What are climate risks and what types of climate risks can be analyzed?

Climate risks are potential negative effects of climate change or the adaptation thereto. A distinction is made between physical and transitory risks.

While physical risks result from natural events, transitory risks are caused by various factors such as political, technological or market-driven changes.

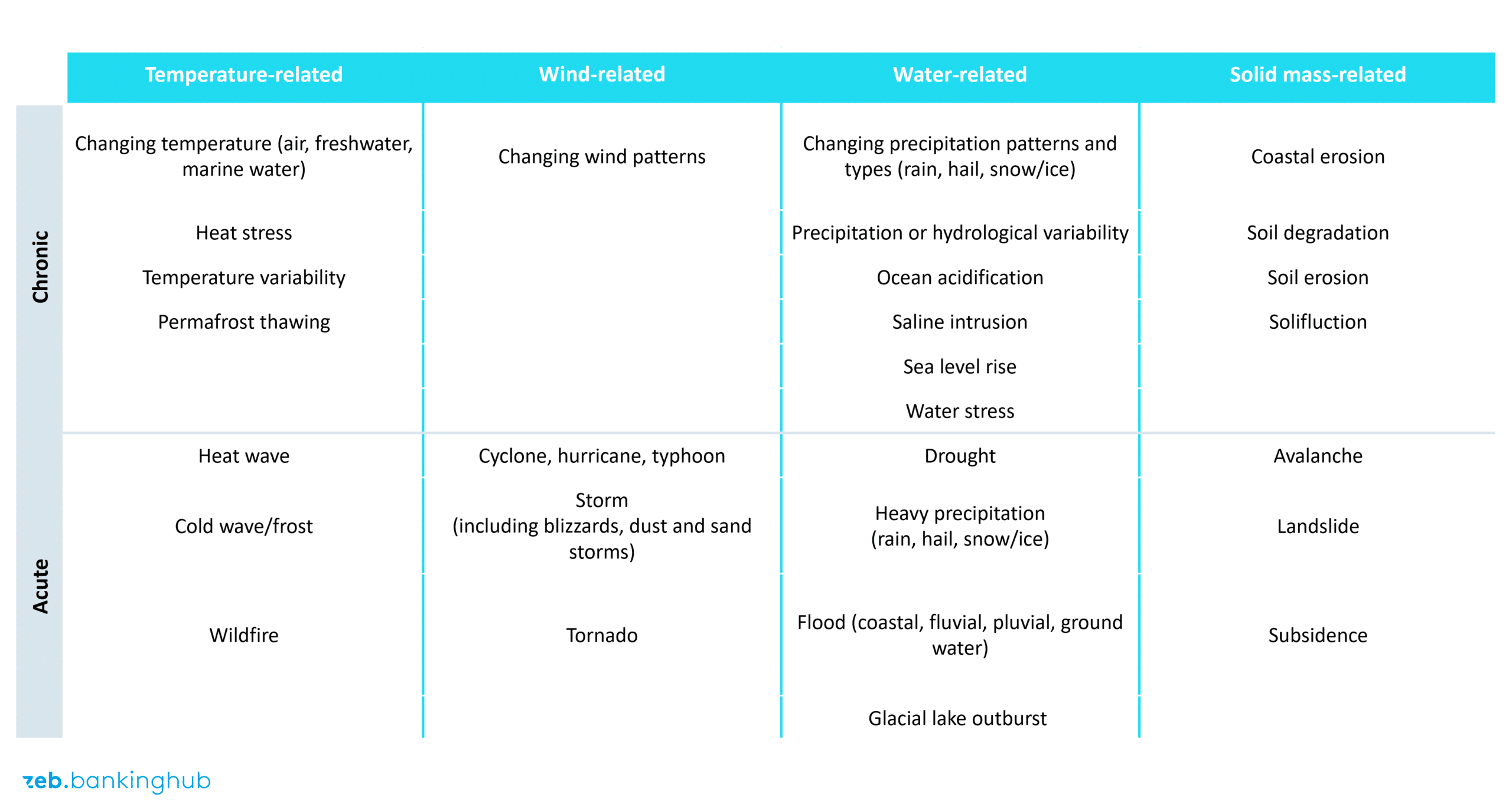

In this article, the focus is on physical risks, which include not only extreme weather events (acute climate risks) but also slowly occurring climate-induced changes (chronic climate risks).

Financial institutions are affected by climate risks both directly and indirectly, i.e. through their credit and investment portfolios. One example of direct risks is the flooding of offices and branches, which can result in physical damage and business interruptions. Indirect risks may, for instance, arise from extreme droughts leading to crop failure and thus loan defaults at agricultural businesses in the affected region that are part of the bank’s sub-portfolio. Another example would be a drop in value of real estate collateral due to extreme weather events such as flooding.

Climate risk analysis is a systematic process for identifying and assessing the potential impact of climate risks. It is a tool for banks to assess the vulnerability of various economic activities to natural disasters. As such, it provides a sound basis for decision-making in the context of strategic adaptation to climate change and sustainable transformation.

Which three key questions need to be considered when implementing climate risk analysis?

Question 1: Why do we need climate risk analyses?

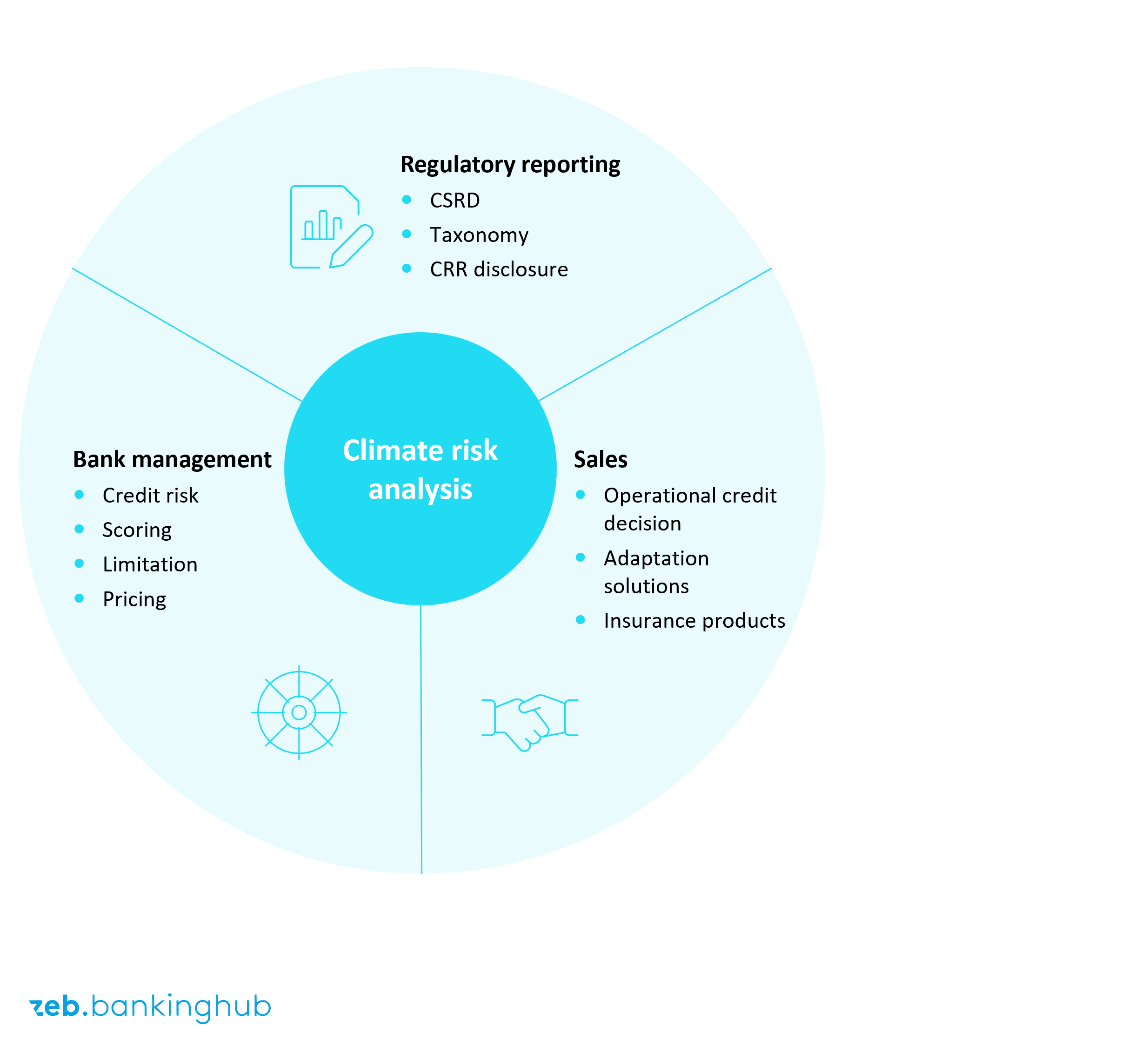

Banks apply climate risk analyses in different contexts – primarily for reporting, management and sales purposes.

Reporting: information on climate risks are required by regulation as part of non-financial CSRD reporting, taxonomy reporting or CRR disclosures. For institutions that are subject to CSRD reporting obligations, ESRS E1 mandates disclosures on climate risks.

For financing decisions with known use of funds to be considered green under the EU taxonomy, a review of climate risks is required. To this end, the taxonomy provides a standardized annex including an overview of the climate risks to be analyzed for the financed property or activity.[1]

Disclosure reports pursuant to the CRR require the disclosure of climate risks in a standardized form.[2] For one thing, they must be taken into account as risk drivers of the relevant risk types included in the existing disclosures, such as credit default risks. For another, in the separate section on ESG risks, qualitative and quantitative information on physical climate risks in the investment book must also be provided.[3]

In addition to mandatory regulatory reporting, climate risk analyses can also be used for reporting pursuant to voluntary standards. For example, the Equator Principles require the implementation and reporting of an environmental and social assessment, which also includes climate risks.[4]

Bank management: climate risks are covered by regulations such as MaRisk or the EBA Guidelines on loan origination and monitoring (GLOM) as well as the new EBA Guidelines on the management of ESG risks. Banks must take them into account as part of their ESG risk assessments when granting loans as well as in ex‑ante management, pricing, scoring, limiting and limit monitoring. This requires a quantitative assessment of climate risks in lending to corporate customers and the valuation of collateral for real estate loans. Climate risks must also be included in the risk inventory and in portfolio risk management as drivers of credit default, market or operational risk.

Sales: climate risks of financed properties and customers must also be taken into account when making operational lending decisions. They can be decisive in determining whether and under what conditions an individual loan is approved. In this context, climate risks might also open up new business opportunities and become a potential conversation starter for customer advisors. The identification of relevant physical climate risks for mortgage customers can serve as an upselling opportunity as those customers may need additional funding for climate-related modifications to their properties or building insurance.

Question 2: What are the relevant standards and requirements for climate risk analyses?

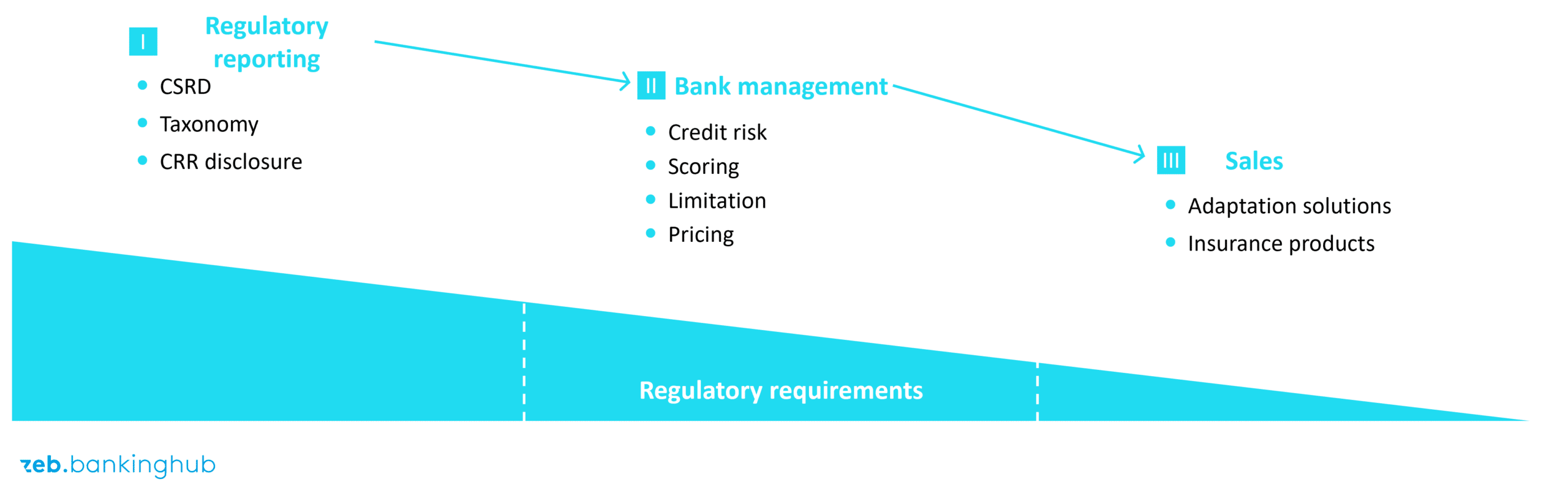

The requirements for climate risk analyses vary depending on the area of application. The lower the level of detail, the greater the scope for custom implementation.

Reporting in particular is subject to detailed regulatory provisions and requires a robust climate risk and vulnerability analysis (CRVA) based on scientific standards[5].

Three key features must be taken into account:

- Climate risks: All risks relevant to the respective business model must be selected from the list of potential climate risks (see Figure 1). Exclusions of risk types due to geographical significance or lack of business relevance must be comprehensibly justified.

- Lifetime: The data to be used for climate risk analysis depends on the lifetime of the economic activity. For economic activities with a lifetime of less than ten years, historical data is used, while those with a lifetime of more than ten years require model projections. There are no binding regulatory requirements for determining the lifetime.

- Scenarios: For businesses with a lifetime of more than ten years, GHG transition pathways must be selected that reflect potential global warming. The selection of scenarios is the responsibility of the banks and is based on the specifications of the Intergovernmental Panel on Climate Change (IPCC), in particular the Representative Concentration Pathways (RCPs). RCP 8.5 (or SSP5-8.5) is currently considered the most relevant scenario (worst case).

In the context of bank management, the new EBA guidelines (EBA/GL/2025/01) supplement the existing requirements of the 7th MaRisk amendment. Climate risks – as a subcategory of ESG risks – are an integral component of banks’ overall risk assessment. Climate risk analyses are relevant for several areas of bank management. In the first step, the analyses serve to identify the bank’s key climate risks as part of the materiality analysis. In the second step – the risk measurement – these key climate risks are quantified via climate stress tests and a climate resilience analysis. Finally, the derived key figures can be used for action-based risk management.

Climate stress tests are used to assess the financial resilience of a bank. For key climate risks, the scenario-based climate risk analysis is carried out with a time horizon of less than five years. The scenarios include a base scenario and several adverse scenarios, whereby climate-sensitive variables (e.g. CO2 price, defaults due to extreme weather events) must also be taken into account. Climate risks influence the default probabilities of loans and should be considered in pricing as well as risk limitation – both at individual business level (interest rate, probability of default) and at portfolio level (value at risk, loss given default).

The climate resilience analysis pursuant to the new EBA guidelines, is used to assess the resilience of the business model. Regulators require that the climate risk analysis be carried out for long time horizons of at least ten years and for several scenarios, including a central scenario (the most likely one) and other long-term scenarios. Sector-specific developments and transition plans of important counterparties must be included in these analyses in order to assess the impact of climate risks on future profitability and risk exposure.

The sales perspective is concerned with reducing the financial impact of climate risks. One way to achieve this is to insure one or more climate risks, which transfers the financial risk to the insurance company. Another option is to implement climate adaptation measures that reduce the financial risk of extreme weather events. From a sales perspective, the bank has the lowest level of regulation and the greatest scope for action.

Question 3: What are the biggest challenges when it comes to analyzing climate risks?

The implementation of climate risk analyses in banks is by no means a trivial matter.

Different levels of requirements

The different requirements and regulatory specifications described under question 2 make it difficult to develop a standardized approach for implementing the CRVA within the bank, especially when multiple use cases have to be considered.

Data availability

Large amounts of data are required to carry out climate risk analyses. However, the availability of reliable, location-specific climate data is currently still limited. For one thing, the necessary climate data is completely lacking for certain product types, risk types and time horizons. For another, the available data has an uneven granularity and is sometimes inconsistent in terms of its accuracy. The bank must therefore decide on a way to deal with missing or inaccurate data. However, on a positive note, the overall data availability is continuously – albeit slowly – increasing.

Risk definition

There are no uniform thresholds for when a climate risk can be classified as “material”. Definitions vary depending on the industry, region and regulator. A one-size-fits-all approach is therefore not feasible, and the bank must decide independently how to categorize the extent of the respective climate risks in a meaningful way.

A particular challenge lies in the spatial localization of risks: While the location of real estate can be clearly determined, this is significantly more difficult for movables such as vehicles.

Choice of RCP scenarios

In climate risk analyses, issues are also assessed using the RCP scenarios. A lack of regulatory requirements for scenario selection, the regular development of new RCP scenarios and long-term climate projections with a high degree of uncertainty impair the comparability and resilience of climate risk analyses.

Integration into risk management

The results of climate risk analysis must be integrated into existing risk and control systems. This requires not only technical interfaces, but also new organizational approaches and clear responsibilities. The results of the climate risk analysis must be converted into risk variables (e.g. probability of default, loss given default) for this integration.

What requirements should banks observe in order to successfully implement the climate risk analysis?

Banks should systematically and holistically assess the requirements and earnings potential of climate risk analysis. Subject-matter knowledge and expertise are essential for successful implementation. It is important to create a consistent database and establish effective recording capabilities. Usually, banks outsource the location-specific modeling of climate risks to an external provider. A clear procedural and organizational structure ensures transparent responsibilities and smooth processes. The targeted development of expertise among employees is essential for the comprehensive identification and management of climate risks.

As the significance of climate risks can be expected to increase further in the future, banks should see the information obtained not only as a challenge, but also as an opportunity – for example for sales or for innovations that promote sustainable growth and future viability.