The (banking) world in coronavirus fever

This situation has various implications for regional banks. In addition to the economic consequences for their own P&L and a changing working environment, banks have to respond in particular to their crisis-ridden customers, who need quick solutions and support in many areas right now.

We expect increased risks and defaults in banks’ commercial and private lending business, which will primarily be driven by their customers’ financial difficulties and, ultimately, insolvencies. To make matters worse, the (temporary) drop in income of many retail customers compared to the usual level and a (temporary) increase in the number of unemployed people further aggravate this situation.

Even though, due to various uncertainty factors, there are no reliable projections to date, the coronavirus pandemic will certainly have a negative impact on the entire economy. More than ever before, banks need to master this difficult situation together with their customers in the best possible way and emerge stronger than they were before.

Regional banks as crisis partners for their customers: challenges and opportunities

Since the beginning of the crisis, banks have implemented numerous immediate measures to ensure their operational capacity to act and to stabilize customer business. The daily (re)orientation following current developments and findings as well as the associated (re)prioritization and taking up of new tasks are currently a fixed item on the daily coronavirus crisis management agenda at all banks. In order to ensure the ability to act and work, banks have already found and implemented pragmatic working regulations in sales, operations and control for their employees, both on-site and remote. According to individual circumstances and experiences within the institutions, they adapt and supplement existing regulations and further professionalize their crisis-mode working methods.

Based on our current experience and findings from cooperation and exchange with banks on the coronavirus topic, we can group the immediate measures for stabilizing the capacity to act into four areas (see Fig. 1).

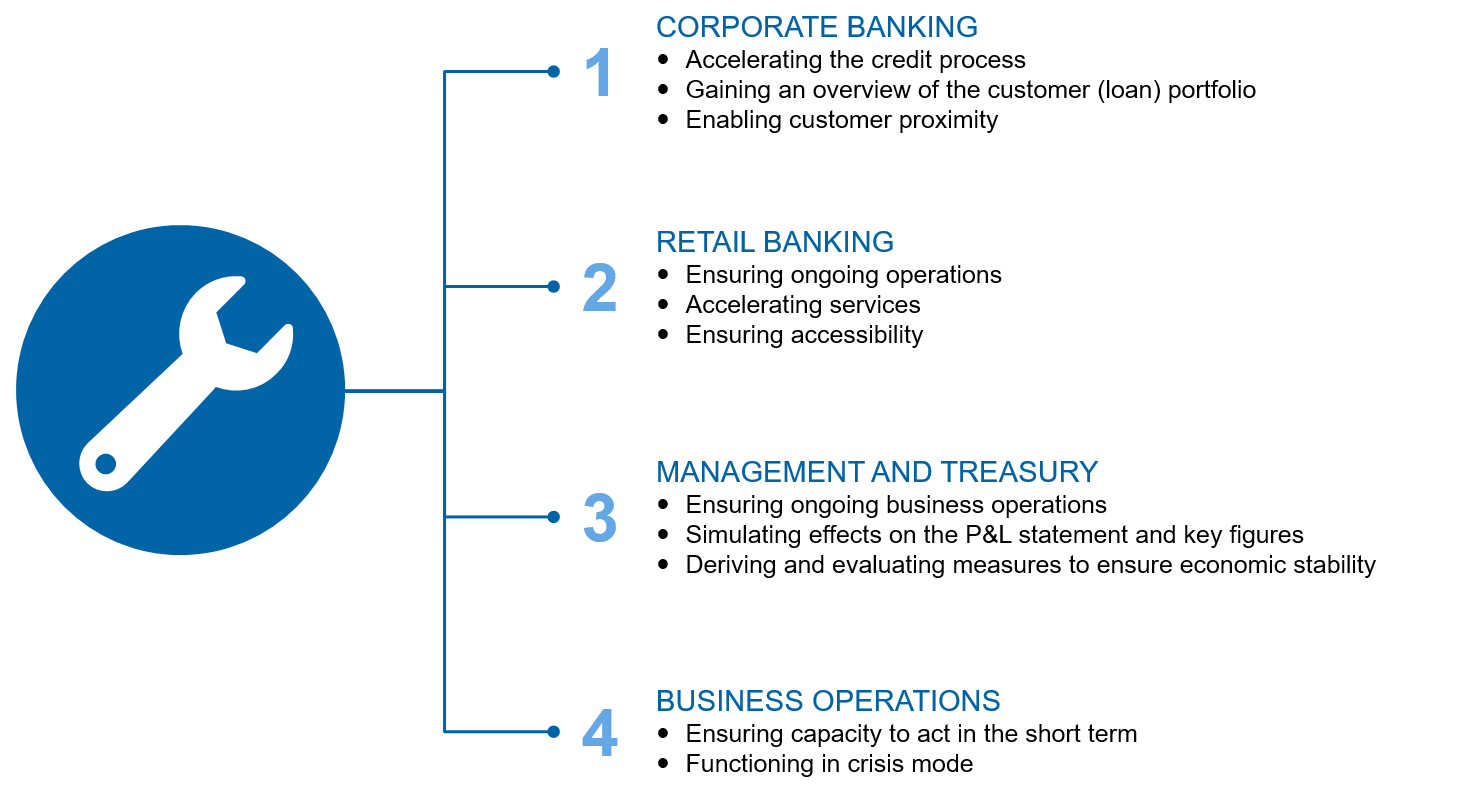

Figure 1: Immediate measures for regional banks

Figure 1: Immediate measures for regional banksMany institutions are currently facing major challenges in corporate banking. As a result of the coronavirus crisis, the liquidity situation of many customers deteriorates, credit default risks increase massively, transparency and an overview, e.g. of concrete effects, are often still lacking and advisors experience uncertainty and an enormous workload. Banks must provide their customers with short-term liquidity so that they can continue to pay salaries, for example. In addition, they need to arrange government aid. This requires to rapidly increase knowledge among relationship managers as well as to establish and maintain transparency regarding the programs that are suitable for the customer.

The levers on both the process and organizational levels are complex. In principle, the urgency of the situation requires rapid and pragmatic implementation within the local banks.

What are effective immediate measures in corporate banking?

- Accelerating the credit process: implementing ad-hoc measures, adjusting framework conditions, introducing simplified credit processes, broad-based knowledge development regarding the application for subsidies

- Gaining an overview of the customer (loan) portfolio: data-based clustering of customer portfolios and automated calculation of expected liquidity requirements

- Enabling customer proximity: ensuring virtual proximity to customers, providing concrete tools and internally relocating free resources

At present, retail banking also faces extraordinary burdens, such as temporarily closed bank branches.

What are effective immediate measures in retail banking?

Regional banks aim at providing the most comprehensive customer service possible, whereby creating adequate physical and digital customer presence is a top priority. Banks must implement the following three immediate measures:

- Allocating resources for daily business: organizing presence in stationary sales (branches, opening hours, cash supply), shifting employee capacities from service and consulting of stationary units to the customer service center and/or the digital consulting center

- Accelerating services: establishing first-level and second-level support within the customer service center, whereby the following applies: first-level support for simple queries and second-level support for more in-depth consulting requirements (staffed by advisors from branches)

- Ensuring accessibility: creating additional communication options (chat, contact form, hotline, e-mail) and actively approaching the customer or keeping close contact with the customer in order to generate sales impulses for the time following the coronavirus pandemic

In addition to maintaining operations, managing the bank as a whole requires the best possible assessment of the expected effects of the pandemic on relevant key figures and also the identification and exploitation of opportunities in the current market environment.

What are effective immediate measures in bank management and treasury?

- Organizing ongoing business operations: safeguarding business operations (submission of supervisory reports, risk reporting, maintaining (proprietary) trading capability), regular communication/information as a component of the risk culture

- Simulating effects on the P&L statement and key figures: reviewing the customer business and treasury portfolio as well as the parameter/key figure set, adjusting business, capital and earnings planning, conducting stress tests as required

- Deriving measures to ensure economic stability: deriving and evaluating measures to ensure the economic stability (P&L, capital, risk, liquidity) of the entire bank, evaluating and seizing opportunities in the current economic and regulatory environment

In order to ensure the ability to act, it is decisive to fully digitalize the core processes in accordance with the “function before optimization” principle. This is the only way to ensure that the work and (virtual) collaboration of employees can continue to take place partly on the banks’ premises on site and when working from home. Apart from process digitalization, the largest fields of action in this context are organization and enabling virtual work and collaboration.

What are relevant immediate measures for working from home and virtual collaboration?

Creating the technical basis for working from home requires the provision and rapid activation of tools (e.g. Skype, Zoom, GoToMeeting)—as well as clarifying issues relating to flexible working hours. Banks should implement these immediate measures in two waves:

- Ensuring capacity to act in the short term: creating the legal and technical conditions to enable employees to work from home

- Functioning in crisis mode: organizing work and collaboration in virtual teams, including smooth implementation of regulatory and legal requirements

You can find further information on the work and collaboration of virtual teams in crisis mode here:

Work and collaboration of virtual teams in crisis mode (German version only)

Regional banks will emerge stronger from the crisis if they manage it successfully, consistently implement necessary immediate measures and take advantage of opportunities.

Banks can prove themselves to their customers as “reliable partners and caregivers in the crisis”. In the crisis-ridden lending business, banks have the opportunity to further expand their business, e.g. by making greater use of lines, or by achieving higher margins in new customer business. Customers’ perception of the bank’s digital sales competence is likely to increase, which opens up attractive opportunities. Regional banks can use this momentum to place digital sales channels permanently with their customers and position themselves as competent multi-channel suppliers and innovative financial service providers.

Within the banks, employees are unburdened through accelerated credit processes, for example, are (forcibly) digitally enabled, and the mentality of a pragmatic approach strengthens the solidarity within the teams. Further opportunities lie in establishing the higher decision-making speed within many institutions, which is required in the current climate, as well as increasing and maintaining greater flexibility and adaptability among employees.

From crisis mode back to normal business

The question of how to proceed after the crisis is a driving factor for all banks. To this end, they assess and discuss the economic effects, e.g. through the increase in valuation results in the lending and securities business and the change in earnings potential on the basis of general economic data. At the same time, banks revise their plans, calculate new scenarios and make possible changes visible.

In addition to the expected negative economic effects, however, there are also opportunities in customer business, treasury and on the cost side of banks. Thus, on the one hand, we expect customers’ creditworthiness to decline in customer business, but on the other hand, the rising demand for loans will also lead to higher margins in variable business. Many customers’ declining cash flows also contribute to an increasing credit volume. Moreover, we expect falling interest rates on the market to lead to positive price gains in the securities account (Depot A) of many banks. The currently “decreed” substitution of physical presence in branches by digital sales channels will effectively leverage efficiency potentials of other dimensions.

Overall, we assume that the crisis will weaken the business management basis within the banks—as mentioned above, the effects of the coronavirus crisis depend on the duration of the “lockdown” and the associated gradual exit.

What will happen once the banks have managed the crisis?

Once the economy has been gradually and controllably ramped up and banks have assessed the effects in concrete terms and converted their emergency management successively to “normal” business operations, they must refocus as quickly as possible on the strategic development and implementation of measures.

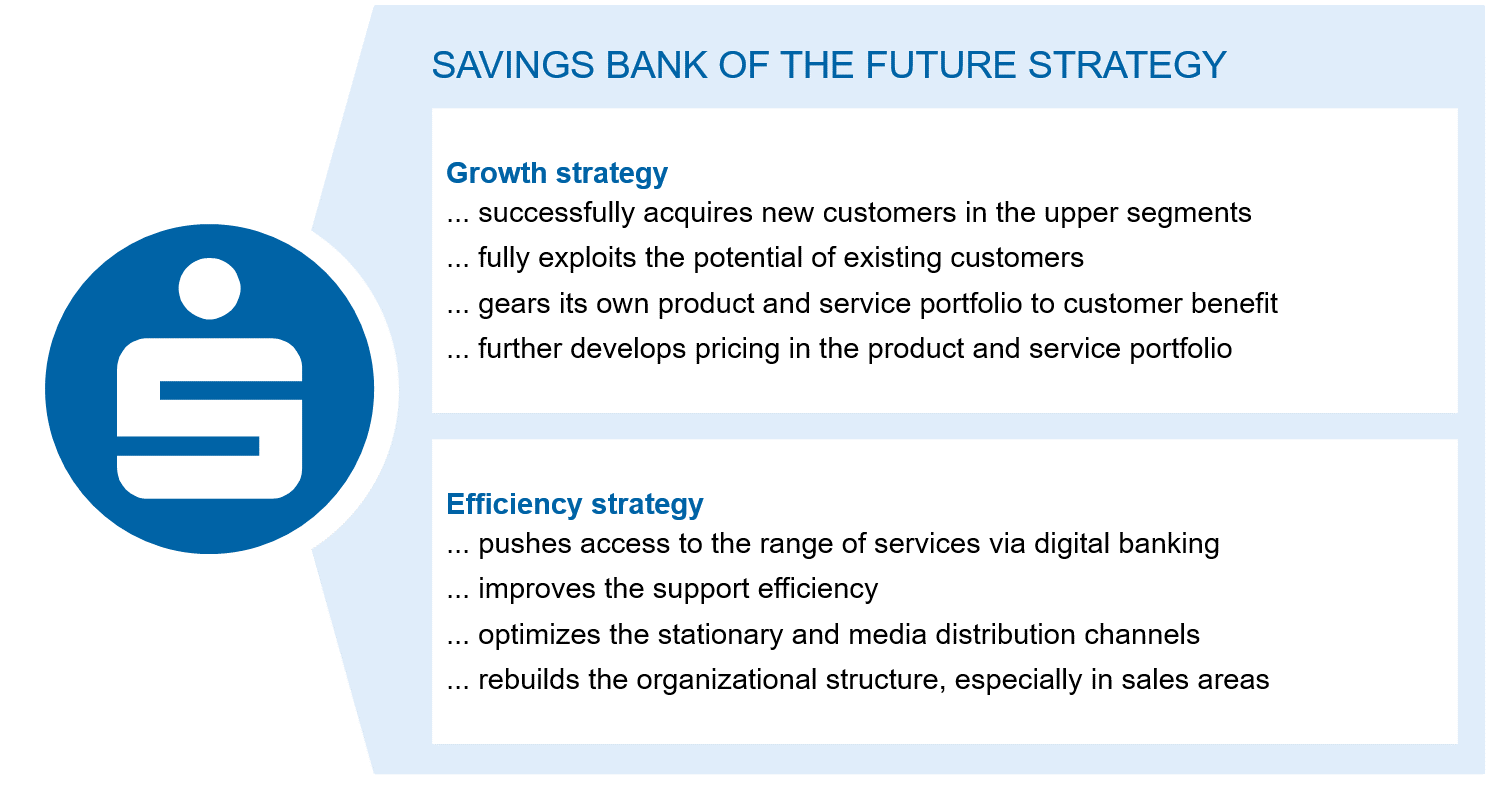

In addition to individual topics, the strategic orientation of many regional banks for sales in customer business focuses in particular on the central growth and efficiency issues prior to the coronavirus pandemic.

Figure 2: Strategic orientation at regional banks

Figure 2: Strategic orientation at regional banksThe basic strategic orientation, which was the right one just a few weeks ago, will remain in its core after the coronavirus pandemic.

The growth strategy, for example, continues to push necessary expansion in the lending and securities business with both commercial and retail customers, as well as aligning a value-added product portfolio for the customer, including insurance and provision products, and the pricing of products and services. The efficiency strategy includes, for example, the reorganization of sales structures, the further streamlining and comprehensive automation of processes, the shifting of individual tasks to the customer, and requires constant digitalization throughout the bank.

All these issues will continue to be of enormous importance for the further development and the maintenance or expansion of the institutions’ competitiveness and the banks must therefore pursue them as a matter of principle. Banks must, however, review the measures decided on to implement their individual strategies with regard to the expected effects on earnings (cost savings and/or increased earnings) and their realization in medium-term planning. Because of the coronavirus crisis, banks are currently unable to realize as planned the efficiency potential already identified in the credit back office area, for example, or to leverage priced-in earnings effects along the individual customer segments and products. On the other hand, however, they must also review the timing of the implementation of measures. Banks can, however, implement changes to sales structures more easily and directly—the window for the radical substitution of branches with digital sales channels will be wide open in the coming months.

With a view to the entire financial services industry, the coronavirus crisis will further increase the business pressure. Where stand-alone bank strategies are not sustainable in the long term, we expect consolidation processes to gain in momentum.

Facing the future with renewed strength

The coronavirus crisis presents regional banks with unprecedented challenges. The first step is therefore to implement a pragmatic crisis management and to establish and professionalize immediate measures to stabilize customer business. A second step, based on the actual effects and results, is to operatively evaluate the strategic action measures within the banks and to adjust them, if necessary.

Regional banks must seize the opportunity to prove themselves as partners to their customers also during the crisis, to emerge from the crisis with positive changes and to maintain a change of mindset even beyond the crisis. This includes taking advantage of new business opportunities, continuing the major advances in digitalization and agility, but also implementing a new sales-driven digital strength.

In addition to the authors, other zeb contact persons will be happy to assist you:

- Corporate banking: Marion Pfaller, Tobias Schnitzler

- Retail banking: Dr. Hans-Jörg Kuttler, Martin Seidenberg

- Business operations: Michael Kühnelt, Christoph Wienert

- Virtual collaboration / working methods: Martin Fürst, Prof. Dr. Joachim Paul Hasebrook