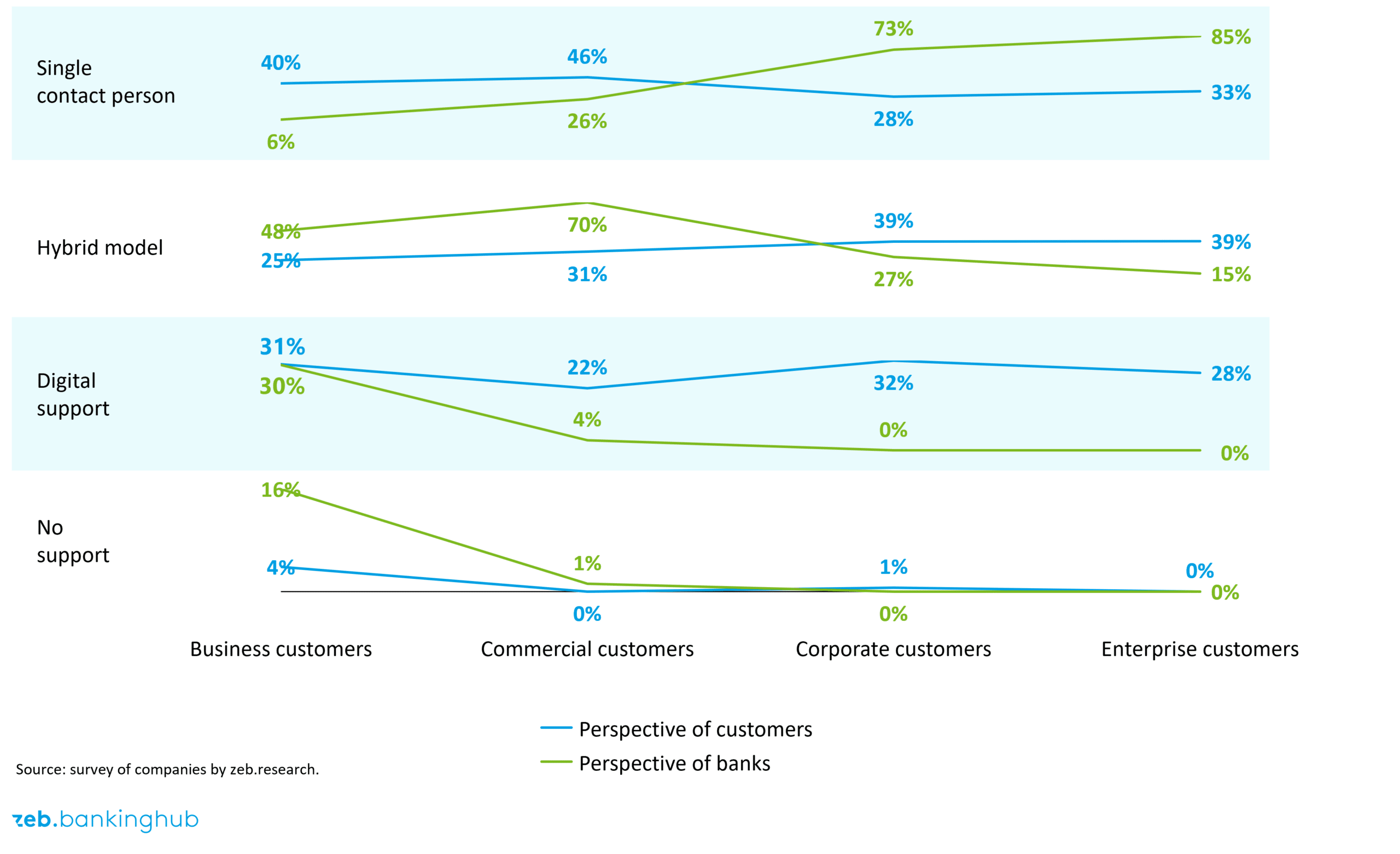

Banks underestimate the potential of digital support

A comparison of how banks and companies assess support options shows that banks often misjudge the preferred service model in the various corporate customer segments: almost all corporate customers wish for a support model that is more digital than the banks assume.

In particular, banks underestimate the openness to digital and hybrid support for large companies and the importance of personal support for smaller business customers and tradespeople. The majority of the companies surveyed would also like to see additional digital services, for example in the areas of financing and automation. For banks this means that digitalization helps them increase customer satisfaction and save costs at the same time.

Corporate customers expect more specific expertise

The survey of companies underlines the relevance of specialist knowledge as a differentiating factor in the competitive landscape: 60% of companies want their bank to have industry expertise, 65% also require business model-specific know-how. However, this requirement is not easy to meet, especially for smaller banks.

On average, the cooperative banks surveyed hold two sales units for specific target groups, while the savings banks have three. Another obstacle on the way to becoming a competent sparring partner is customer segmentation: a large proportion of the banks surveyed have assigned more than 20% of their customers to the wrong segment.

Artificial intelligence holds great potential

The companies surveyed believe that artificial intelligence holds great potential, be it for service and process issues or for customer advisory services.

Interestingly, corporate customers rate the potential of AI as particularly high. As in the case of digital support models, banks also see the potential for using AI, but they consistently attach less importance to it than their corporate customers.

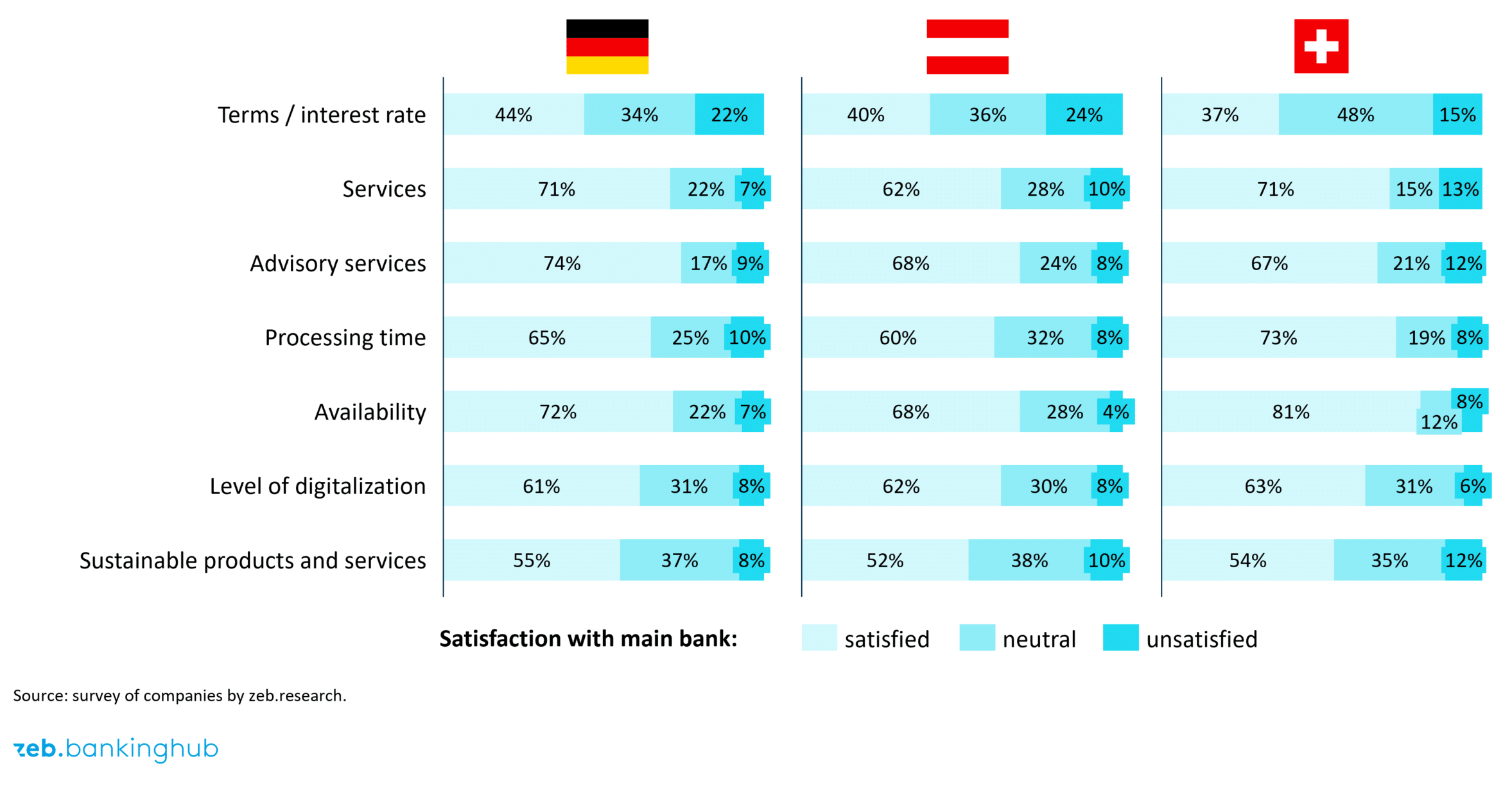

Excursus: comparing DACH countries

Not only German, but also Austrian and Swiss companies and banks were surveyed in this year’s Corporate Banking Study. This also allows a comparison of the countries in the DACH region. Our findings reveal that customer satisfaction differs along various dimensions.

Figure 4: Country-specific comparison of customer satisfaction

Figure 4: Country-specific comparison of customer satisfactionIt is noticeable that Swiss banks are leaders in most price and service areas. Overall, customer satisfaction is lowest in the dimensions “Terms”, “Sustainable products” and “Digitalization”.

Looking ahead: what action should banks take?

Numerous drivers of change are shaping an environment for banks that is becoming increasingly uncertain, volatile and complex. At the same time, there is still a need for genuine advice and proximity. In order to remain successful in this field of tension, banks must integrate themselves into the reality of their customers. We have identified three key fields of action for this purpose:

- From replaceable provider to relevant sparring partner: In a challenging economic environment, companies are under massive pressure to make decisions, so they need partners who provide guidance and impetus. To fully assume this role, banks must provide in-depth understanding of industries and business models and use their specialist knowledge to navigate corporate customers.

- Building infrastructure that starts with the customer, not the bank: Corporate customers expect solutions that can be seamlessly integrated into their business reality: Embedded finance, AI agents and self-services are not only relevant in the future, but are already mandatory today. At the same time, these applications give banks access to new data and sales channels.

- Mastering the internal transformation: Being able to act as a competent sparring partner to customers and to integrate seamlessly into their day-to-day business requires an excellent operating model set-up. What is needed is an orchestration model that considers and manages income, risk, costs, capacities, greenhouse gas emissions and equity as a whole.

Only those banks that accept these challenges have a good chance of continuing to be successful partners for companies.