Key results

Artificial intelligence is a global “game changer”. It will transform our lives and our societies. It is sometimes said that the best way to master the future is to create it. Let’s not leave it to others to do so.[1]

In both the UK and Germany, the understanding of AI is framed more by reference to certain technologies that can be extended by AI functionalities (e.g. machine learning) than by an understanding of AI itself. Early initiatives typically focus on stand-alone solutions at divisional or department levels rather than over-arching, strategic institute-wide AI applications.

Figure 1: Framework for analysing the survey results

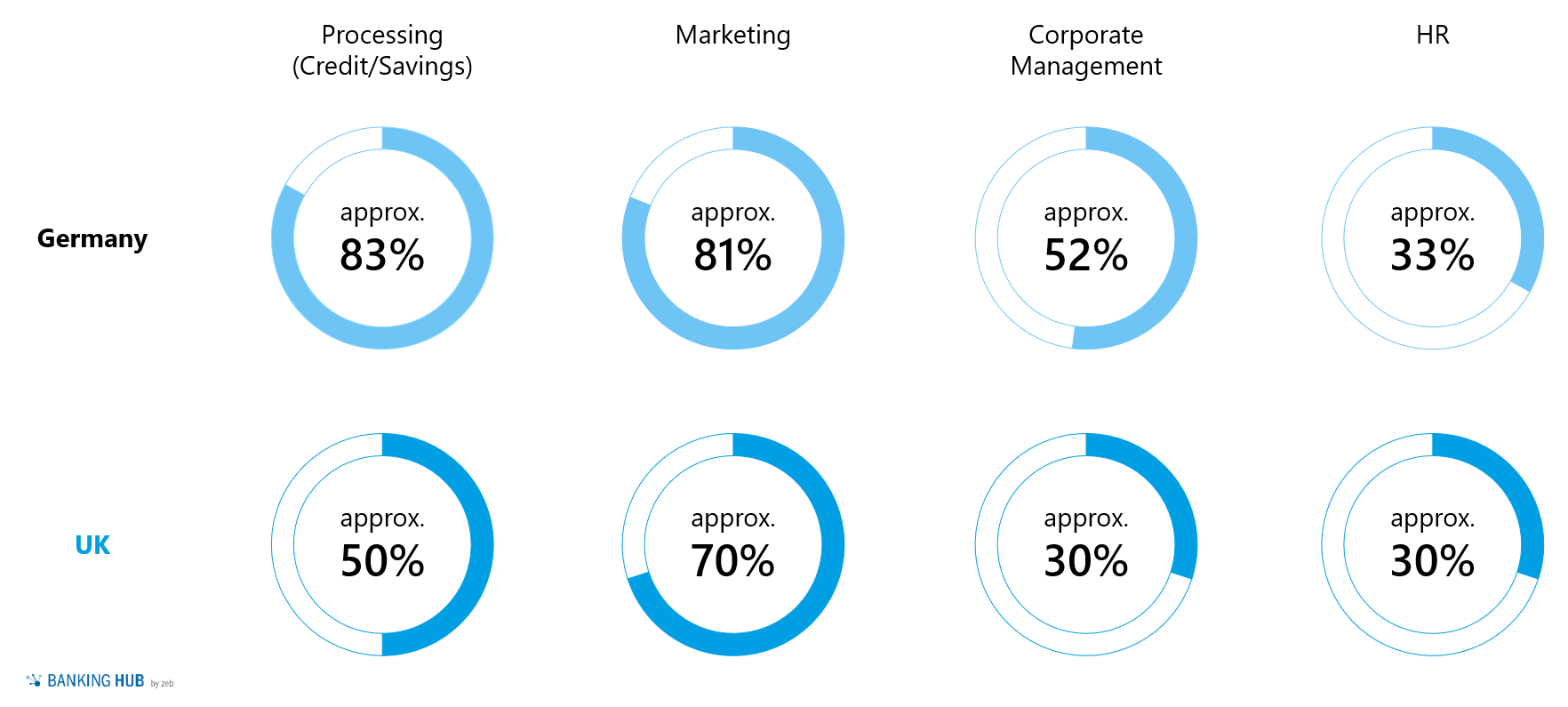

Figure 1: Framework for analysing the survey resultsUK building societies see the greatest potential application in marketing and sales while the German counterparts place more emphasis on the processing of mortgages and savings. Cost reductions and revenue growth play equal roles. The greatest challenges facing the introduction of AI are legacy IT systems and available know-how/skills followed by a lack of strategic orientation. In contrast, neither legislation nor regulation are perceived as major challenges in either jurisdiction. The finding of both surveys suggest that there are five factors for a successful application of AI in the building society sector.

Understanding AI – extending the functionality of existing technologies

The majority of UK and German participants characterized AI solutions by their ability to learn (i.e. machine learning, 90%) or as self-learning algorithms (90%). German responses also stressed cognitive systems that combine different AI technologies to simulate and imitate human thought and action and mentioned Data Analytics and Robotic Process Automation (RPA) more often. It is worth nothing that these are technologies that can be extended easily by AI functionalities rather than AI per se (e.g. combining RPA and AI to automate the processing of unstructured, paper-based data). The survey results suggest that a common framework and clear semantic has not yet developed and defined for AI. Rather, the terminology seems to be applied loosely for a range of new technologies and data-driven analytical methods. This, of course, can lead to misunderstandings or wrong expectations.

Experience with AI – stand-alone solutions vs strategic application

UK building societies had less experience with AI-related projects than German Bausparkassen (50% vs 75%) but the majority stated that they had projects planned for the next 12 months. In both countries, however, only a minority of participants indicated that AI was present at the strategic level. AI is used primarily for stand-alone solutions (e.g. fraud detection) at the divisional or departmental level. Overarching, institute-wide AI approaches have only been observed in rudimentary forms despite being critical for the successful introduction and broader use of AI. Such holistic views can be very beneficial to the provision of sufficient, high-quality databases for training and validation on AI models.

Application of AI – increase revenues while reducing costs and risks

Figure 2: Assessment of potential for application areas of AI

Figure 2: Assessment of potential for application areas of AIUK and German participants both highlighted the potential for applying AI to marketing and sales, but the latter saw greater potential impact in the processing of mortgages and savings. The potential is seen mainly in the automation of processes in combination with RPA to reduce costs. In contrast, the potential application of AI in marketing lies in increasing revenues through individual product pricing and improved sales management / market segmentation. The high potential for applying AI in processing (intelligent automation) is supported strongly by zeb project experience.

About a third of UK and half of the German participants saw potential in corporate management, i.e. Finance, Risk & Compliance. However, the results also indicate a certain caution and restraint in the use of AI due to regulatory uncertainty (e.g. in credit risk) and a sense of loss of (management) responsibility. In everyday project work, it is also apparent, that despite open regulatory questions, there are various possible applications for AI, for example in forecasting implicit options for mortgages (e.g. prepayments) or deposits (e.g. stickiness).

Only about 30% of UK respondents see potential for the use of AI with regards to HR, which is in line with the German responses. As possible explanations, the participants cite the high sensitivity of personal information and the high importance of traceability in HR decisions.

The majority of the participants see the IT sector in the central role as enabler and partner in the concept development and implementation of AI solutions.

Challenges in AI introduction – know-how, systems and strategic orientation

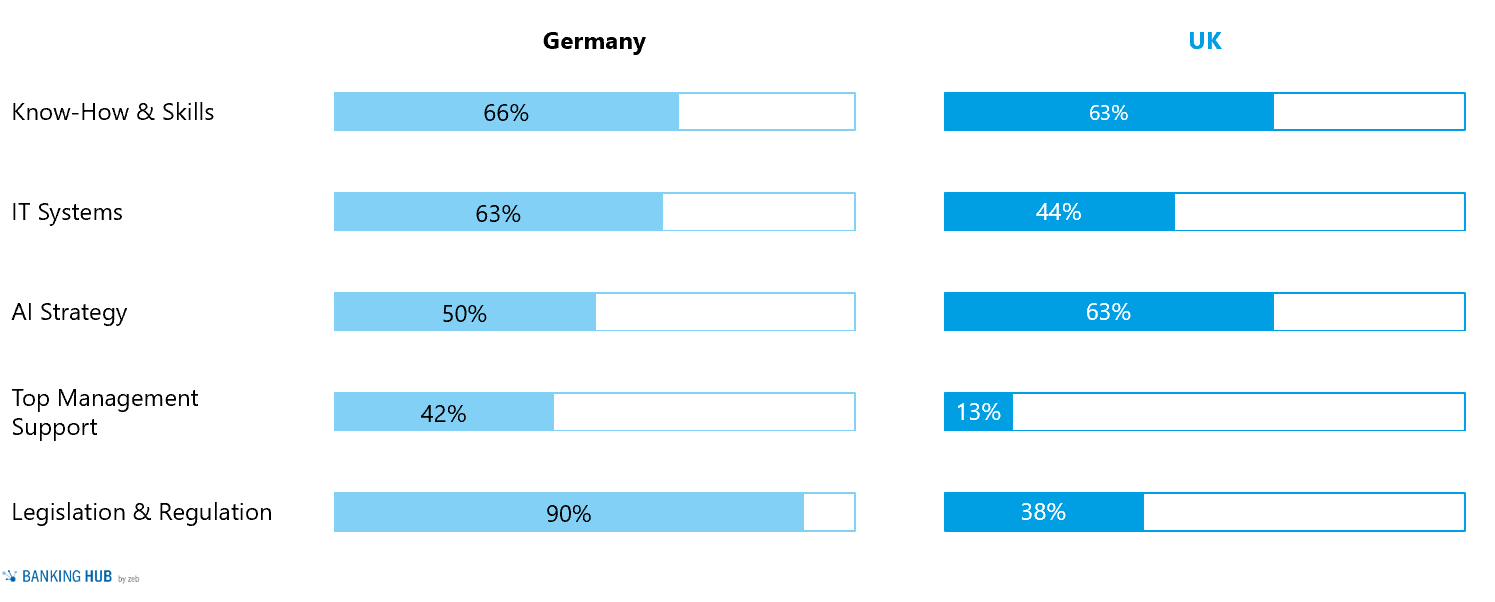

Figure 3: Main challenges facing AI introduction

Figure 3: Main challenges facing AI introductionMore than half of the participants cited know-how, skills and legacy IT systems as central challenges. The former refers to limited internal competencies relating to AI methods and models. The latter often results in dispersed and heterogeneous data sets. It is, however, the availability as well as the quantity and quality of the database are decisive for the use of AI.[2]

A majority of participants mention the lack of a strategic orientation towards AI as the next biggest challenge. Overall, the UK answers match mostly with the German Bausparkassen survey differentiating only a little in the exact ranking of individual concerns.

Success factors – lessons from the survey and wider experiences

The findings of the UK and German surveys and our experience from other financial service institutions point to five factors that will determine whether the continuing application of AI in building societies will be successful or not:

Recognise the strategic relevance: AI is already changing the economics and competitive dynamics in the market for savings and mortgages and other financial services.[3] The associated benefits and challenges need to be recognised at an early stage along with the comprehensive strategies to proactively shape them.

Organise your data: AI, machine learning and any kind of advanced analytics is only as good as the data feeds on which they are built. Admittedly, the advent of new ways of organising and storing data as well as modern algorithms that accept “fuzzy” data points help. Nevertheless, a primary focus should always be put on the quantity and quality of available (external and internal) data.

Collaborate and always gauge value-add: Business and IT representatives need to closely work together. Otherwise, AI either remains toy without real business application or wishful thinking without realistic implementation scenarios. At the end of the day, AI is only a means to solve business problems and not an end in itself.

Empower and inspire employees: Managers and employees are likely to feel challenged or even threatened by AI. New AI competencies need to be acquired and the correct motivation ensured to provide commitment to new initiatives. Ethical questions should be addressed openly and not brushed aside.

Be courageous and allow failures: Courage is a prerequisite for walking new paths and overcoming obstacles that inevitably arise. Inevitably, mistakes will happen in trial and error phases. Embracing a true “failure” culture is a central cornerstone of making AI happen in FSI and delivering upon its promises.

Conclusion

AI is already adding functionality to the technologies that are shaping the economics and competitive dynamics of savings and mortgage markets in the UK and in Germany. Early initiatives are focused typically on stand-alone solutions in marketing and in processing with a focus on increasing revenues, reducing costs and managing risk. The main challenges to a wider application of AI are a shortage of know-how, legacy IT issues and a lack of strategic orientation.

The results from this unique zeb survey suggests that German Bausparkassen are slightly more experienced with AI-related projects than their UK building society peers and, more importantly, that insights from their experiences can be transferred to the UK market directly and vice versa. We believe that cross-border exchanges regarding AI are beneficial to building societies in Germany and the UK alike. For this reason, we will continue helping to build bridges in a post-Brexit world by sharing information and experiences and act as a guide in these unchartered waters.