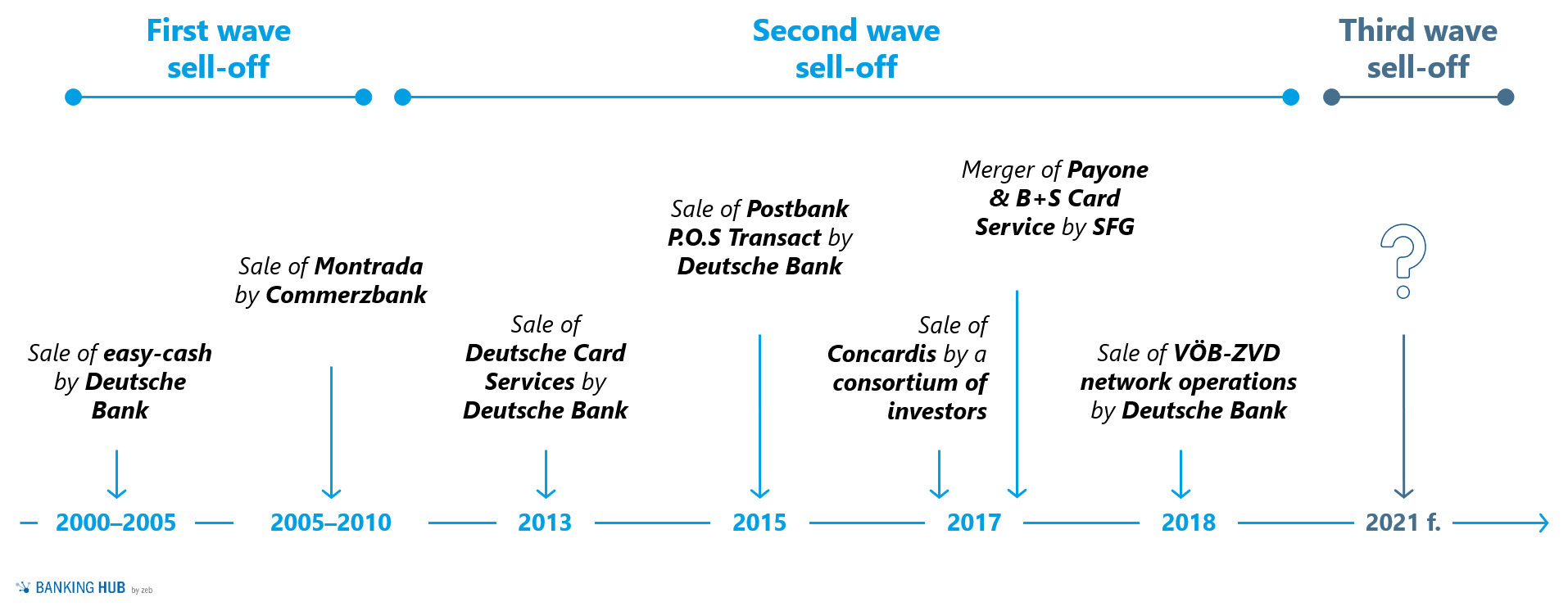

Payment market Germany: Consolidation Trends

Over a long period of time, only the Genossenschaftliche FinanzGruppe (Cooperative Financial Network) and the Sparkassen-Finanzgruppe (Savings Banks Finance Group) in Germany maintained significant payment service providers of their own.[1] Nevertheless, even these institutions showed tendencies towards consolidation[2]: taking Payone as an example, the Deutsche Sparkassenverlag (German Savings Banks Publishing House) entered into a joint venture with the French payment service provider Ingenico in July 2018. After withdrawing from merchant payment processing, Deutsche Bank recently bucked the trend by announcing that it would once again offer payment solutions for merchants, and is even contemplating a possible takeover.

Figure 1: Exemplary M&A activities of German banks in the payment market

Figure 1: Exemplary M&A activities of German banks in the payment marketA bank’s payment transaction activities especially comprise the provision of account infrastructure, the distribution of debit and credit cards, the processing of paper-based payment transactions, and cost-intensive cash handling.[3] Since 2018, the introduction of instant payments has prompted many German banks (including Deutsche Bank, Commerzbank, HypoVereinsbank, Sparkassen, and many Volksbank/Raiffeisenbank institutions) to start tapping additional revenue potential by charging fees for real-time transfers.

The ongoing coronavirus pandemic has greatly changed payment behavior, above all among private individuals. As more and more people shop online from home, digital payment methods such as PayPal continue to gain momentum. In addition, contactless or mobile payments are increasingly used for purchases at local stores to reduce the risk of infection. While cash supply and physical PoS transactions are losing in importance, there is a significant boost in the use of digitally processed payments triggered by the coronavirus pandemic. This trend calls for the expansion of suitable offerings and infrastructure.

Banks mostly incorporate third-party solutions for mobile and contactless payments. In this context, Apple Pay and Google Pay are in direct competition with the German banking industry’s “girocard”. Another option is to integrate digital or virtual credit cards from payment service providers such as PayPal. Volksbank and Raiffeisenbank institutions were the last major German banking group to introduce Apple Pay in April 2020.

Banks and their business and retail customers rely on external payment service providers, such as VISA, Mastercard, Ingenico, Concardis, PayPal, and others. This article aims to explore the shift in the existing balance of power and the strategic options available to banks.

The rise of payment providers

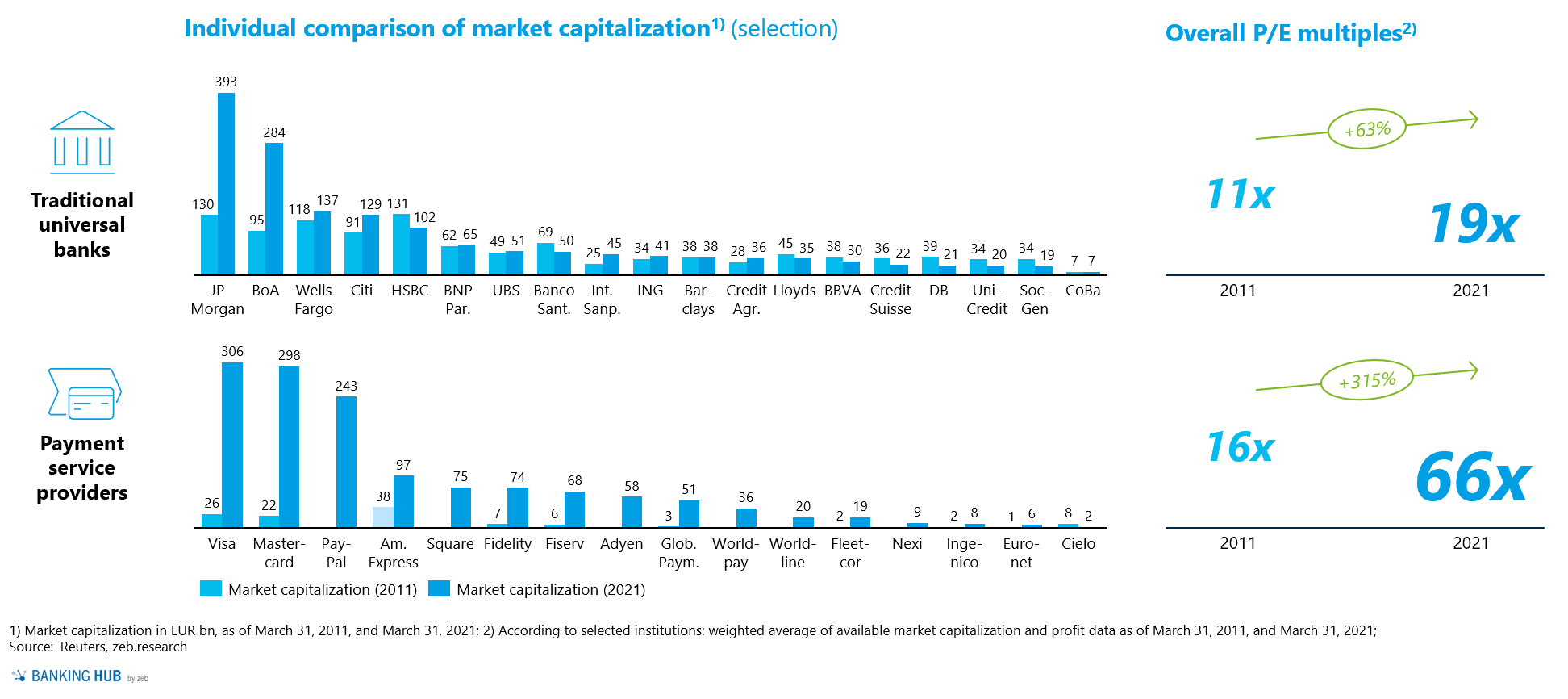

Due to strong growth in recent years (in terms of market valuation), international payment service providers now increasingly play in the same league as traditional major banks. The Swedish payment provider Klarna, for example, recently tripled its valuation to USD 31 billion (around EUR 26.2 billion) and is now considered the most valuable private start-up in Europe. With the exception of U.S. banks, most banks have only just managed to maintain their market capitalization at a constant level over the past ten years, if at all. Measured in terms of pure price-to-earnings multiples, it is also evident that investors place significantly more trust in the future expansion of income from the payment services provided by fintech companies than by banks.

Figure 2: Market capitalization and P/E multiples of selected banks and payment service providers

Figure 2: Market capitalization and P/E multiples of selected banks and payment service providersIn terms of market capitalization, VISA, Mastercard, and PayPal are at least on a par with the largest U.S. banks and are therefore significantly better valued on the market than all European banks. PayPal, for example, boasts a price-earnings multiple of 68.6 as of March 1, 2021, whereas the price-earnings multiple of ING, a prominent European bank with a high digital affinity, amounts to a mere 16.4. Furthermore, PayPal reports having almost 30 million users in Germany[4] – and thus more customers than Deutsche Bank. Contrary to the market position expected from its high media presence, PayPal’s share of European payment transactions is less than 1% – which clearly indicates growth potential in this line of business.

Meanwhile, the payment service providers’ dependence on banks is declining. Technological and regulatory (e.g., e-money) developments increasingly enable payments that do not require the integration of traditional bank accounts and physically issued payment cards. Some large payment service providers, such as PayPal and Klarna, hold EU-wide banking licenses of their own and are therefore able to offer other banking services in addition to payments. PayPal USA already provides this service through cooperations with banks that remain in the background.[5] Klarna now also offers credit to online merchants.[6] The payment service providers consistently exploit the opportunity to grow along their payment processes in the traditionally high-margin consumer finance business of banks.

When it comes to payments, the banks’ ability to innovate tends to lag behind large Internet and tech companies. For the most part, banks limit themselves to providing the technical infrastructure. Trend topics, such as blockchain and cryptocurrencies, also create further shifts. Payments do not necessarily require a bank’s infrastructure. In addition to fintech companies, Internet giants such as Facebook also position themselves in these areas. PayPal, for example, underpins its ambitions in the field of cryptocurrencies with its recent acquisition of the Israeli crypto manager Curv, thereby buying expertise in the safekeeping of digital assets.[7]

As payment service providers grow and gain in importance, and competition from outside the financial services industry intensifies, it is imperative that banks position themselves strategically with regard to payments.

Evaluation of the observed market movements

Outsourcing the technical infrastructure is a common and advisable step toward further industrialization in order to leverage efficiency advantages through economies of scale and thus enable low-cost payment transactions. The consolidation of service providers supports efficiency gains and is therefore generally welcomed.

Outsourcing product areas, however, means that banks are giving away business, since the outsourcing process also involves the transfer of customer data. Banks are currently neglecting the resulting risk of losing customers on the merchant side. Driven by the current low interest rate environment, they tend to focus instead on short-term cost advantages, thereby jeopardizing a strategic source of income.

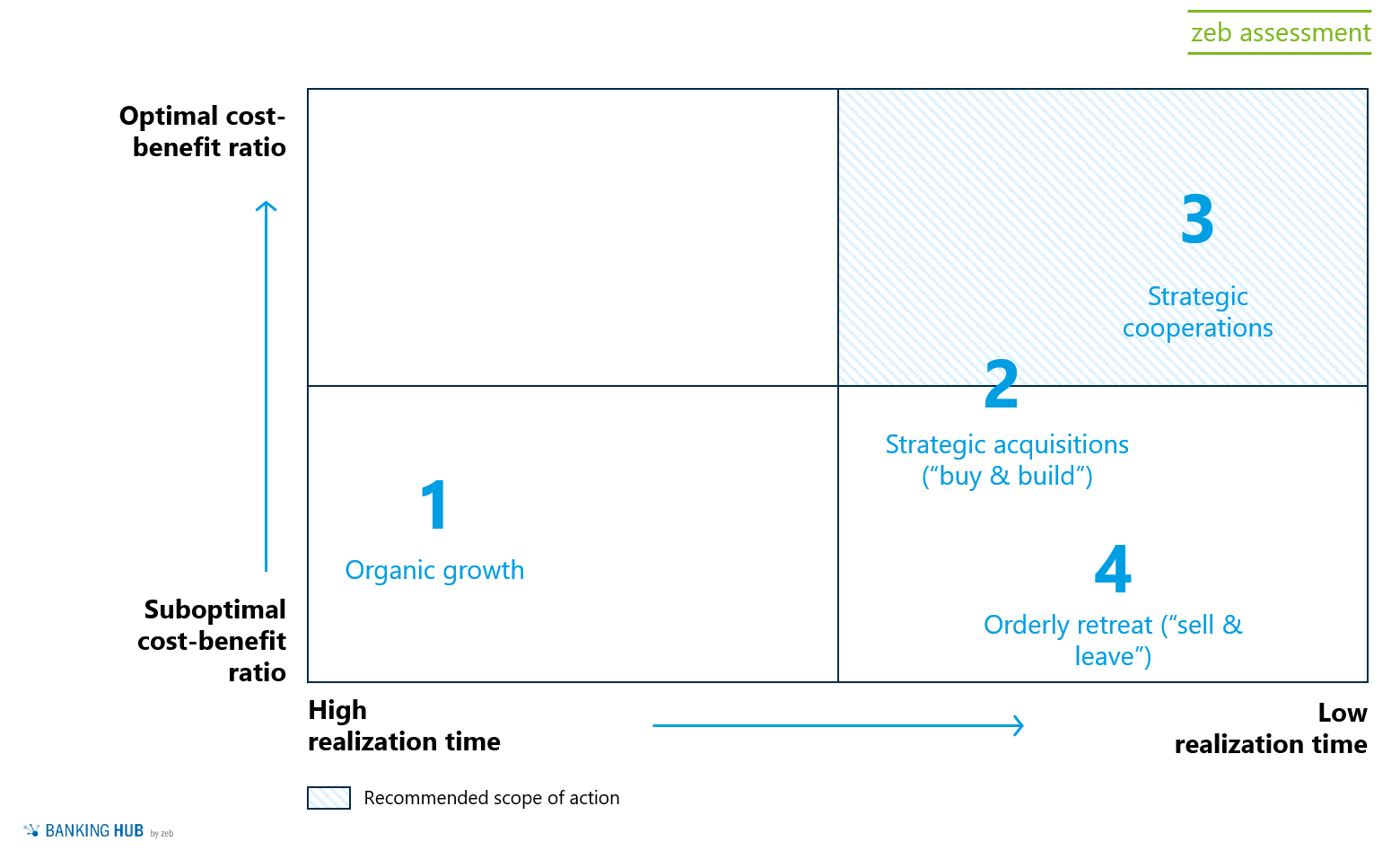

Four strategic options for banks

zeb has identified four strategic options to respond to the developments in the payments industry:

1. Organic growth

Banks can further develop their current offerings and/or build new solutions on their own. This allows them to avoid dependencies and retain full control over customer access. At the same time, it enables them to better utilize existing internal resources. Organic growth, however, entails comparatively long development times and relatively high investment costs. This only pays off in fields in which the bank can expand an existing base and/or which offer real opportunities with high growth rates.

One example is DZ Bank, which, according to press reports, intends to build its own payments platform for SEPA, instant payments, and foreign transfers together with Fiducia & GAD by 2023.[8]

2. Strategic acquisitions (“buy and build”)

Aside from the in-house development of services, strategic acquisitions are also an option. The purchase of an established payment provider enables subsequent integration in various expansion stages (subsidiary in the group up to full integration) and further development of its innovative and already tried-and-tested solution. M&A activities can thus be used to acquire complementary technologies and expertise. This, however, requires large investments, since specialized payment providers – as previously shown – are often expensive. In addition, it is important not to curb the innovative ability of the acquired company through corporate structures.

Individual banks use strategic acquisitions to expand their payment offerings. In 2016, for example, Banco Santander’s Brazilian subsidiary bought the fintech startup ContaSuper, a provider of prepaid credit cards and digital wallets[9], for about USD 40 million. The company now operates under the name Superdigital and was recently sold to the Spanish parent company Banco Santander for around USD 60 million.

3. Strategic cooperations

Targeted strategic cooperations with specialist providers enable banks to expand their own offerings without extensive ramp-up investments. White-label solutions from payment service providers allow the use of state-of-the-art technologies, expertise, and resources. This can generate win-win situations for both parties, although it increases the dependency on external partners.

Specific examples include the strategic cooperations of both Commerzbank (since 2018) and UniCredit (since 2020 for Germany and Austria) with EquensWorldline. Moreover, Deutsche Bank recently announced its intention to enter into a joint venture with the payment platform Fiserv. And there are other collaborations with innovative providers of new payment methods, for instance with Apple Pay. These collaborations increasingly involve the customer interface, a key area for banks.

4. Orderly retreat (“sell and leave”)

Another option for banks is to withdraw further from the payment business and leave the market to other providers. The sale of remaining payment assets, e.g., as part of a carve-out, could free up investment funds and equity for other business areas. By taking such a step, banks would, however, forgo future income from the payment business.

Conclusion on the positioning of banks in the payment market

In view of the current situation in the payments market, zeb recommends that banks take a much more proactive approach to examining their own strategic options in the payments sector, especially with regard to innovative topics, such as instant payments or cryptocurrencies. Every bank should carry out a timely analysis of whether and where payments constitute a strategic business area and to what extent an in-house solution would prove profitable.[10]

Figure 3: zeb indication based on a customer example

Figure 3: zeb indication based on a customer exampleBased on the advantages and disadvantages of the different options that have been examined here, zeb believes that an orderly retreat of banks from the payment business should only be considered in exceptional cases. In view of low interest rates, commission income from payment transactions is too important for the business model of private banks, savings banks, and Volksbank and Raiffeisenbank institutions.

Given the downsizing of assets and competencies in payments that has occurred in the past, banks now frequently lack a starting point for a “buy-and-build” strategy. Notwithstanding isolated examples, acquisitions of relevant market participants, especially by German banks, should be comprehensively examined in advance in order to establish their actual added value as part of the commercial due diligence. This holds true particularly in light of the current high valuations and premiums that have to be paid.

The possibility of strategic cooperation offers especially promising opportunities at the moment. But this may increasingly mean that banks – in relation to large players in the payment market – assume the unaccustomed role of a junior partner, who must adapt to the payment service provider. Nowadays, a bank without Apple Pay effectively loses access to a relevant customer group. What access will it be tomorrow? This applies all the more as most of the changes to date have been directed at the merchant and end customer/retail sector. When partnering with companies in payment processing via smart contracts in combination with instant payments or with instant payments as a cash substitute, there are plenty of opportunities – especially for retaining direct customer loyalty. As a result, banks will be able to generate income from payments in the years to come, while at the same time safeguarding their customer interfaces.

As a “partner for change”, zeb supports financial services providers, investors, and fintech companies from strategy definition to implementation. Thanks to a holistic consulting approach and a high level of market expertise, zeb acts as a partner both in selecting strategic options for action and in successfully implementing them in day-to-day business.