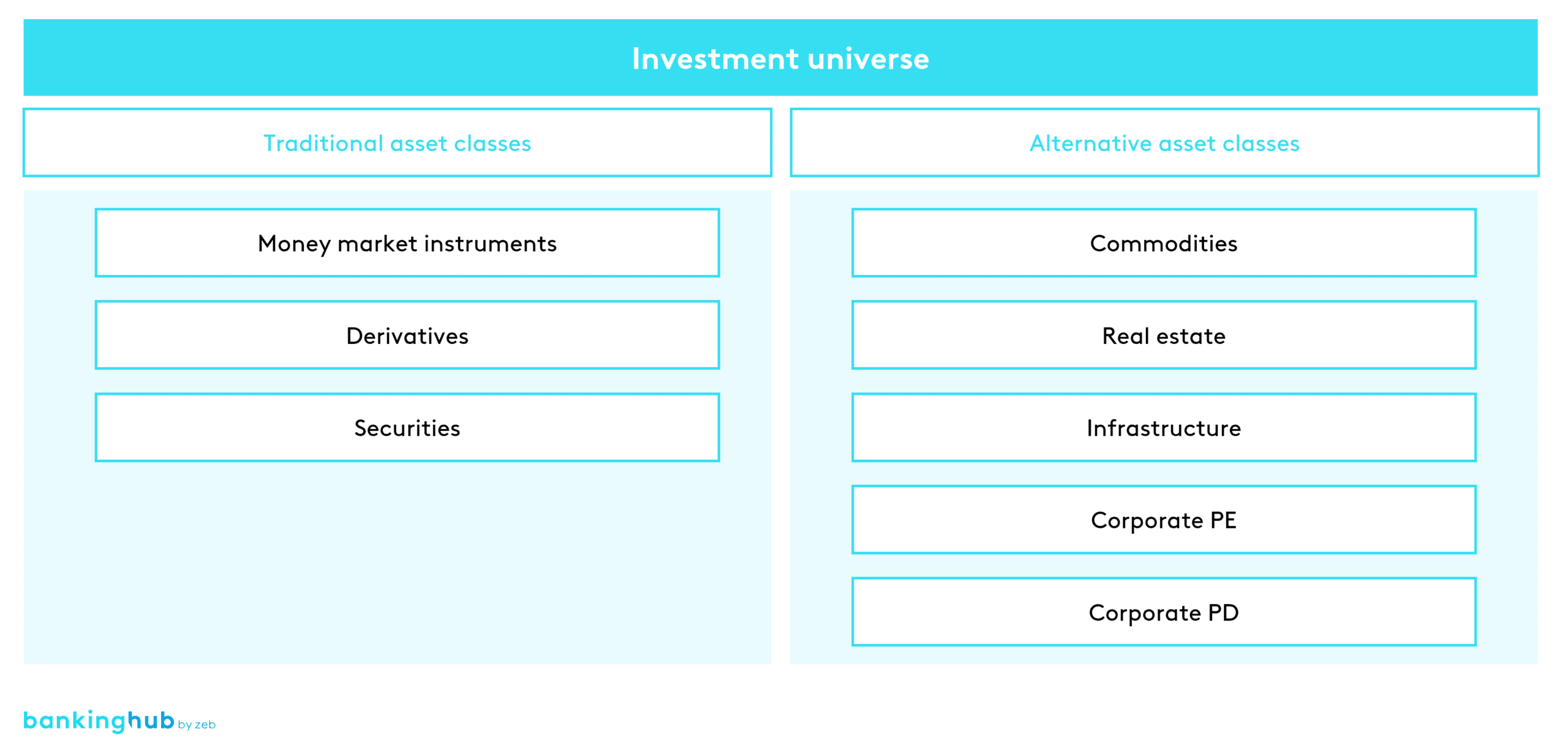

Special features of alternative assets

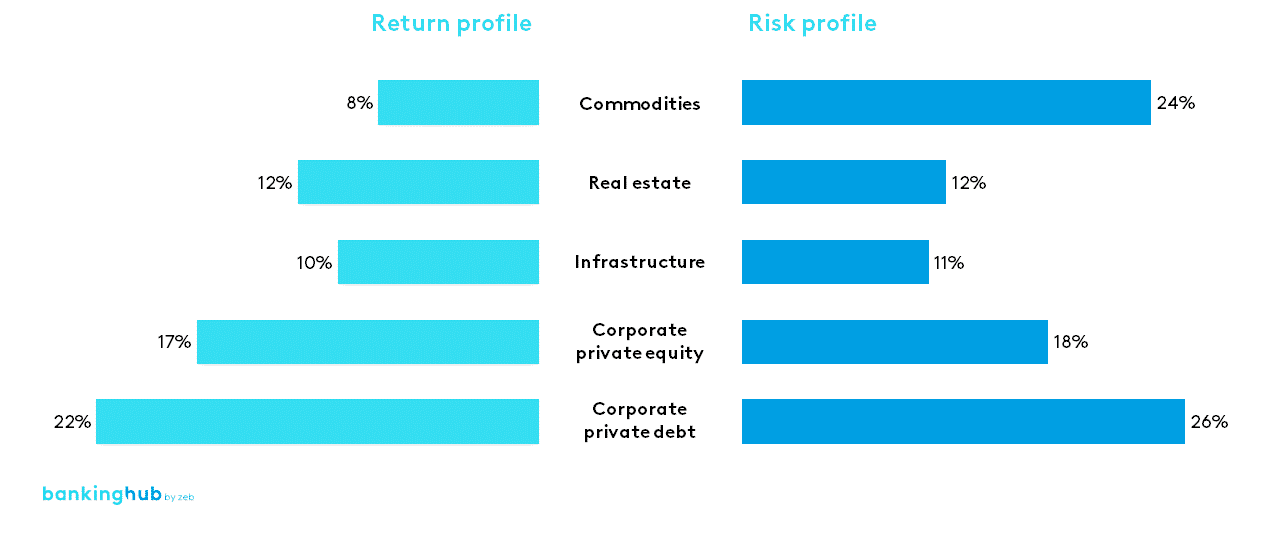

Since alternative investments (see figure 1[1]) are generally not traded on an exchange, there are some specific aspects to consider when comparing them to securities, money market instruments and derivatives. First and foremost, alternative investments are much less liquid than traditional assets and tend to have a low correlation with them. Secondly, the relatively high return and risk potential of these asset classes is often emphasized (see Figure 2[2]).

Alternative asset classes are generally less regulated and therefore less transparent. Finally, depending on the asset itself, the configuration of the investment and its legal wrapper is significantly more complex compared to standardized financial instruments.

Investments in alternative asset classes are primarily made by institutional investors, such as insurance companies, pension funds and family offices. This is mainly due to difficult access channels, high minimum investment amounts and long capital commitment periods. Institutional investors use alternative assets primarily for risk diversification, long-term capital accumulation and to generate stable, regular payouts.

Overview of selected alternative asset classes

Short- to medium-term alternative asset trends

Various surveys show that alternative investments are an important part of institutional investors’ portfolios, and that this share could increase further in the coming years. The Investor Survey 2022 of the German Association for Alternative Investments (Bundesverband alternativer Investments), for example, shows that the majority of investors would like to maintain or increase their portfolio allocation to alternative investments, which currently stands at around 25%. J.P. Morgan’s 2022 Long-Term Capital Market Assumptions confirm this finding – alternative assets are an integral part of institutional investors’ allocation considerations.

What are the reasons for increasing the share of alternative assets in the portfolio?[7]

On the one hand, the coronavirus pandemic and Russia’s war of aggression against Ukraine heralded the end of an era of stable capital markets and made uncorrelated asset classes much more attractive. On the other hand, there are other developments that could further increase demand for certain alternative assets.

First and foremost, investors face inflation driven by supply shocks and low but rising interest rates. Given supply chain constraints and global nationalization efforts, inflation is unlikely to moderate significantly over the next few years, at least in the short to medium term. Consequently, investments in tangible assets, whose value usually increases in times of inflation, such as real estate and infrastructure, are becoming more attractive.

Furthermore, in keeping with the spirit of social change, investors are seeking greater sustainability in their portfolios. Investments in infrastructure are particularly well suited for this purpose. Promoting renewable energy, for example, can reduce global carbon emissions. Alternatively, investments in commodities may be classified as sustainable under certain circumstances. For example, investing in forest land can provide a steady stream of income through the sale of timber as a sustainable building material, while at the same time the forest land can be managed sustainably, which can contribute to carbon sequestration. Finally, technological innovation is often driven by young, independent companies, providing ideal opportunities for venture capital investment.

However, volatile capital markets and inflation are also fueling uncertainty and fears of recession, which are having a significant impact on investors’ risk appetite and investment behavior. It remains to be seen whether the latter will primarily focus on the many reasons for investing in alternative assets and whether the surveys on the increasing shares of alternative assets in portfolios will prove true.

Developments in alternative assets on the supply side

The supply side, too, is already showing signs of an increase in alternative asset offerings. On the one hand, as in previous years, regulators are expected to continue to drive forward access to alternative asset classes for retail investors, both in the form of direct investments and through inclusion in fund offerings. Pioneering initiatives include the 2013 European Venture Capital Regulation (EuVECA) and the 2015 European Long-Term Investment Fund Regulation (ELTIF). The EuVECA Regulation has set relatively loose conditions for launching venture capital funds, while the ELTIF Regulation has created a framework to promote long-term European investment in the real economy, targeting in particular private investors who have so far not been able to invest in infrastructure projects.

In addition to the regulatory framework, asset managers are also looking to gradually expand their product offerings to include alternative asset classes, either by incorporating alternative assets into existing funds or by launching new products exclusively geared to alternative investments. The main driver is the fierce price war fueled by the emergence of passive solutions and the resulting low margins on traditional products such as equity and multi-asset funds.

In addition, offering alternative products allows asset managers to differentiate themselves from their competitors. For example, traditional financial products can be used as core investments in a holistic approach to managing customer funds, while alternative assets can be used as satellites, primarily to generate returns.

Long-term development of alternative assets

The amount of money invested in alternative assets is also expected to increase over the long term. Blockchain technology can break down assets into small shares, known as security tokens, thereby making them accessible to a large number of people at low cost. This technology also enables decentralized recording, validation and execution of transactions that are immutable and thus largely tamper-proof.

Regulators have recognized these advantages, and the German government, as a pioneer in the European Union, is gradually creating a legally secure framework for token trading. As early as June 2021, the first cornerstone was laid with the German Electronic Securities Act (eWpG). The next step is expected in 2023 with the EU-wide Digital Ledger Technology Pilot Regime, which is aimed at investment firms, market operators and CSDs, and will enable the operation of a digital ledger market infrastructure.

Implications for market participants

The question arises as to what the developments outlined above mean for the various market participants, both on the demand and the supply side.

For investors, such as insurance companies, pension funds, family offices and, where applicable, private individuals, two key questions arise in light of the market developments.

- First, should alternative assets be included in a portfolio, taking into account their different risk-return profiles and their low correlation with traditional asset classes?

- If the answer to this question is yes, then another question arises: how is the investment made? There are several options. In addition to direct investments or investments in suitable securities, it is possible to acquire shares in funds that contain alternative investments. Alternatively, an asset management mandate can be signed, whereby the investor leaves investment decisions to the respective asset manager.

Against this background, regulators are also called upon to lay further legal foundations for investments in alternative assets. In this context, well-functioning markets, such as the private equity and venture capital market in the US, could serve as a model. It is also important to further expand the basis for token trading and to make alternative assets available to private individuals in terms of easy access, lower minimum investment amounts and shorter capital commitment periods.

Asset managers will take advantage of the regulatory framework and successively expand their range of alternative asset classes in order to differentiate themselves from the competition and, above all, to benefit from the still prevailing higher margins. However, since alternative assets differ greatly from traditional assets in terms of value creation, the question arises as to whether asset managing companies should build up / expand the expertise by themselves or obtain it through the acquisition of specialist firms.

Offering alternative assets requires fundamental changes in the structure and processes of both the front and middle office. Assets such as real estate or infrastructure companies, for example, are only included in a portfolio after extensive due diligence and contract negotiations, and in addition, it should be borne in mind that such properties also need to be managed. This includes tasks that go beyond the typical fields of activity of an asset manager, such as the development of property strategies and technical or leasing management. Consequently, skills and expertise are required that are not available among the typical staff of an asset management company. Property-related activities can alternatively be outsourced, although finding the right partner is made more difficult by what is currently still a limited offering.

As a long-standing partner of established banks and asset management companies in Europe, zeb has always kept a close eye on changes in the capital markets, investor needs and the conditions in a wide variety of institutions. Drawing on extensive knowledge and experience in the field of alternative assets and their integration into portfolios and organizations, we have been supporting asset managers in developing and expanding their range of services for many years. As partners for change, we help our clients master the only constant – change – and support them with expertise and foresight in dynamic times.